In the last week, the United States market has stayed flat, yet over the past 12 months, it has experienced a notable rise of 20%, with earnings forecasted to grow by 18% annually. In this context, identifying stocks that may be undervalued can provide opportunities for investors seeking to capitalize on potential growth while considering current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Rayonier (RYN) | $21.60 | $42.86 | 49.6% |

| Q2 Holdings (QTWO) | $53.41 | $103.09 | 48.2% |

| Procore Technologies (PCOR) | $44.04 | $86.98 | 49.4% |

| Natera (NTRA) | $283.80 | $554.53 | 48.8% |

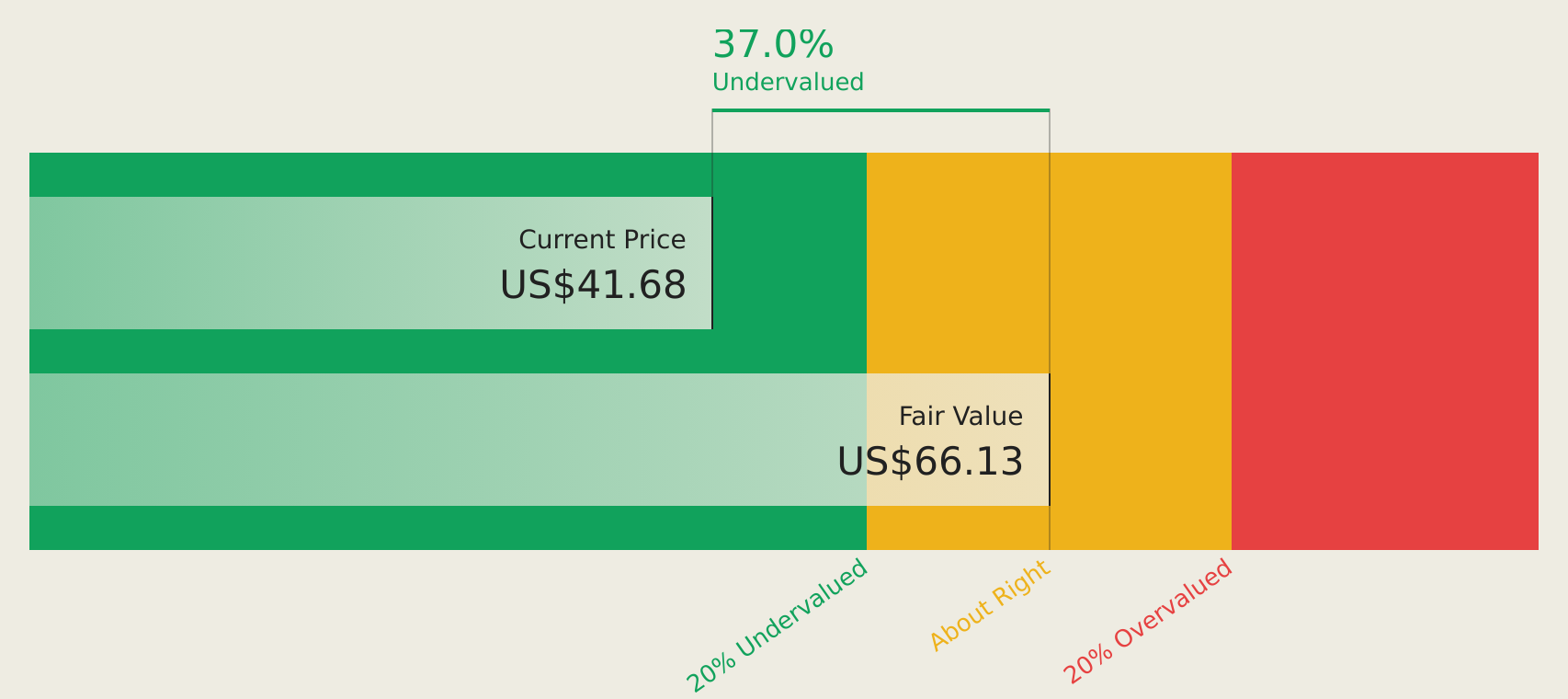

| Klaviyo (KVYO) | $17.00 | $33.62 | 49.4% |

| Janus Living (JAN) | $29.38 | $57.58 | 49% |

| Genuine Parts (GPC) | $128.66 | $249.25 | 48.4% |

| Esquire Financial Holdings (ESQ) | $120.48 | $238.84 | 49.6% |

| Betterware de MéxicoP.I. de (BWMX) | $18.44 | $36.26 | 49.1% |

| Beacon Financial (BBT) | $30.24 | $60.42 | 50% |

Below we spotlight a couple of our favorites from our exclusive screener.

