Northern Trust (NTRS) is back in focus after securing fresh administration, custody and depositary mandates from Invesco and TirNua Capital Partners, highlighting its role in asset management and infrastructure fund servicing.

See our latest analysis for Northern Trust.

Northern Trust's recent client wins come on top of strong share price momentum, with a 30.05% year to date share price return and a 44.16% total shareholder return over one year, while multi year total shareholder returns suggest sustained compounding.

If these fund servicing mandates have caught your attention, it could be a good moment to broaden your watchlist and check out 20 top founder-led companies

Northern Trust now trades close to analyst targets after a strong run, yet still shows a small discount to some fair value estimates. Is the recent optimism overheating the stock, or is the market still underpricing it?

Most Popular Narrative: 3.4% Overvalued

Northern Trust last closed at $181.14, a touch above the most followed fair value estimate of $175.23 that is built on detailed earnings and margin forecasts.

The company's recent organic growth and margin expansion are largely attributed to near-term operational efficiencies and balance sheet optimization (notably lower expense growth and improved operating leverage), yet investors may be overestimating the persistence of these improvements in light of ongoing industry fee pressure from the growing shift to passive investing and ETFs, which is likely to constrain long-term revenue growth and profit margins.

Curious what sits underneath that fair value for Northern Trust? The narrative leans heavily on specific revenue assumptions, margin rebuild and a tighter share count. The exact mix of these inputs matters more than the headline target.

Result: Fair Value of $175.23 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Northern Trust could still surprise this narrative if its alternatives platform scales faster than expected, or if automation efforts hold margins higher than current assumptions.

Find out about the key risks to this Northern Trust narrative.

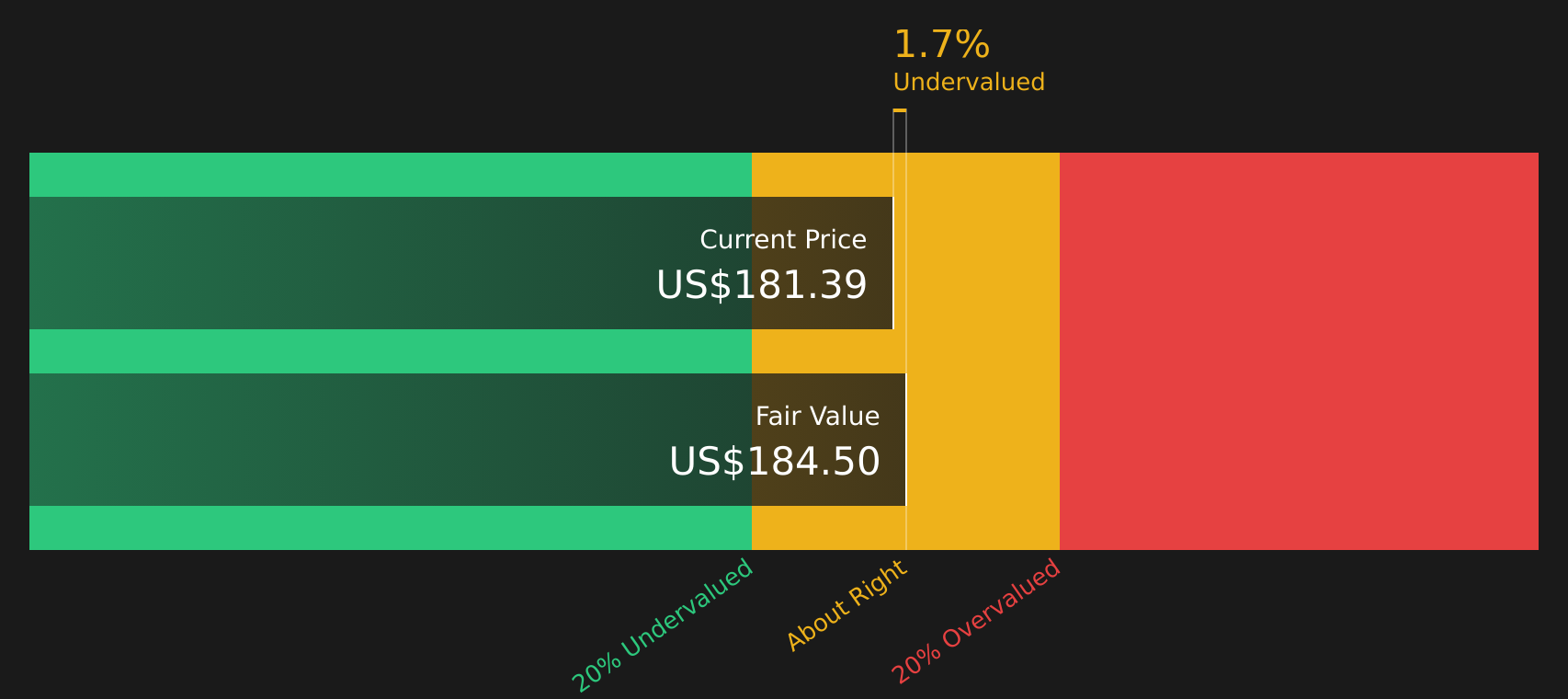

Another View On Northern Trust's Valuation

While the most followed fair value narrative for Northern Trust lands at $175.23 and calls the stock 3.4% overvalued, the Simply Wall St DCF model points in a slightly different direction, with an estimated future cash flow value of $184.58 that sits above the current $181.14 share price. For you as an investor, that mixed picture raises a simple question: which set of assumptions feels more realistic for how Northern Trust will actually earn and return cash over time?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northern Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Northern Trust looking mixed, this is a moment to move quickly, review the numbers yourself, and weigh both sides of the story using 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Northern Trust?

If Northern Trust has you thinking more seriously about your portfolio, do not stop here. Use these tools to uncover other opportunities that could fit your goals.

- Target resilient income by scanning companies with strong yields and robust fundamentals using the 8 dividend fortresses.

- Hunt for quality at a reasonable price by filtering for companies that look attractively priced on core metrics with the 41 high quality undervalued stocks.

- Prioritize stability by focusing on companies with healthier finances and lower perceived risk scores through the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com