- In late June 2026, Teradata Corporation was removed from several Russell 1000 and midcap indices and added to multiple Russell 2000, value, growth, and defensive indices, reflecting a broad reclassification of its benchmark footprint.

- This reshuffling can alter how index-tracking funds and benchmark-aware investors hold Teradata, potentially changing the stock’s ownership base and trading patterns over time.

- Next, we’ll examine how Teradata’s move from Russell 1000 to Russell 2000 benchmarks may influence its existing investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

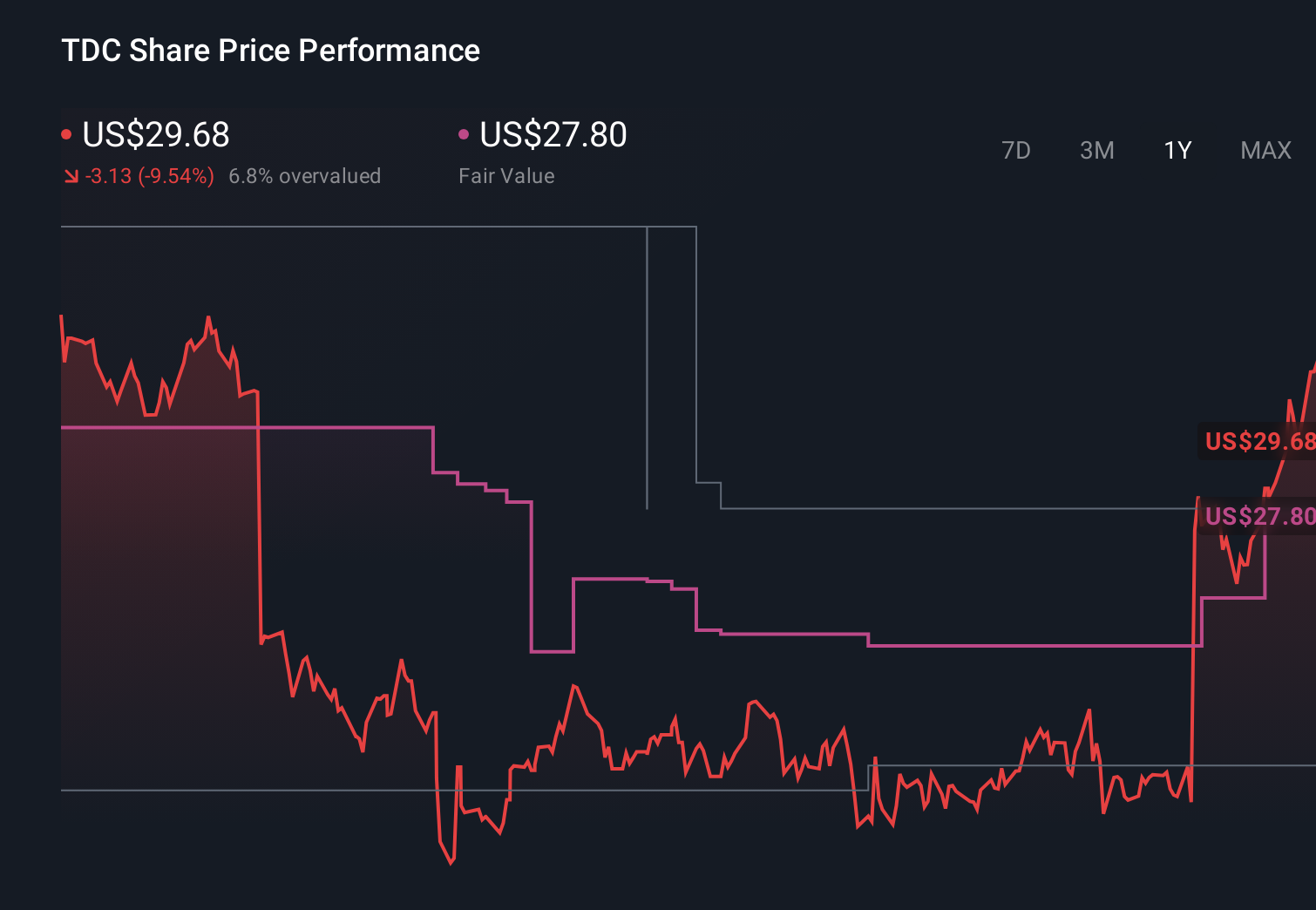

Teradata Investment Narrative Recap

To own Teradata today, you have to believe in its ability to stabilize revenue while shifting more of the business to cloud and AI-driven analytics. The index move from Russell 1000 to Russell 2000 may change who holds the stock, but it does not materially alter the core near term catalyst around execution in cloud ARR or the key risk of ongoing top line pressure and competitive intensity from larger cloud providers.

The recent US$400,000,000 revolving credit facility is especially relevant here, as it refreshes Teradata’s financial flexibility after replacing the prior agreement. While the facility itself does not change the investment thesis, it shapes how Teradata can fund product initiatives like the Autonomous Knowledge Platform and manage through any revenue volatility tied to the transition toward recurring cloud revenue.

However, against this backdrop, investors should also be aware that...

Read the full narrative on Teradata (it's free!)

Teradata’s narrative projects $1.7 billion revenue and $102.4 million earnings by 2029. This assumes essentially flat yearly revenue growth and an earnings decrease of $318.6 million from $421.0 million today.

Uncover how Teradata's forecasts yield a $34.88 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts see Teradata eventually earning about US$150.8 million on roughly US$1.8 billion of revenue, yet they still flag risks around cloud transition and competition that could look different after this index reshuffle and new credit capacity.

Explore 4 other fair value estimates on Teradata - why the stock might be worth just $34.88!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Teradata research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Teradata research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradata's overall financial health at a glance.

No Opportunity In Teradata?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com