Index removal puts RenaissanceRe Holdings in focus

RenaissanceRe Holdings (RNR) has come into focus after being removed from the Russell 1000 Dynamic Index, a technical event that can prompt mechanical selling and reshuffling among index-linked investors.

This index exit sits alongside an upcoming second quarter 2026 earnings release and conference call in late July, giving investors two near term reference points as they reassess how RenaissanceRe Holdings fits within their portfolios.

See our latest analysis for RenaissanceRe Holdings.

RenaissanceRe Holdings has seen strong positive momentum in recent months, with a 30 day share price return of 13.11% and year to date share price return of 19.85%, alongside a 1 year total shareholder return of 37.17% and 5 year total shareholder return of 125.03%. This suggests the index removal is being weighed against a longer record of value creation.

If this kind of price action has you thinking about what else is moving, it could be a good moment to broaden your watchlist with 20 top founder-led companies

After RenaissanceRe Holdings rallied and now sits just below the average analyst price target, while modelled intrinsic value points to a much larger gap, the real tension is this: is fair value closer to US$327 or that higher estimate range?

Most Popular Narrative: 0% Overvalued

The most followed narrative currently pegs RenaissanceRe Holdings at a fair value of about $325.47, which is almost exactly in line with the recent $326.29 close. This makes the key issue the assumptions that sit underneath that tight gap.

The analysts have a consensus price target of $325.47 for RenaissanceRe Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $401.0, and the most bearish reporting a price target of just $277.0.

Want to know what is driving that wide spread in views on RenaissanceRe Holdings? The narrative leans heavily on shifting revenue expectations, margin compression and a very specific earnings multiple a few years out. Curious how those moving parts combine to land almost exactly on today’s price?

Result: Fair Value of $325.47 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer property catastrophe pricing in regions like Florida and the Gulf of Mexico, along with the new 15% Bermuda corporate tax, could pressure RenaissanceRe Holdings' earnings assumptions.

Find out about the key risks to this RenaissanceRe Holdings narrative.

Another view on RenaissanceRe Holdings valuation

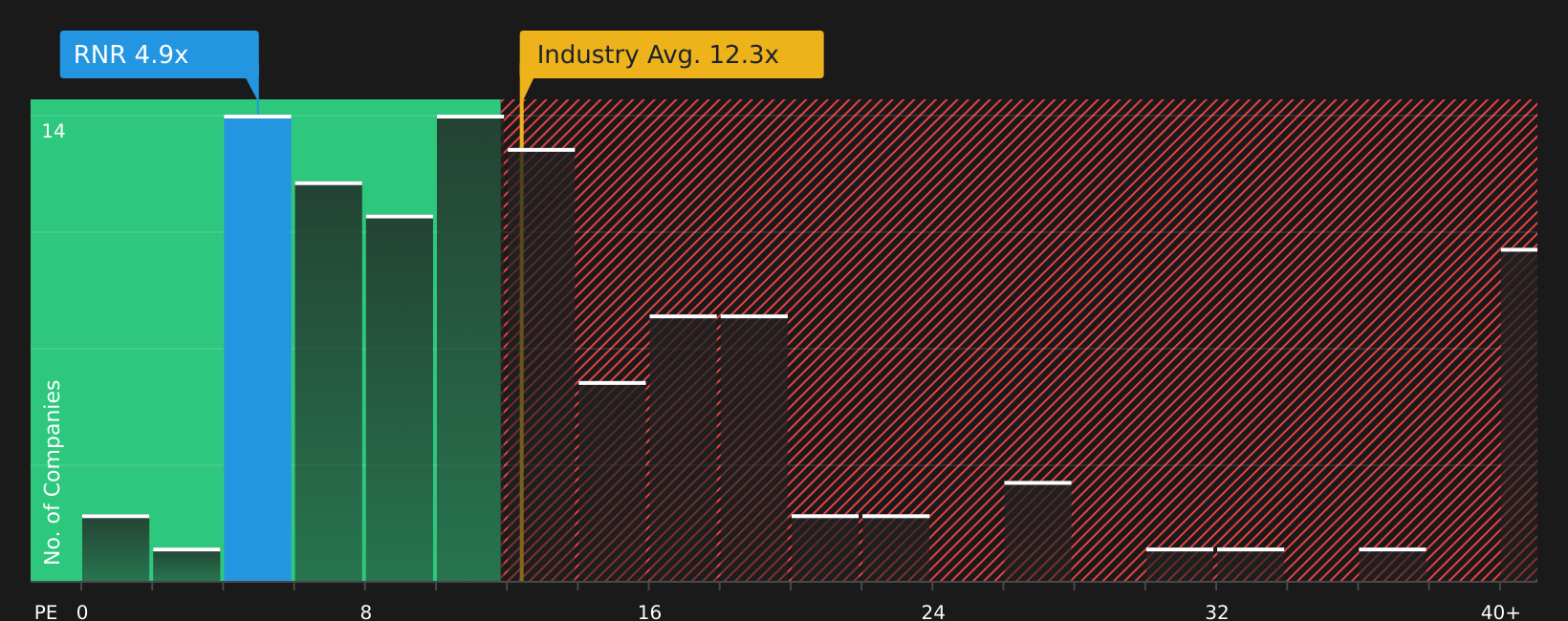

While the consensus narrative frames RenaissanceRe Holdings as roughly fairly priced around $325, the current P/E of 5.1x tells a different story. It sits well below the US Insurance industry at 12.4x, below peers at 7.9x, and even below a fair ratio of 8.4x, which the market could move toward over time. That gap cuts both ways, as it can reflect opportunity or simply higher perceived risk, so which side do you think fits better with your view of the next few years for this stock?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of bullish and cautious signals on RenaissanceRe Holdings feels evenly balanced, treat it as a prompt to review the numbers yourself and move quickly while sentiment is still split. Then weigh both sides in detail through the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond RenaissanceRe Holdings?

RenaissanceRe Holdings might be front of mind today, but the next opportunity could already be moving. Use the screener to quickly surface fresh ideas that match your style and risk comfort.

- Target potential upside by zeroing in on companies that combine quality fundamentals with appealing valuations through the screener containing 18 high quality undiscovered gems.

- Strengthen the defensive side of your portfolio by focusing on companies highlighted in the 73 resilient stocks with low risk scores that aim for more resilient performance.

- Build a watchlist of companies with steady financial footing using the solid balance sheet and fundamentals stocks screener (47 results) before the market pays closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com