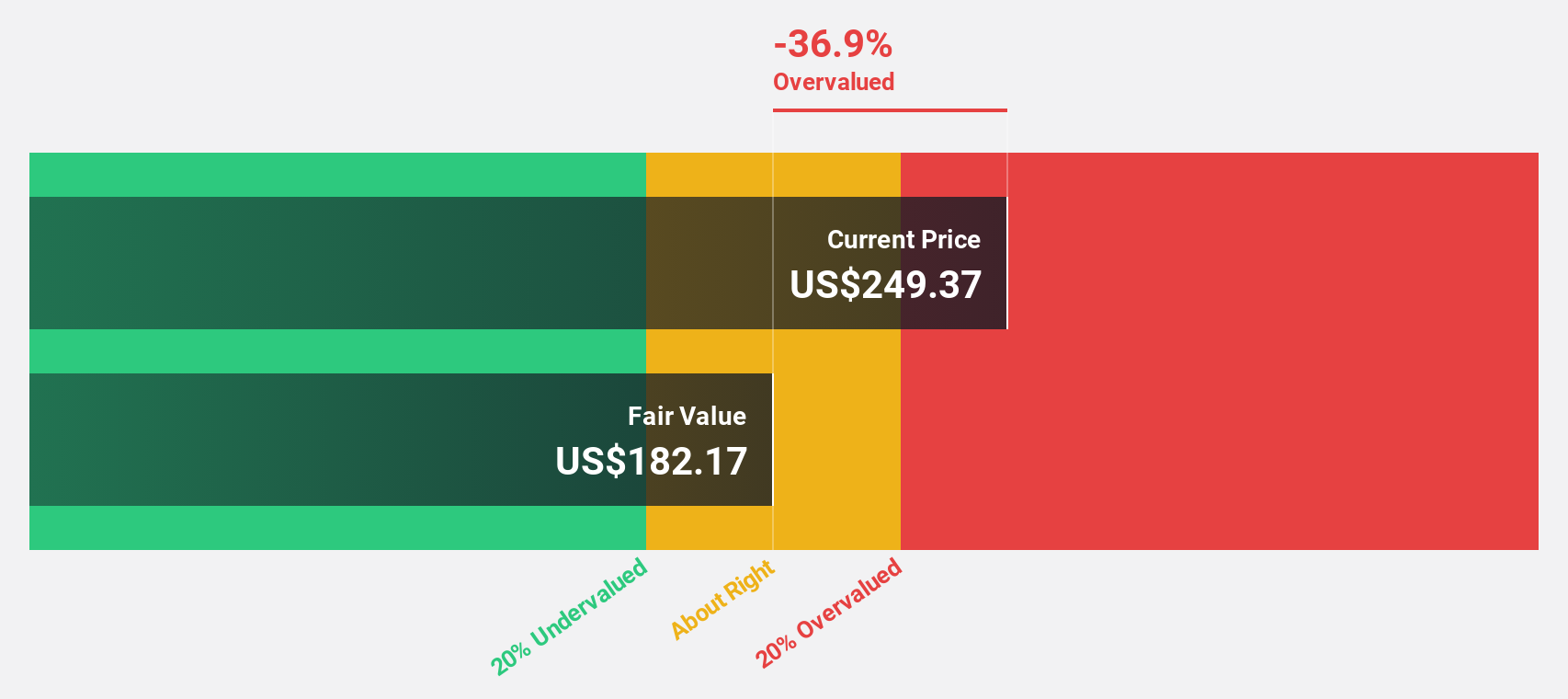

Broadcom (AVGO)

Overview: Broadcom Inc. is a global company that designs, develops, and supplies semiconductor devices and infrastructure software solutions, with a market cap of approximately $1.71 trillion.

Operations: Broadcom's revenue is primarily derived from two segments: Infrastructure Software, contributing $27.70 billion, and Semiconductor Solutions (including Intellectual Property Licensing), generating $47.76 billion.

Estimated Discount To Fair Value: 18.2%

Broadcom's earnings are expected to grow significantly, outpacing the US market. The stock is trading at a good value, 18.2% below its estimated fair value of US$457.08 based on discounted cash flow analysis. However, significant insider selling and high debt levels could be concerns for investors. Recent partnerships with Apple and OpenAI may bolster future revenue growth, while its collaboration with Meta supports AI infrastructure development through 2029.

- Our earnings growth report unveils the potential for significant increases in Broadcom's future results.

- Delve into the full analysis health report here for a deeper understanding of Broadcom.

Goosehead Insurance (GSHD)

Overview: Goosehead Insurance, Inc. operates as a holding company for Goosehead Financial, LLC, providing personal lines insurance agency services in the United States with a market cap of approximately $1.88 billion.

Operations: The company's revenue primarily stems from its insurance distribution segment, which generated $382.20 million.

Estimated Discount To Fair Value: 22.6%

Goosehead Insurance is trading at 22.6% below its estimated future cash flow value of US$68.46, suggesting undervaluation based on cash flows. Revenue and earnings growth are expected to surpass the US market, with earnings projected to rise significantly at 21.7% annually over three years. Despite a high debt level and recent index exclusion, strategic executive appointments could enhance operational efficiency and technological advancements, potentially supporting long-term financial performance improvements.

- The growth report we've compiled suggests that Goosehead Insurance's future prospects could be on the up.

- Get an in-depth perspective on Goosehead Insurance's balance sheet by reading our health report here.

Flowserve (FLS)

Overview: Flowserve Corporation designs, manufactures, distributes, and services industrial flow management equipment across various regions including the United States, Canada, Mexico, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of approximately $9.25 billion.

Operations: The company's revenue is primarily derived from its Flow Control Division, contributing $1.47 billion, and the Flowserve Pump Division, contributing $3.20 billion.

Estimated Discount To Fair Value: 12.2%

Flowserve is trading at 12.2% below its estimated future cash flow value of US$85.07, indicating potential undervaluation. The company's earnings are projected to grow significantly at 21.3% annually over the next three years, outpacing the broader US market growth rate. Recent operational improvements and strategic acquisitions, such as Trillium Flow Technologies' Valves Division, bolster its cash generation capacity despite slower revenue growth forecasts compared to peers and ongoing investor activism challenges.

- Insights from our recent growth report point to a promising forecast for Flowserve's business outlook.

- Click to explore a detailed breakdown of our findings in Flowserve's balance sheet health report.

Turning Ideas Into Actions

- Click this link to deep-dive into the 149 companies within our Undervalued US Stocks Based On Cash Flows screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com