- In early July 2026, CAVA Group drew attention as slowing same-store sales growth, softer restaurant traffic, and more cautious analyst views contrasted with ongoing revenue expansion expectations.

- The episode also highlighted how earlier valuation concerns from InvestingPro’s Fair Value models were later echoed by shifting sentiment around CAVA’s growth quality.

- Now we’ll examine how cooling same-store sales trends influence CAVA’s existing investment narrative built around rapid expansion and margin improvement.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

CAVA Group Investment Narrative Recap

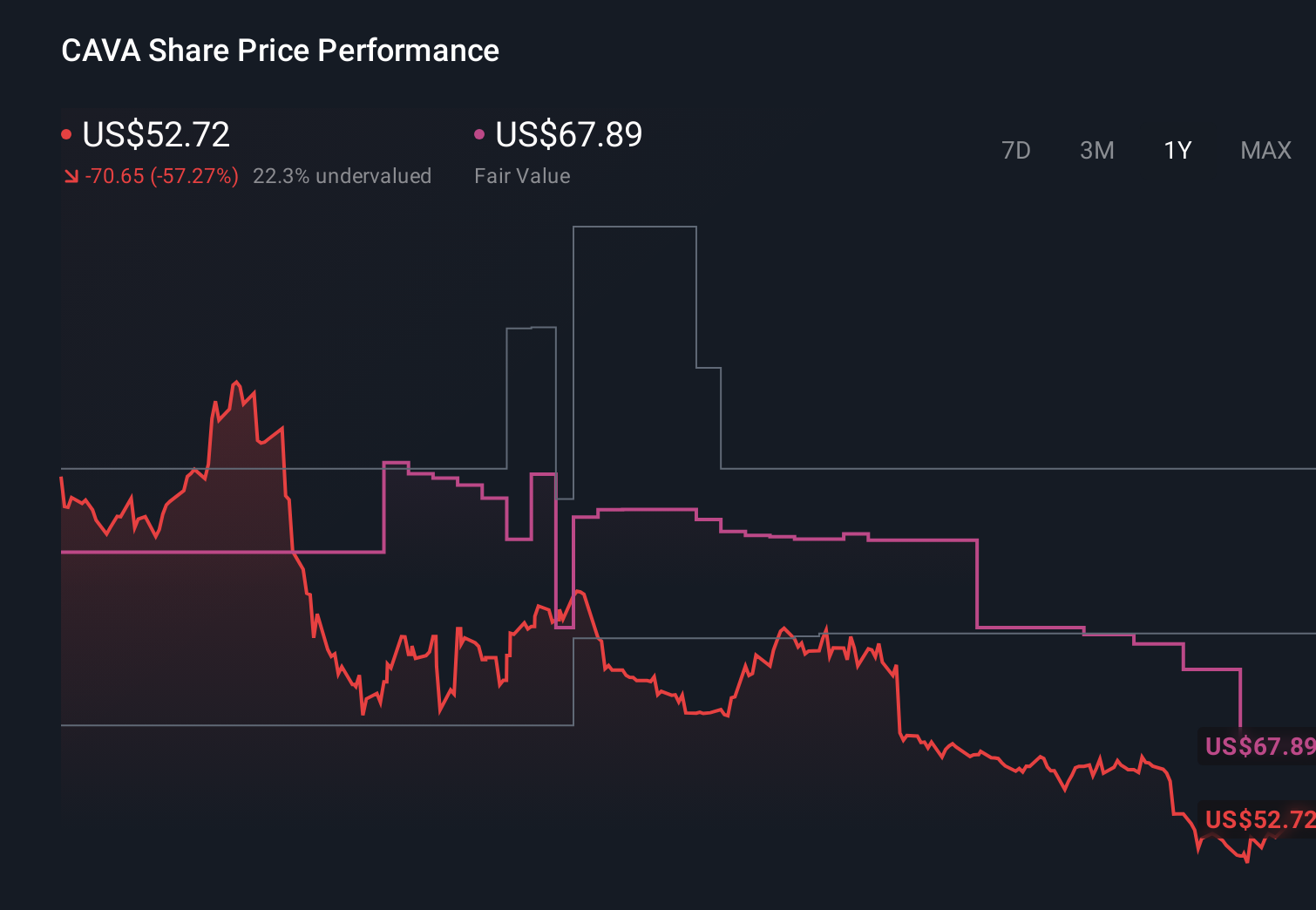

To own CAVA today, you likely need to believe its rapid unit expansion, menu innovation, and tech investments can offset a cooling in same-store sales and softer traffic. The recent slowdown directly touches the near term catalyst of sustaining strong same-restaurant sales, while also sharpening the key risk that high expectations, paired with a premium valuation, may be harder to support if traffic and margin trends remain under pressure.

Freedom Capital Markets’ Hold rating and US$95 price target captures this tension: it recognizes CAVA’s expansion runway and revenue growth forecasts, but also reflects caution around the quality and durability of that growth given slowing same-store sales and a 2 percent traffic decline, especially after InvestingPro’s models flagged valuation concerns well before the stock’s pullback.

Yet beneath CAVA’s growth story, there is a less obvious risk investors should be aware of around slowing in store traffic and how it could eventually intersect with...

Read the full narrative on CAVA Group (it's free!)

CAVA Group's narrative projects $2.1 billion revenue and $122.3 million earnings by 2029. This requires 21.8% yearly revenue growth and a $58.6 million earnings increase from $63.7 million today.

Uncover how CAVA Group's forecasts yield a $87.27 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts already expected revenue near US$2.2 billion and earnings around US$134.8 million by 2029, yet they were far more cautious about how persistent traffic softness and slower same restaurant sales might impact whether those numbers and today’s premium multiple still make sense for you.

Explore 5 other fair value estimates on CAVA Group - why the stock might be worth as much as 14% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com