- Wall Street analysts previously projected that FB Financial would report quarterly earnings of US$1.14 per share, implying a 29.6% year-over-year increase, while also forecasting improvements in its Core Efficiency Ratio and Net Interest Margin compared with the prior year.

- However, consensus earnings estimates have edged down by 1.7% over the past month, highlighting some caution even as analysts still expect stronger profitability metrics.

- With analysts now balancing higher expected earnings per share against recent estimate cuts, we’ll assess how this shapes FB Financial’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

FB Financial Investment Narrative Recap

To own FB Financial, you need to believe in its ability to translate balance sheet strength and loan growth into sustainably improving profitability. The latest earnings estimate trim looks modest and does not appear to materially alter the near term catalyst around better efficiency and net interest margin, though it does underline the risk that higher funding costs or credit issues could temper that progress in the short run.

Among recent announcements, the Q1 2026 results stand out in this context, with EPS of US$1.10 and net interest income of US$145.97 million providing a recent snapshot of profitability ahead of the upcoming report. As investors weigh those results against expectations for improved Core Efficiency and Net Interest Margin, the trajectory of credit quality, including net charge offs that have ticked higher from recent quarters, remains an important backdrop for any near term earnings surprise.

But while earnings expectations are high, investors should be aware of the integration risk around the Southern States Bank combination and...

Read the full narrative on FB Financial (it's free!)

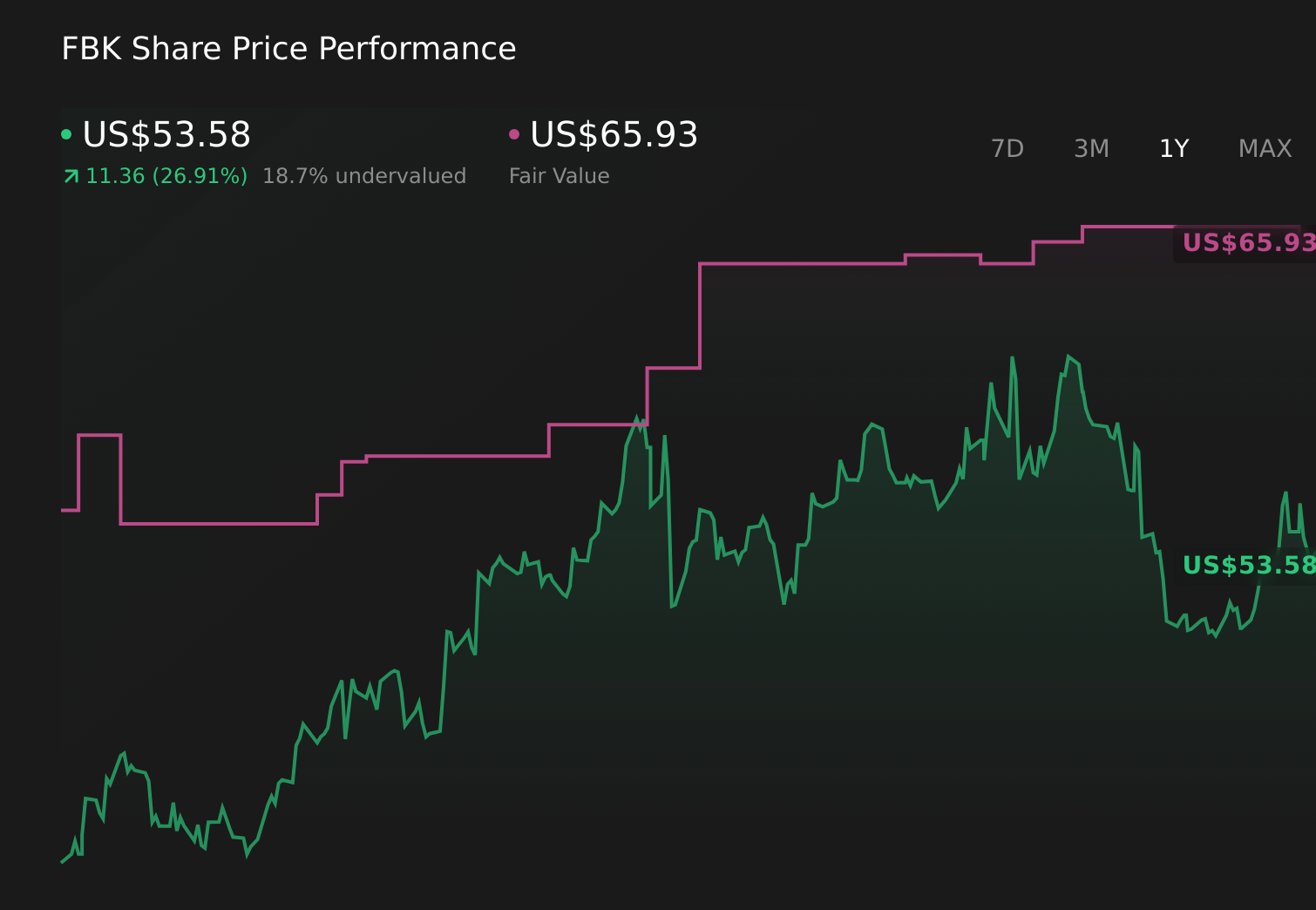

FB Financial's narrative projects $1.0 billion revenue and $415.1 million earnings by 2029.

Uncover how FB Financial's forecasts yield a $64.43 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Two members of the Simply Wall St Community currently value FB Financial between US$64.43 and US$101.14 per share, underscoring how far opinions can differ. Against those views, the focus on improving efficiency and net interest margin after the recent earnings estimate revision may have meaningful implications for how you think about the bank’s earnings power over time.

Explore 2 other fair value estimates on FB Financial - why the stock might be worth as much as 81% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FB Financial research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free FB Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FB Financial's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com