Paychex (PAYX) stock is in focus after the company was removed from several Russell growth indices. This shift can prompt trading by index funds and raise questions about how investors assess its fundamentals.

See our latest analysis for Paychex.

After the index removals, Paychex is trading at $106.58, with the 30-day share price return of 7.74% and 90-day share price return of 21.31% contrasting with a 1-year total shareholder return that is down 23.97%. This suggests that short term momentum has strengthened even as longer term returns remain weak.

If this shift in sentiment has you reassessing your watchlist, it could be a good moment to broaden your search and check out 19 top founder-led companies

Paychex has just been dropped from several Russell growth indices, yet the stock has climbed in recent months, leaving you weighing fresh momentum against past underperformance. Do the current fundamentals and price still tilt the risk reward toward buyers?

Most Popular Narrative: 1% Overvalued

The most followed narrative pegs Paychex fair value at $105.43, just below the last close at $106.58, framing the stock as slightly above that estimate.

The analysts have a consensus price target of $105.43 for Paychex based on their expectations of its future earnings growth, profit margins and other risk factors.

Curious what has to happen in Paychex earnings, revenue mix, and margins to support that fair value and future P/E multiple? The full narrative unpacks the growth runway, dividend support, and acquisition assumptions that underpin this tight gap between price and fair value.

Result: Fair Value of $105.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Paychex still faces two key pressures that could challenge this fair value story: integration risk around the Paycor deal and margin strain from higher employee costs.

Find out about the key risks to this Paychex narrative.

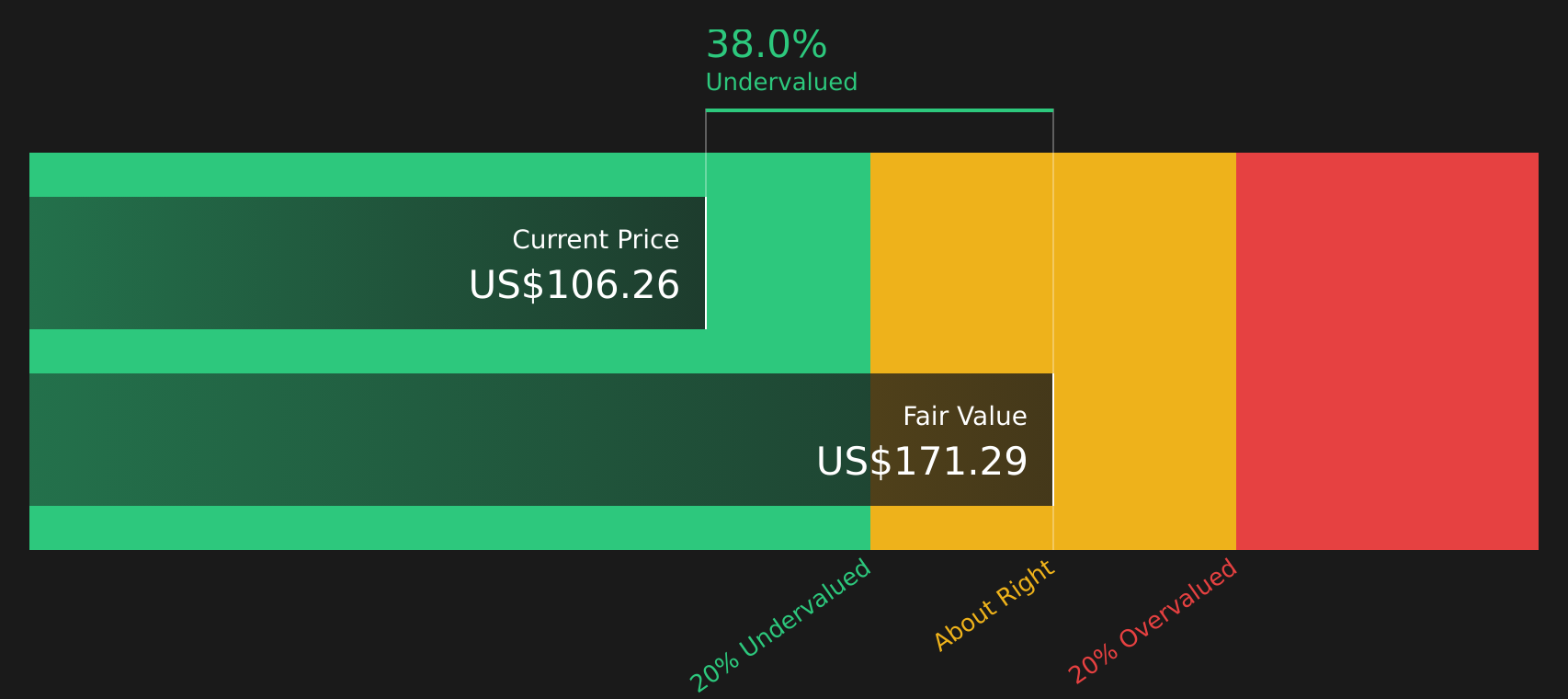

Another View: SWS DCF Puts Paychex in a Different Light

While analyst targets suggest Paychex is roughly fairly priced, the Simply Wall St DCF model points to a very different message, with fair value estimated at $170.98 versus the current $106.58, implying the stock is trading well below that long term cash flow view. Which lens do you trust more for a business this mature?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Paychex for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern around Paychex leaves you undecided, review the underlying data now and shape your own view with 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Paychex?

If Paychex has sharpened your focus on quality and price, do not stop here. Use the Simply Wall St screener to surface more targeted opportunities now.

- Target resilient income by reviewing companies in the 9 dividend fortresses that may appeal if you want yields with a focus on stability.

- Hunt for quality at a possible discount by scanning the 44 high quality undervalued stocks that filters for strong fundamentals and potentially mispriced stocks.

- Prioritize capital preservation by checking the 72 resilient stocks with low risk scores which highlights businesses with lower risk profiles that can help balance a concentrated portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com