Agilysys (AGYS) is back in focus after Fitzroy Island Resort reported that a unified Agilysys hospitality platform replaced a patchwork of legacy systems, delivering efficiency gains and strong staff acceptance across core property operations.

See our latest analysis for Agilysys.

Agilysys shares have recently shifted back into the spotlight, with a 30 day share price return of 25.4% and a 90 day gain of 61.85%. This comes even though the year to date share price return is down 3.9% and the 1 year total shareholder return is down 2.96%, while the 3 and 5 year total shareholder returns of 61.17% and 92.81% point to stronger results over a longer horizon.

If this kind of operational progress has your attention, it could be a good moment to see what else is emerging across hospitality tech and services via the 20 top founder-led companies

After a sharp move in Agilysys and a share price still below both intrinsic estimates and analyst targets, the tension is clear: is the market rightly cautious, or is it underpricing what investors are already seeing in the field?

Most Popular Narrative: 11% Overvalued

Agilysys last closed at $111, while the most followed narrative anchors fair value at $100. The current price sits above that reference point and sharpens the focus on what is being priced in.

The assumed bearish price target for Agilysys is $100.0, which represents up to two standard deviations below the consensus price target of $127.33. This valuation is based on what can be assumed as the expectations of Agilysys's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

Want to see what underpins that lower fair value for Agilysys? The narrative leans on firm revenue expansion, rising profitability and a rich future earnings multiple. Curious which specific growth and margin assumptions support that outcome and how they compare with current analyst targets?

Result: Fair Value of $100 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if Agilysys continues converting its hospitality footprint into higher subscription revenue and margins, or if international expansion accelerates, this bearish narrative could soften.

Find out about the key risks to this Agilysys narrative.

Another View: Agilysys Through the SWS DCF Lens

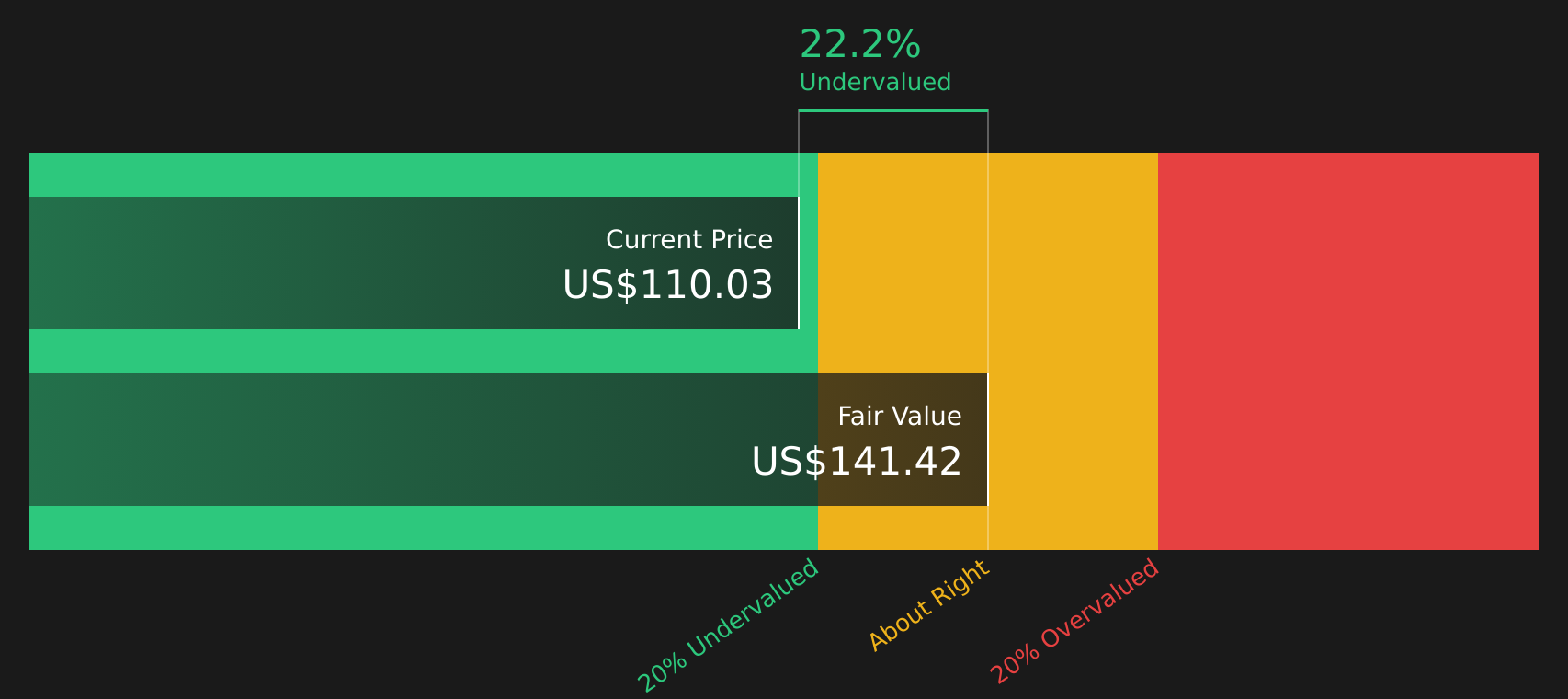

The bearish narrative pegs Agilysys at $100, yet the SWS DCF model points in a different direction, with an estimated future cash flow value of $140.69 and the stock at $111 trading about 21.1% below that mark. When one framework says overvalued and another flags a discount, which do you trust more for your own process?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Agilysys for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing both caution and optimism around Agilysys in the numbers and narratives, it makes sense to move quickly, review the underlying data yourself, and weigh 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Agilysys?

If Agilysys has sharpened your focus, do not stop there. Broaden your watchlist with fresh ideas that could reshape how you think about portfolio construction.

- Target potential value standouts by scanning companies highlighted in the 41 high quality undervalued stocks to see which stocks currently screen as attractively priced against their fundamentals.

- Strengthen your focus on financial resilience by reviewing the solid balance sheet and fundamentals stocks screener (47 results) and identify businesses with support from cleaner balance sheets and healthier funding profiles.

- Spot opportunities others might be overlooking by checking the screener containing 18 high quality undiscovered gems and see which underfollowed stocks still show robust underlying numbers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com