- In late June 2026, Laureate Education, Inc. was removed from several Russell value and small-cap indices, including the Russell 3000 Value, Russell 2000 Value, Russell 2500 Value, Russell 3000E Value, and Russell Small Cap Comp Value benchmarks.

- This broad index exclusion matters because it can drive sizable portfolio rebalancing by index-tracking funds, potentially altering Laureate’s shareholder base and trading liquidity.

- We’ll now examine how Laureate’s removal from multiple Russell value benchmarks interacts with its existing investment narrative and outlook.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

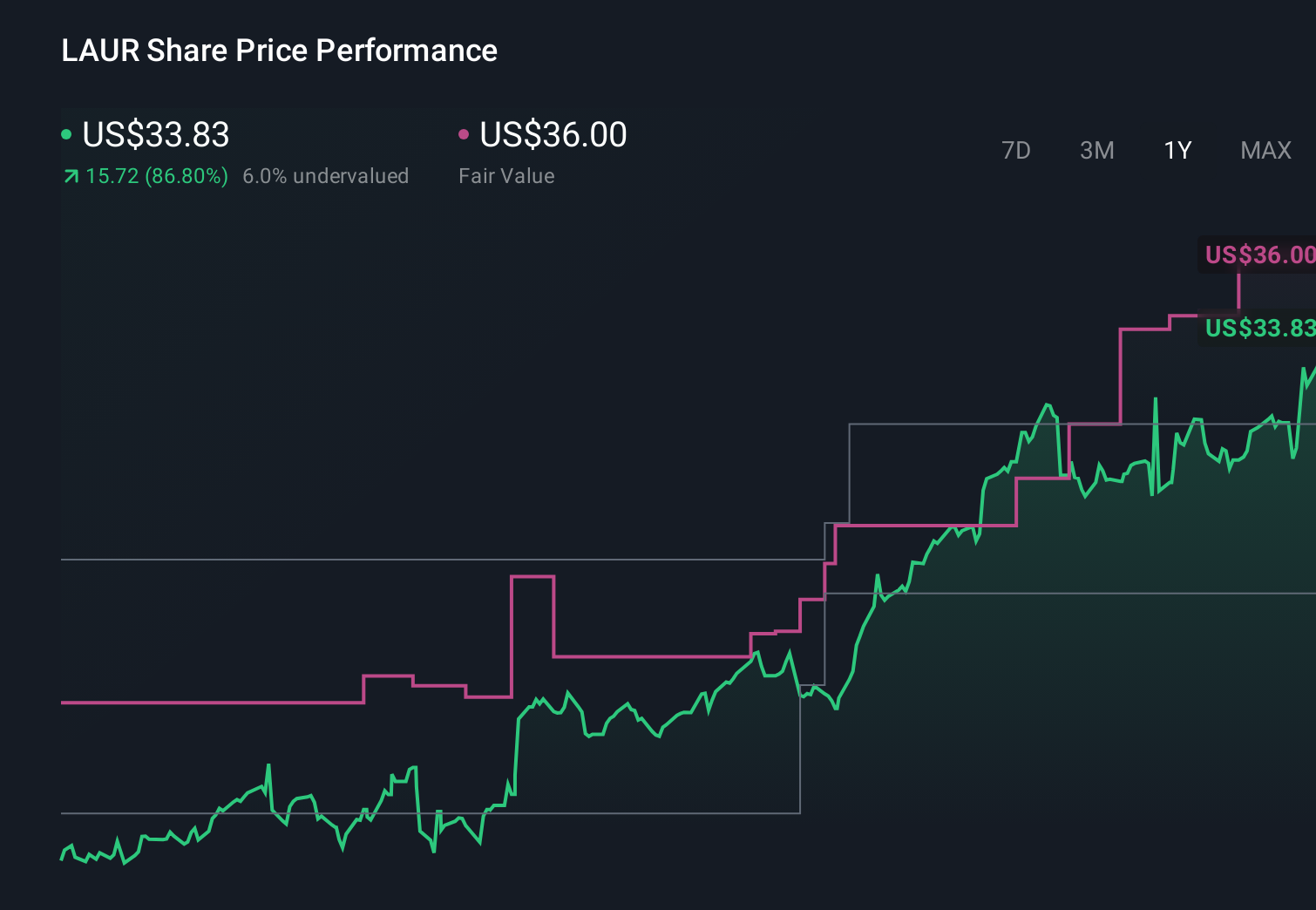

Laureate Education Investment Narrative Recap

To own Laureate, you have to believe its focus on Mexico and Peru, combined with expanding digital programs, can translate into resilient enrollment and earnings despite concentrated country risk and rising online competition. The broad removal from Russell value and small cap indices may create short term trading pressure or shifts in the shareholder base, but it does not directly change the company’s core operational catalyst right now, which is execution against its 2026 revenue guidance and upcoming Q2 results.

The most relevant recent announcement, in my view, is Laureate’s reaffirmed full year 2026 revenue guidance of US$1,890 million to US$1,905 million, alongside continued buybacks. This guidance frames the key near term catalyst around whether reported enrollment and pricing trends in Mexico and Peru support those targets, while the buyback program, with US$324 million already deployed, interacts with potential index driven selling by absorbing shares and influencing liquidity and per share metrics.

Yet beneath the index changes, one risk investors should be aware of is how concentrated exposure to Mexico and Peru could interact with...

Read the full narrative on Laureate Education (it's free!)

Laureate Education's narrative projects $2.3 billion revenue and $373.6 million earnings by 2029. This requires 9.1% yearly revenue growth and about a $93.8 million earnings increase from $279.8 million today.

Uncover how Laureate Education's forecasts yield a $40.25 fair value, in line with its current price.

Exploring Other Perspectives

Compared with the baseline story, the lowest analysts were already more cautious, assuming only 6.9% annual revenue growth to about US$2.1 billion and earnings near US$328.6 million by 2029, so you should weigh whether June’s index removal could reinforce that more pessimistic view or ultimately prove those concerns too harsh.

Explore 3 other fair value estimates on Laureate Education - why the stock might be worth 8% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Laureate Education research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Laureate Education research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Laureate Education's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com