Guidance upgrade and credit facility draw investor focus

Palomar Holdings (PLMR) recently raised its 2026 adjusted net income guidance after a robust first quarter, while also securing a new US$450,000,000 unsecured credit facility that increases its financial flexibility.

This combination of a higher earnings target, disciplined underwriting, broad-based premium growth, and added borrowing capacity has drawn fresh attention to how the stock’s recent move may reflect the company’s longer term ambitions.

See our latest analysis for Palomar Holdings.

Against this backdrop, Palomar Holdings’ recent guidance upgrade and new credit facility arrived alongside a 33.9% 1 month share price return and a 10.22% year to date share price return. Its 3 year total shareholder return of 158.16% highlights how longer term holders have already seen significant gains, suggesting recent momentum may be shifting expectations around both growth potential and risk.

If this kind of move has you thinking about what else is setting up for the next leg, it may be worth scanning for other ideas through the 19 top founder-led companies

For Palomar Holdings, the recent surge could be investors re-rating a stronger specialty insurer, or it could be sentiment running ahead of fundamentals. How does the current valuation stack up against the upgraded earnings outlook?

Most Popular Narrative: 6% Undervalued

At a last close of $145.29 versus a narrative fair value of $154.17, Palomar Holdings is framed as modestly undervalued, with analysts centering that view on its reinsurance program and earnings power.

Improved reinsurance terms, proactive risk management, and capital strength (including a $150M buyback program) enable Palomar to maintain conservative retentions while locking in favorable reinsurance economics through 2026, underpinning future earnings stability and supporting continued growth in book value and return on equity.

Want to see what is baked into that fair value? The narrative leans heavily on premium growth, margin durability, and a richer earnings multiple than the sector. The full breakdown shows how those pieces fit together.

Result: Fair Value of $154.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Palomar Holdings' heavy exposure to catastrophe linked lines and reliance on reinsurance terms means that severe events or tighter cover could quickly challenge this undervalued narrative.

Find out about the key risks to this Palomar Holdings narrative.

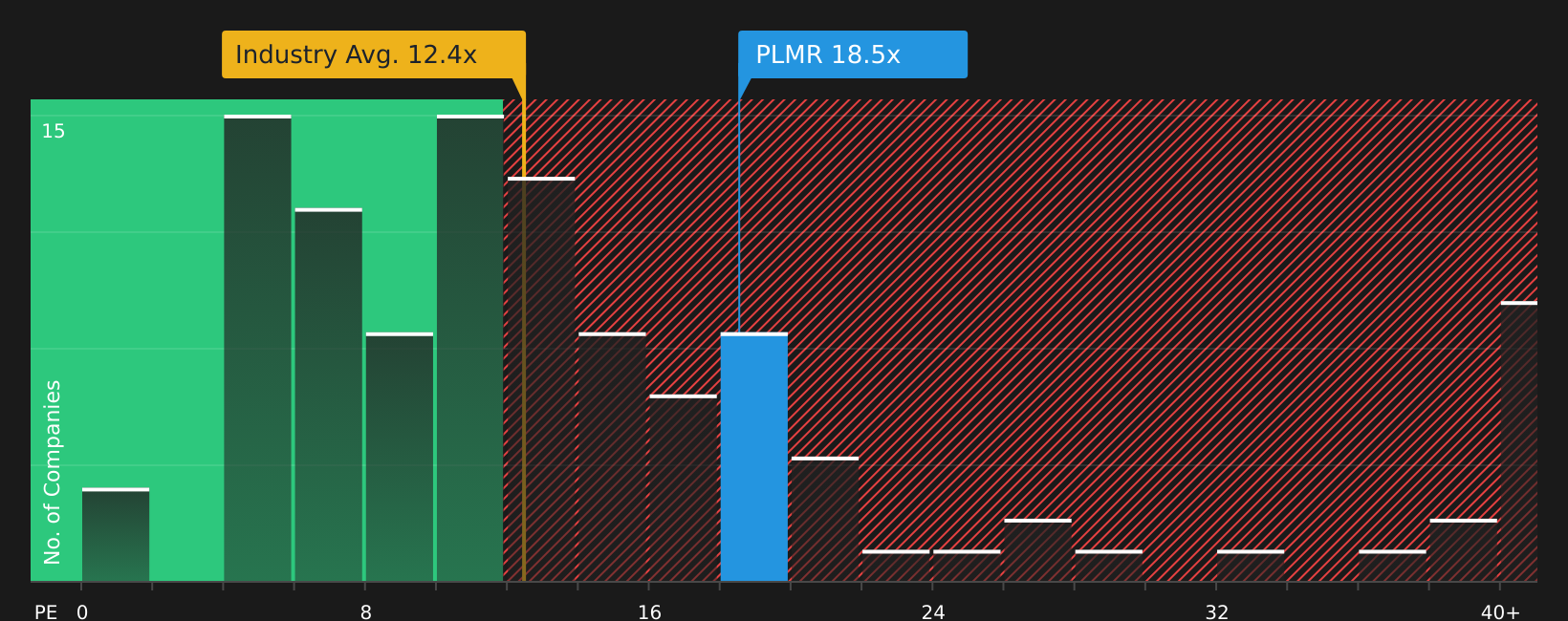

Another View: Palomar Holdings Through A P/E Lens

While the narrative fair value suggests Palomar Holdings is 6% undervalued at $145.29 versus $154.17, the P/E picture tells a different story. The stock trades on 19.5x earnings, compared with 12.2x for the US Insurance industry and 8.2x for peers, and a fair ratio of 14.8x.

That gap points to investors already paying a premium multiple, which can limit upside if expectations around growth or underwriting quality soften. The key question is whether Palomar’s execution justifies that richer P/E or if the market could drift closer to the fair ratio over time.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages in the Palomar Holdings story so far? If the balance of risks and rewards feels finely poised, it may be worth reviewing the data for yourself. You can start with the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Palomar Holdings?

If Palomar Holdings has sharpened your focus on quality, do not stop here. Broader, well researched stock ideas can round out your watchlist and sharpen your next move.

- Spot potential turnarounds early and size them appropriately by scanning 20 elite penny stocks with strong financials before the crowd focuses on them.

- Stack the odds in your favor by filtering for quality companies that look attractively priced using the 45 high quality undervalued stocks.

- Build a steadier income stream by zeroing in on companies highlighted in the 9 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com