- In recent weeks, Citigroup Inc. has expanded its funding base with multiple new senior unsecured fixed-rate note issuances across maturities out to 2046, while also being admitted as a clearing member of London Precious Metals Clearing Limited, adding Loco London settlement services for gold, silver, platinum and palladium.

- These moves, alongside the appointment of Michael Yannell to lead hedge funds within Citi’s wealth division and rising expectations for second-quarter earnings, point to a concerted push to deepen higher-fee businesses and enhance the bank’s global markets infrastructure.

- We’ll now examine how Citi’s expanded role in London precious metals clearing shapes the existing investment narrative around its wealth and institutional platforms.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Citigroup Investment Narrative Recap

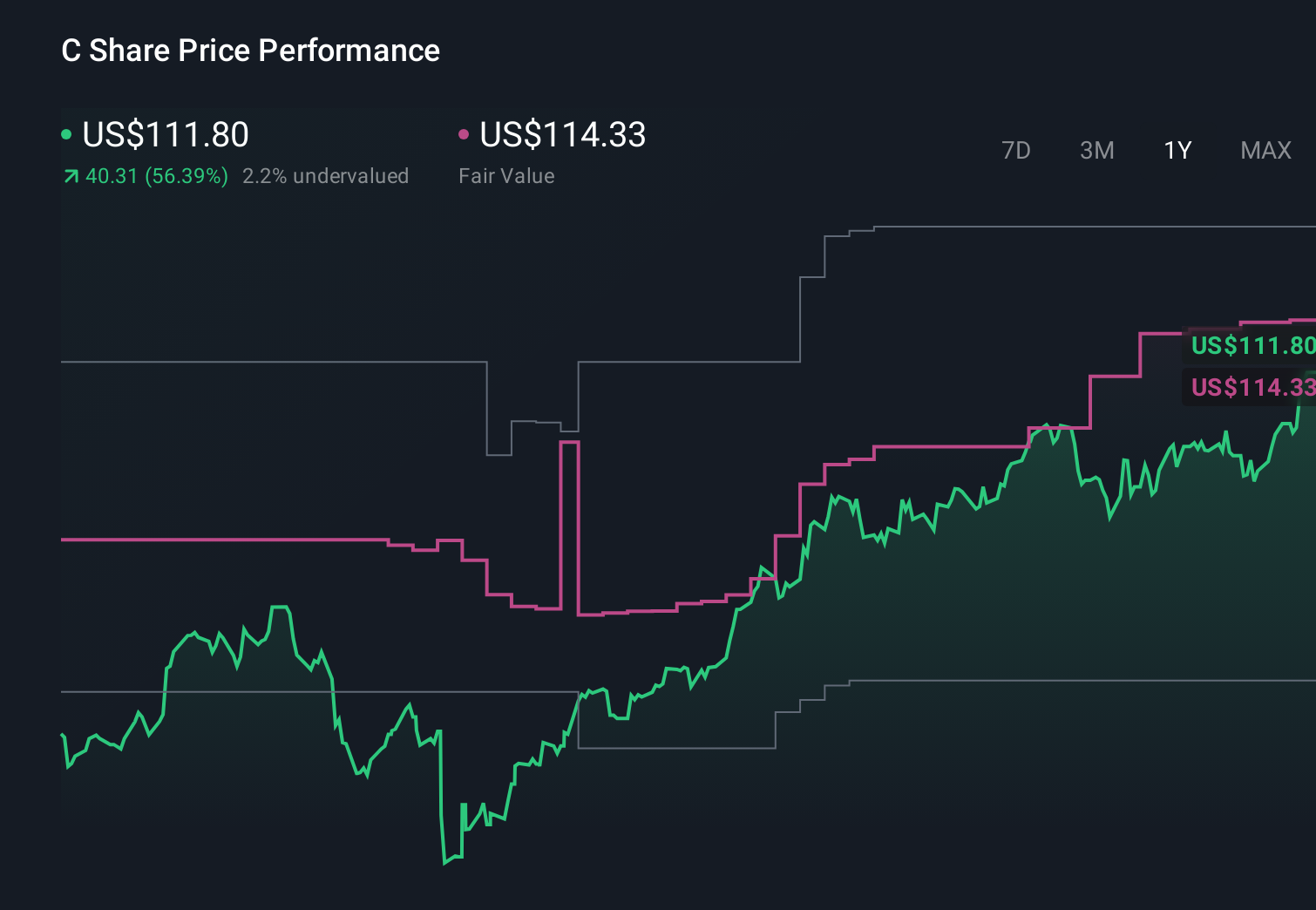

To own Citigroup today, you need to believe its simplification and global scale can steadily lift returns despite elevated transformation costs and regulatory scrutiny. In the near term, the key catalyst is execution around earnings and efficiency, while the biggest risk is that ongoing compliance and technology spending keep margins under pressure. The latest funding and London precious metals clearing news modestly support Citi’s markets and fee story, but do not fundamentally change that risk balance.

The most relevant recent development here is Citi’s admission as a clearing member of London Precious Metals Clearing Limited, adding Loco London settlement. This directly ties into its institutional and wealth ambitions by broadening precious metals capabilities for global clients. How much this clearing role ultimately contributes to fee income and differentiates Citi’s markets platform could matter for how investors weigh the upside from its wealth and markets franchises against the drag from continued restructuring.

Yet, against these potential upsides, investors should also be aware that Citi’s high transformation spend and regulatory overhang could still...

Read the full narrative on Citigroup (it's free!)

Citigroup’s narrative projects $102.4 billion revenue and $21.7 billion earnings by 2029. This requires 9.2% yearly revenue growth and about a $7.0 billion earnings increase from $14.7 billion today.

Uncover how Citigroup's forecasts yield a $146.93 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts are far more cautious than consensus, even before this news, assuming revenue of about US$100.4 billion and earnings of roughly US$20.6 billion by 2029, so if you see Citi’s new London precious metals clearing role as a meaningful fee catalyst, it is worth asking whether that more pessimistic view of elevated costs and pressured margins still holds up for you.

Explore 9 other fair value estimates on Citigroup - why the stock might be worth just $138.08!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com