Tencent Music Entertainment Group stock has had a tough run over the last year, yet both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings-based valuation checks currently point to the shares trading at a discount to that underlying assessment.

- Over the past 12 months, Tencent Music Entertainment Group is down 54.5%, which means recent shareholders are sitting on sizeable paper losses despite the stock screening as undervalued.

- The key support for any upside case is whether Tencent Music Entertainment Group can sustain healthy cash generation from its music and audio platforms. The main risk is that slower user monetisation or higher content costs could weigh on future cash flows and narrow the apparent discount.

- On Simply Wall St's broader checks, Tencent Music Entertainment Group looks undervalued in 5 of 6 tests, and you can see that breakdown at this valuation summary.

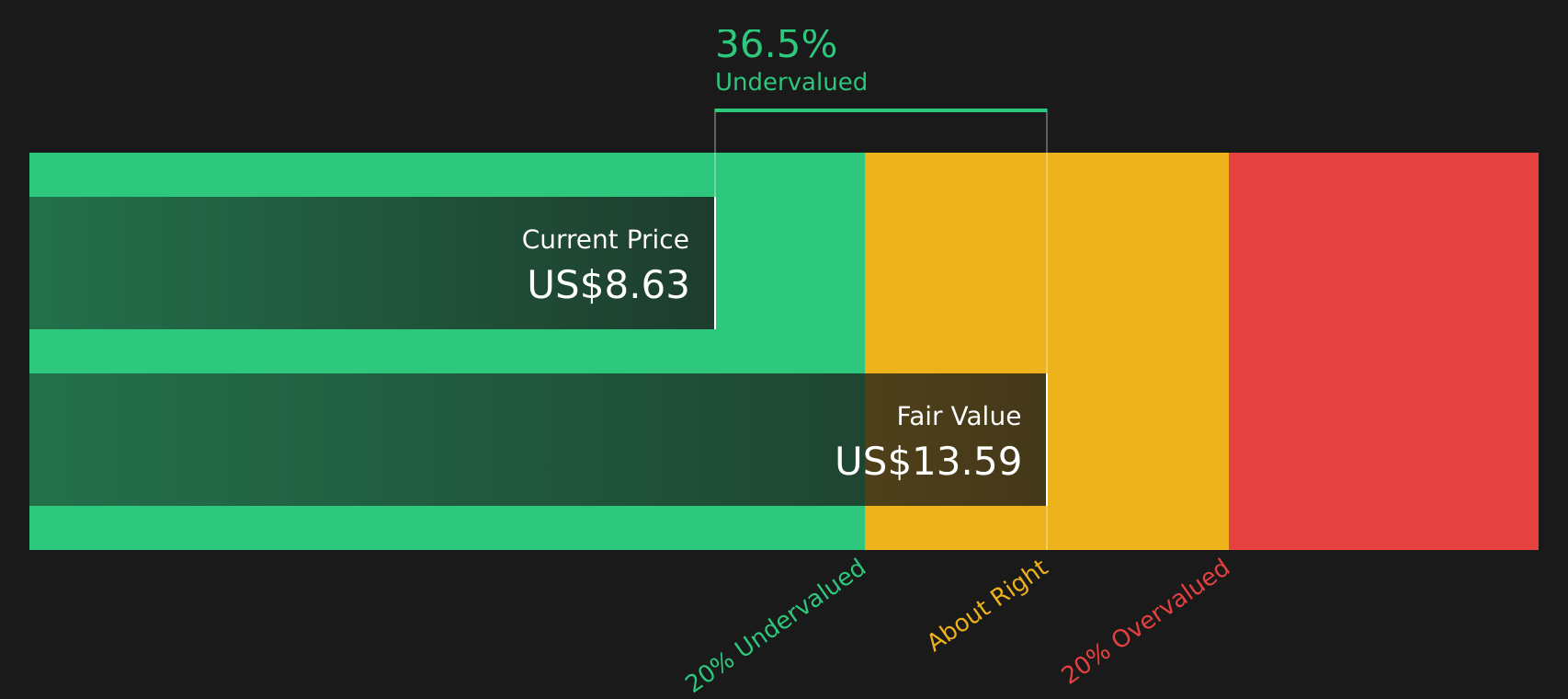

The issue now is whether Tencent Music Entertainment Group's share price at around US$8.63 genuinely offers a margin of safety relative to its current intrinsic value estimate.

Does Tencent Music Entertainment Group Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Tencent Music Entertainment Group could be worth based on the cash it generates for shareholders. On the latest figures, the company produced last twelve month free cash flow of about CN¥8.8b, and the model assumes these cash flows continue to grow from this base over time rather than shrink.

Using those projections, the DCF points to an intrinsic value of about $13.59 per share, compared with the current share price of around $8.63. That implies the stock trades at roughly a 36.5% discount to the model’s estimate, which indicates Tencent Music Entertainment Group may be pricing in more caution than the cash flow profile alone shows.

On this DCF view, Tencent Music Entertainment Group stock appears undervalued relative to its estimated intrinsic worth.

Our Discounted Cash Flow (DCF) analysis suggests Tencent Music Entertainment Group is undervalued by 36.5%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Tencent Music Entertainment Group a Bargain on Earnings?

The P/E ratio is a useful lens for Tencent Music Entertainment Group because it links what you pay for the stock to the earnings the business is already generating. On this measure, Tencent Music Entertainment Group trades at about 10.4x earnings, compared with an Entertainment industry average of roughly 23.0x and a broader peer group average of about 81.1x.

A tailored fair P/E multiple for Tencent Music Entertainment Group, which considers its size, profitability profile and industry risks, is around 20.8x. Compared with the current 10.4x, the stock is priced at a sizeable discount to what this framework suggests could be reasonable if earnings remain at similar levels. It also sits well below both industry and peer benchmarks.

On this earnings multiple, Tencent Music Entertainment Group stock appears undervalued relative to both its tailored fair P/E and sector comparisons.

See what the numbers say about this price — find out in our valuation breakdown.

The Tencent Music Entertainment Group Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Tencent Music Entertainment Group pick up where this valuation puzzle leaves off. They spell out what would need to happen to Tencent Music Entertainment Group's growth, margins and earnings for the stock to be worth materially more or less than today's price, and they sit on the Community page. Rather than a single multiple or model output, each one lays out the assumptions behind its fair value so you can compare them with the actual results as they come through.

One of the top community narratives on Tencent Music Entertainment Group: 44% undervalued

"Proprietary content development, exclusive partnerships, and investments in original artist incubation strengthen content differentiation, support premium pricing, and reduce long term content costs…"

Read one of the top narratives on Tencent Music Entertainment Group

Do you think there's more to the story for Tencent Music Entertainment Group? Head over to our Community to see what others are saying!

The Bottom Line

For Tencent Music Entertainment Group, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings-based multiples point in the same direction, with the stock screening as undervalued on current assumptions. The key question is whether Tencent Music Entertainment Group can keep converting its music and audio platforms into steady cash generation without a meaningful squeeze from user monetisation trends or content costs. If that cash profile holds up, the current discount may reflect caution rather than fundamentals. However, if those pressures intensify, the gap between price and intrinsic value could prove justified.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com