- In early July 2026, InterDigital, Inc. secured a favorable ruling from the Mannheim Local Division of the Unified Patent Court against The Walt Disney Company, winning an injunction across 11 EU countries over a patented HEVC video encoding technology, while also recently signing a patent license agreement with Amazon expected to provide recurring revenue.

- Together, the legal win and Amazon license highlight how InterDigital’s intellectual property portfolio can translate into enforceable rights and long-term licensing income in video streaming and beyond.

- We’ll now explore how the Disney injunction, in particular, could influence InterDigital’s investment narrative around patent strength and future licensing visibility.

Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe that its patent portfolio can keep converting into stable, enforceable licensing income across wireless, video, and connected devices. The Disney injunction and Amazon agreement both reinforce that story in the near term, but the key catalyst remains how consistently InterDigital can turn disputes into signed licenses, while the biggest risk is that legal and regulatory shifts eventually weaken the value or enforceability of its patents.

Among recent developments, the Amazon patent license stands out as most closely tied to the Disney ruling. Amazon’s agreement, which covers services like Prime Video, sits alongside the new EU-wide injunction as another proof point that InterDigital’s video and wireless IP can be both enforced and monetized across large streaming and device ecosystems, an outcome that matters directly for the company’s licensing pipeline and perceived revenue visibility.

Yet investors should also weigh how growing scrutiny of aggressive patent enforcement could affect InterDigital’s ability to keep securing outcomes like the Disney injunction that investors should be aware of...

Read the full narrative on InterDigital (it's free!)

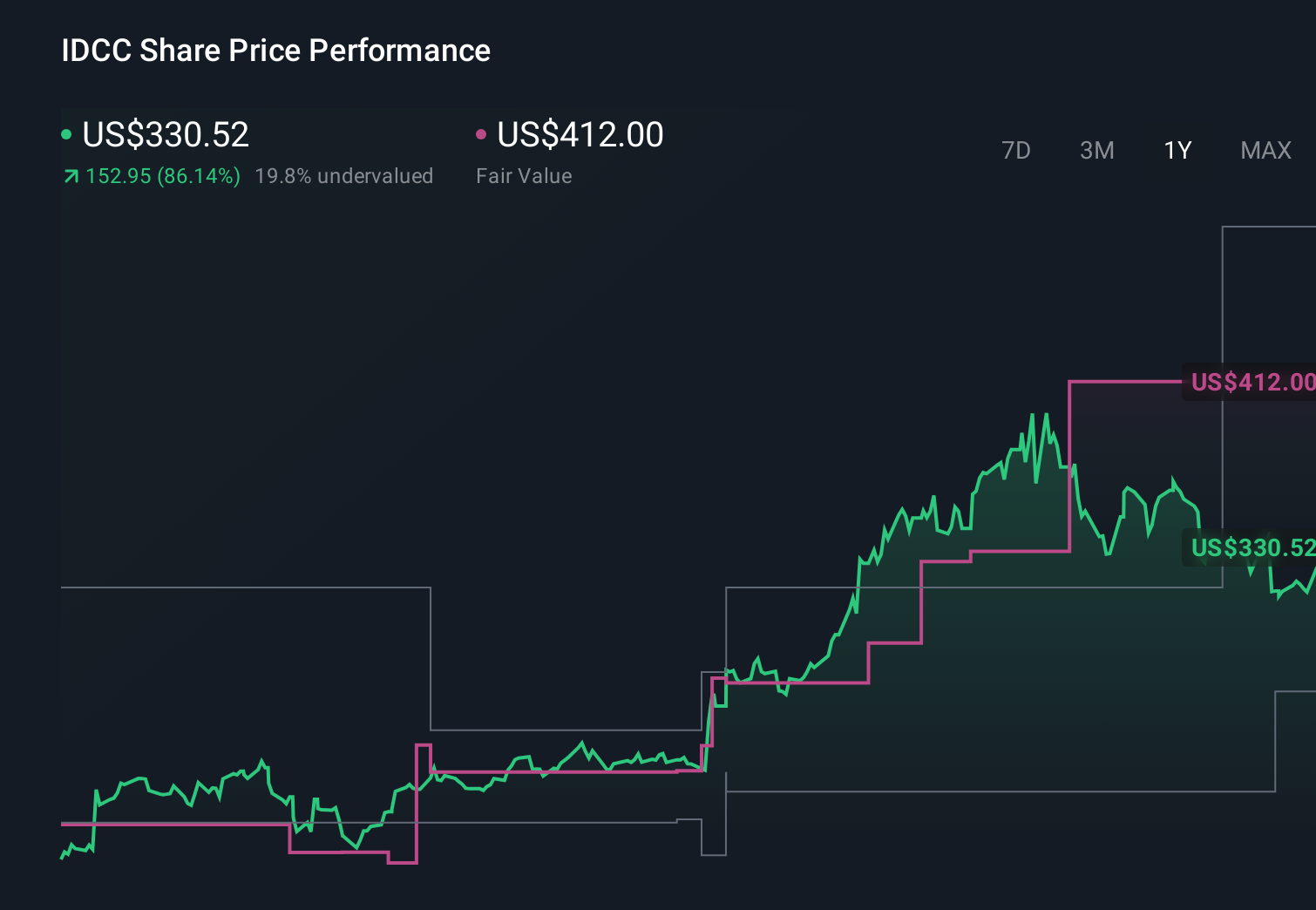

InterDigital's narrative projects $824.6 million revenue and $350.8 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 64% upside to its current price.

Exploring Other Perspectives

While consensus already saw InterDigital earning about US$487.6 million by 2029, the most optimistic analysts assumed strong recurring cash flows and fewer structural threats to IP monetization than the growing regulatory and “patent troll” concerns that the Disney case could bring into sharper focus, so it is worth considering how those forecasts might shift.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth as much as 64% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com