Cognex (CGNX) is back in focus after coverage around its new OneVision platform, which supports AI-based inspection across factories, and growing attention on whether the stock’s valuation premium is justified.

See our latest analysis for Cognex.

The recent OneVision launch and media attention have arrived alongside sharp share price moves. Cognex’s 30-day share price return of 11.48% and 90-day share price return of 31.17% have contributed to an 83.59% year-to-date share price return, while the 1-year total shareholder return of 114.34% contrasts with a weaker 5-year total shareholder return that declined 18.86%. This suggests that momentum has picked up recently as investors reassess growth potential and valuation risk.

If you are looking beyond Cognex to see what else is moving in factory automation and AI infrastructure, it is worth checking out 29 robotics and automation stocks as a next step.

After a move like Cognex has just seen, some investors will want to lock in a position quickly, while others prefer to wait for a pullback. How does the current valuation stack up against that choice?

Most Popular Narrative: 11.1% Undervalued

The most followed narrative currently points to a fair value of $76.25 for Cognex versus a last close of $67.80, which implies room between price and modeled worth before even considering how the story could evolve.

Strong growth in logistics, packaging, and consumer electronics end markets, driven by investments in e-commerce, traceability, and quality automation, is broadening Cognex's customer base and reducing reliance on cyclical sectors. This diversification supports more stable, long-term revenue growth.

Want to see what is sitting underneath that fair value for Cognex? The narrative leans on faster earnings compounding, firmer margins and a richer mix of AI-driven revenue. Curious which assumptions really move the model, and how far they stretch current profitability trends?

Result: Fair Value of $76.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, for Cognex this narrative can be challenged if machine vision hardware continues to face pricing pressure or if AI software adoption progresses more slowly than analysts expect.

Find out about the key risks to this Cognex narrative.

Another View on Cognex Valuation

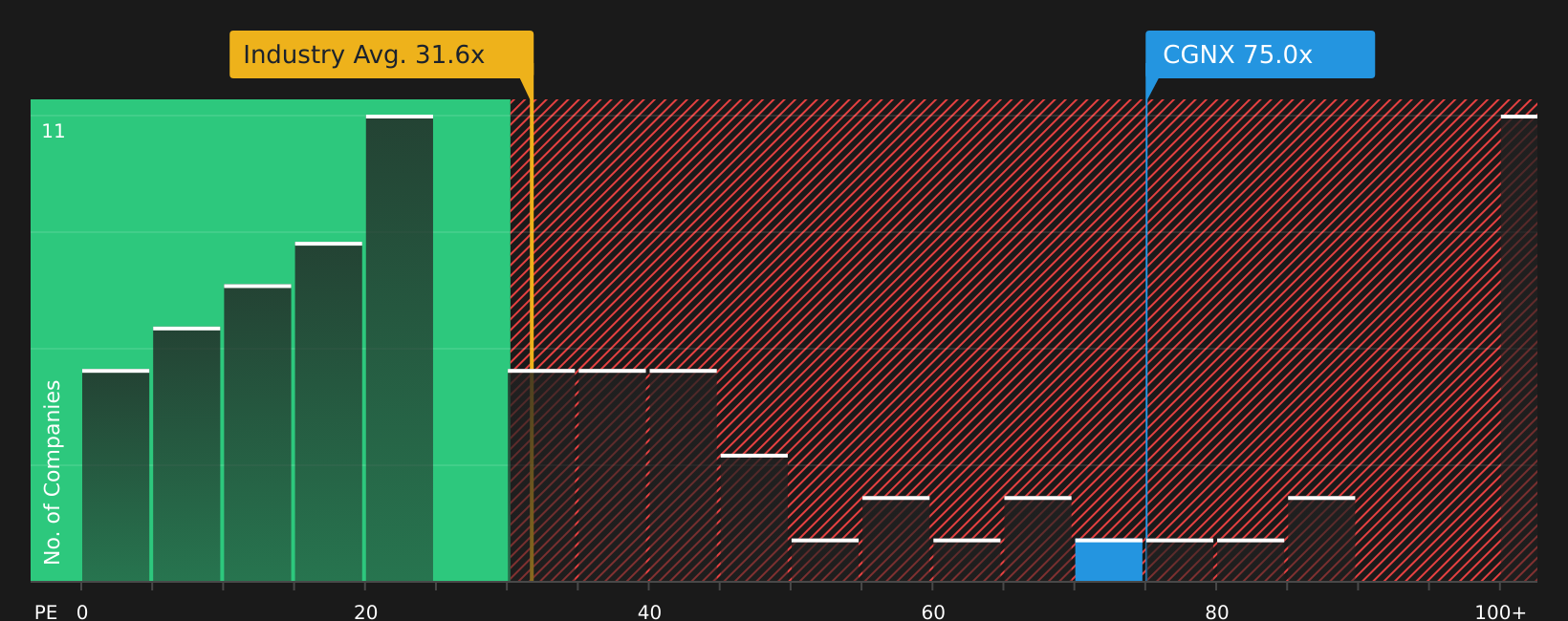

While the fair value narrative points to Cognex trading about 11.1% below a modeled $76.25, the current P/E of 79.2x tells a more cautious story. That multiple is far above the Electronic industry average of 31.9x, the peer average of 59.6x, and the fair ratio of 42.1x. This spread suggests the share price could be more exposed if growth or margins fall short of expectations.

For investors weighing this richer P/E against the earlier fair value estimate, the key question is whether Cognex can deliver enough earnings growth to close that gap, or whether the valuation could instead drift back toward the fair ratio over time and reset expectations.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seen enough debate around Cognex to sense how split sentiment is becoming? Act quickly to review the data for yourself and weigh up the 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Cognex?

Do not stop with Cognex when there are other opportunities to review. Use these focused screens to spot ideas you might regret missing later.

- Target potential value by reviewing companies our models flag as overlooked using the 44 high quality undervalued stocks.

- Strengthen your income watchlist by scanning for higher yielding opportunities with the 7 dividend fortresses.

- Prioritize resilience by focusing on companies highlighted in the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com