Agilysys stock has almost doubled over the past 5 years, yet the valuation checks send a mixed message, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to roughly 19.8% upside while earnings based multiples suggest the shares screen as expensive.

- Over 5 years, Agilysys has returned about 98.6%, which puts current pricing in the context of a strong long term gain that investors now have to justify on fundamentals.

- Recent attention on Agilysys as a growth stock, backed by strong subscription trends, can support higher cash flow expectations, but any disappointment in how that growth translates into sustained free cash generation may weigh heavily on what investors are willing to pay.

- On Simply Wall St’s broader checks, Agilysys scores 1 out of 6, which leans expensive overall even though the DCF estimate screens the shares as undervalued.

The stock’s next move may depend on whether the intrinsic value case or the richer market multiples turn out to be the better guide for Agilysys at today’s price.

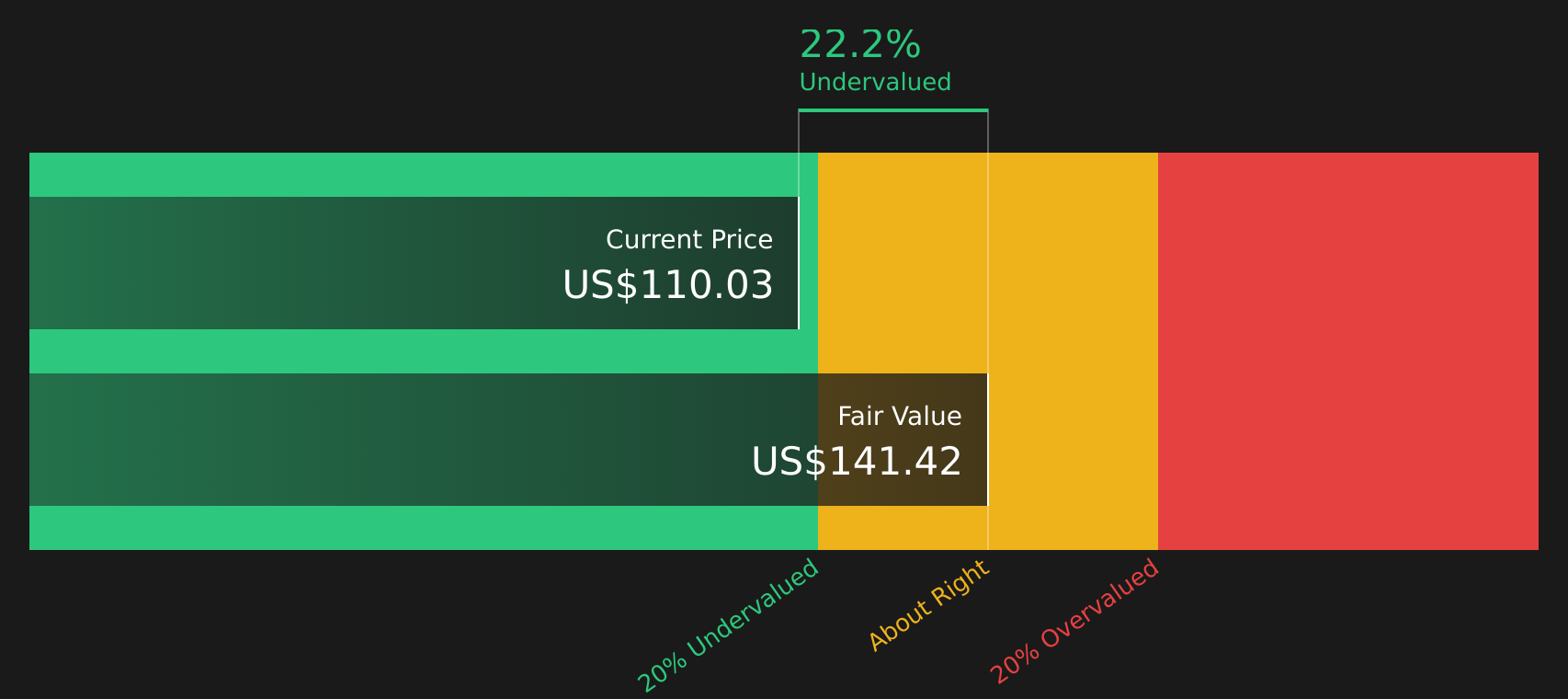

Does Agilysys Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model values Agilysys by projecting its future free cash generation and discounting it back to today. For Agilysys, the latest twelve month Free Cash Flow stands at about $65.1 million, and the model assumes growing cash flows over time rather than a flat or shrinking profile.

On these inputs, the 2 Stage Free Cash Flow to Equity model points to an intrinsic value of about $140.71 per share. Compared with the current market price, that implies the stock is roughly 19.8% below what its projected cash flows suggest. The recent recognition of Agilysys as one of the “Best Growth Stocks to Buy and Hold for the Next Decade” helps explain why investors are prepared to pay a premium; however, the DCF output still indicates room between price and estimated value.

Overall, the Discounted Cash Flow (DCF) workup suggests Agilysys stock currently looks undervalued relative to its projected cash generation.

Our Discounted Cash Flow (DCF) analysis suggests Agilysys is undervalued by 19.8%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Does Agilysys Look Pricey on Earnings?

The P/E ratio is a useful metric for Agilysys, as earnings are a key focus for software investors comparing profitability across peers. Agilysys currently trades on a P/E of about 81.7x, which is materially higher than both the software industry average of roughly 28.8x and the peer group average of about 49.6x.

According to Simply Wall St’s model, a tailored fair P/E for Agilysys, given its profile and risk, is around 32.7x, which is far below the current 81.7x. That gap indicates the market is paying a substantial premium for Agilysys stock compared with what this framework suggests might be reasonable based on typical earnings expectations for companies in a similar position.

Overall, Agilysys stock appears overvalued on its P/E multiple compared with both its industry and the model’s fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The Agilysys Narrative: What Would Justify Today's Price?

Simply Wall St Narratives try to close the gap between Agilysys' cash flow based upside and its rich earnings multiple by spelling out which paths for growth, margins and earnings would justify meaningfully higher or lower prices than today. They sit on the Community page. Each one treats fair value as a thesis about how Agilysys' business could develop that you can revisit over time, rather than a one off snapshot.

Community views on Agilysys are split, with one side seeing meaningful upside and the other arguing the stock already bakes in a lot of optimism.

Bull case: 11% undervalued

"Agilysys' deep investment in product modernization has resulted in a highly integrated hospitality technology ecosystem, enabling cross-selling of multiple products per customer and underpinning higher average revenue per user (ARPU) and customer retention..."

Read the full Bull Case to see why Agilysys could be undervalued

Bear case: 13% overvalued

"Growing competition from larger SaaS providers and new entrants with more scalable or AI-driven hospitality solutions will likely force Agilysys to lower prices or accept higher customer churn, creating headwinds for future net revenue and compressing gross margins over time..."

Read the full Bear Case to see why Agilysys could be overvalued

Do you think there's more to the story for Agilysys? Head over to our Community to see what others are saying!

The Bottom Line

For Agilysys, the Discounted Cash Flow (DCF) estimate flags intrinsic value that sits comfortably above the current share price, while earnings based multiples point to an overvalued stock relative to peers. That split, together with a low overall value score, suggests the cash flow case is not yet fully backed up by broader valuation checks. The key question from here is whether Agilysys can convert its growth profile into durable, high quality free cash flow that justifies both the intrinsic value upside and the rich P/E that the market is currently paying.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com