NovoCure (NVCR) has drawn fresh attention after Bronstein, Gewirtz & Grossman, LLC announced an investigation into potential claims tied to Phase 3 TRIDENT trial results and the subsequent sharp drop in the stock.

See our latest analysis for NovoCure.

The latest legal investigation comes after a sharp reaction to the TRIDENT trial outcome and follows a period where NovoCure's 90 day share price return of 63.03% contrasts with a 5 year total shareholder return that has declined 91.16%. This suggests recent momentum sits against a much weaker long term record.

If you are reassessing risk after the TRIDENT update, it could be a good moment to broaden your watchlist with 40 healthcare AI stocks.

With NovoCure now trading far below its 5 year peak but up sharply over 90 days, and carrying a recent addition to several value indexes, is this punishment overdone, or is the market already pricing in whatever growth lies ahead?

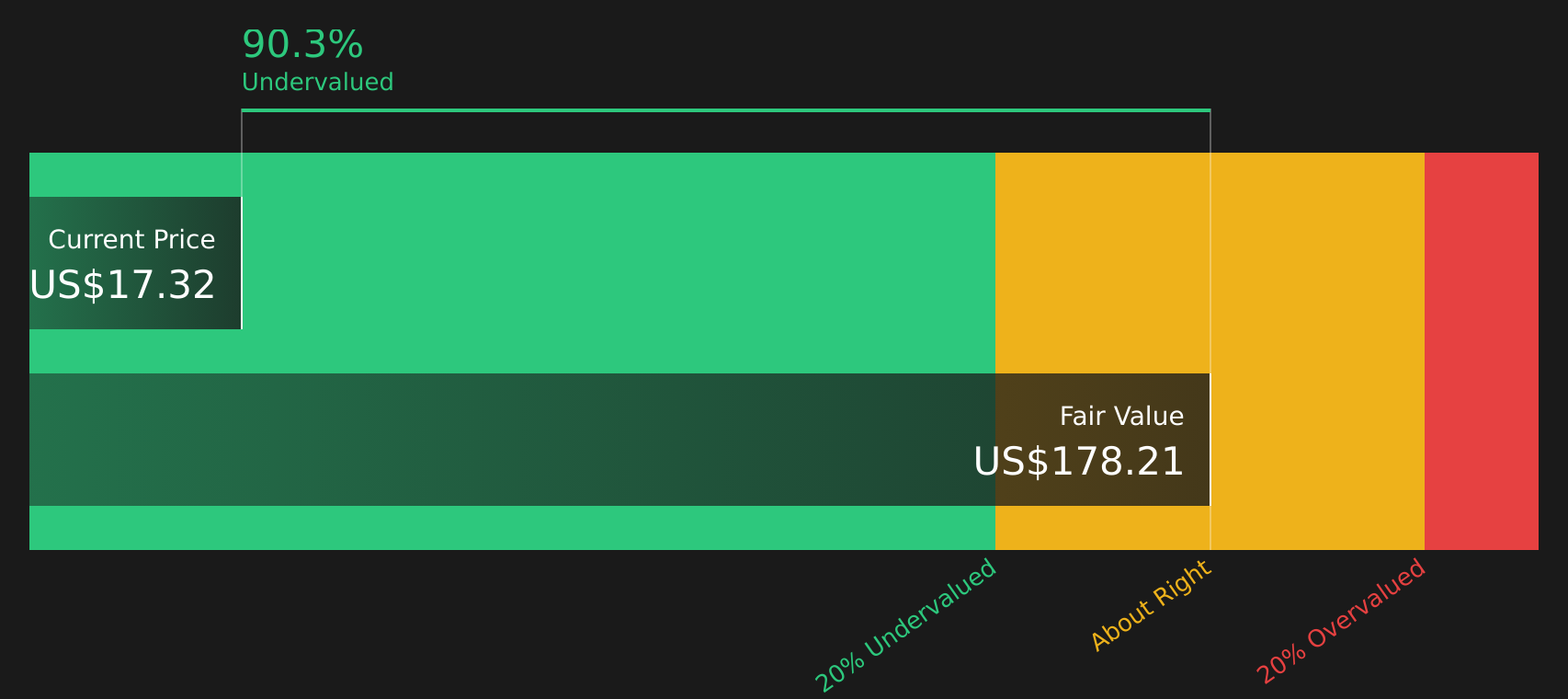

Most Popular Narrative: 34% Undervalued

The most followed narrative on NovoCure compares a fair value of $26.07 against the last close of $17.20. This frames the recent sell off as potentially excessive and heavily tied to how future trial outcomes and adoption trends play out.

Validation of TTFields therapy in multiple new indications, such as pancreatic cancer (PANOVA-3) and brain metastases from non small cell lung cancer (METIS), positions NovoCure for potential regulatory approvals and large market expansion beginning in 2026, likely driving topline revenue growth as global cancer incidence rises in the aging population.

Want to see what sits behind that fair value gap for NovoCure? The narrative leans on sustained revenue expansion, rising margins and a richer future earnings multiple. The key question is how aggressively all three are modeled to evolve.

Result: Fair Value of $26.07 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, NovoCure’s story can change quickly if prescription growth in newer indications stalls or if reimbursement progress slows. This would challenge the current upbeat narrative.

Find out about the key risks to this NovoCure narrative.

Another View on NovoCure’s Valuation

The fair value of $26.07 comes from an earnings based model built around analyst targets, but the SWS DCF model paints a far more aggressive picture, with NovoCure trading about 90% below its future cash flow value. Is this a signal of deep mispricing or just very optimistic cash flow assumptions?

To understand how much faith to place in those cash flow projections versus the market price, take a closer look at how the SWS DCF model treats growth, margins and risk, and what would need to go right for the gap to narrow: Look into how the SWS DCF model arrives at its fair value.

Next Steps

If the NovoCure story so far feels mixed, with real concerns on one side and genuine upside on the other, now is the time to look through the details yourself and weigh both angles by reviewing the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond NovoCure?

If NovoCure has sharpened your focus on risk and reward, do not stop here. The Simply Wall Street Screener can surface other stocks that might better suit your approach.

- Spot potential value opportunities early by scanning screener containing 18 high quality undiscovered gems that combine quality fundamentals with less crowded investor attention.

- Strengthen your downside protection by reviewing 74 resilient stocks with low risk scores built around companies with more resilient risk profiles.

- Aim for a healthier income stream by checking 7 dividend fortresses that focus on companies offering higher dividend yields with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com