- US Foods Holding Corp. (NYSE: USFD) was recently added to the Russell 1000 Value-Defensive Index and the Russell 1000 Defensive Index, increasing its presence in defensive, value-oriented equity benchmarks.

- This dual index inclusion highlights how US Foods is increasingly viewed as a resilient, value-tilted business within the broader U.S. equity landscape.

- We’ll now examine how US Foods’ addition to key Russell 1000 defensive indices could influence its investment narrative and investor base.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

US Foods Holding Investment Narrative Recap

To own US Foods, you need to believe it can keep converting modest revenue growth into better profitability through efficiency, private label mix, and disciplined capital allocation, despite industry softness. The Russell 1000 Value Defensive index additions may broaden its shareholder base, but they do not materially change the near term catalyst around margin execution or the key risk that food away from home demand could stay weaker for longer.

The recent launch of US Foods SIGNATURE for hospitality customers is especially relevant here, because it ties together several catalysts behind the defensive label: digital tools like Menu IQ, sustainability focused assortments, and labor saving products that can support customer retention and margin resilience, even if case volume growth remains under pressure.

Yet beneath the new defensive label, investors should still be watching the risk that prolonged industry softness and rising costs could...

Read the full narrative on US Foods Holding (it's free!)

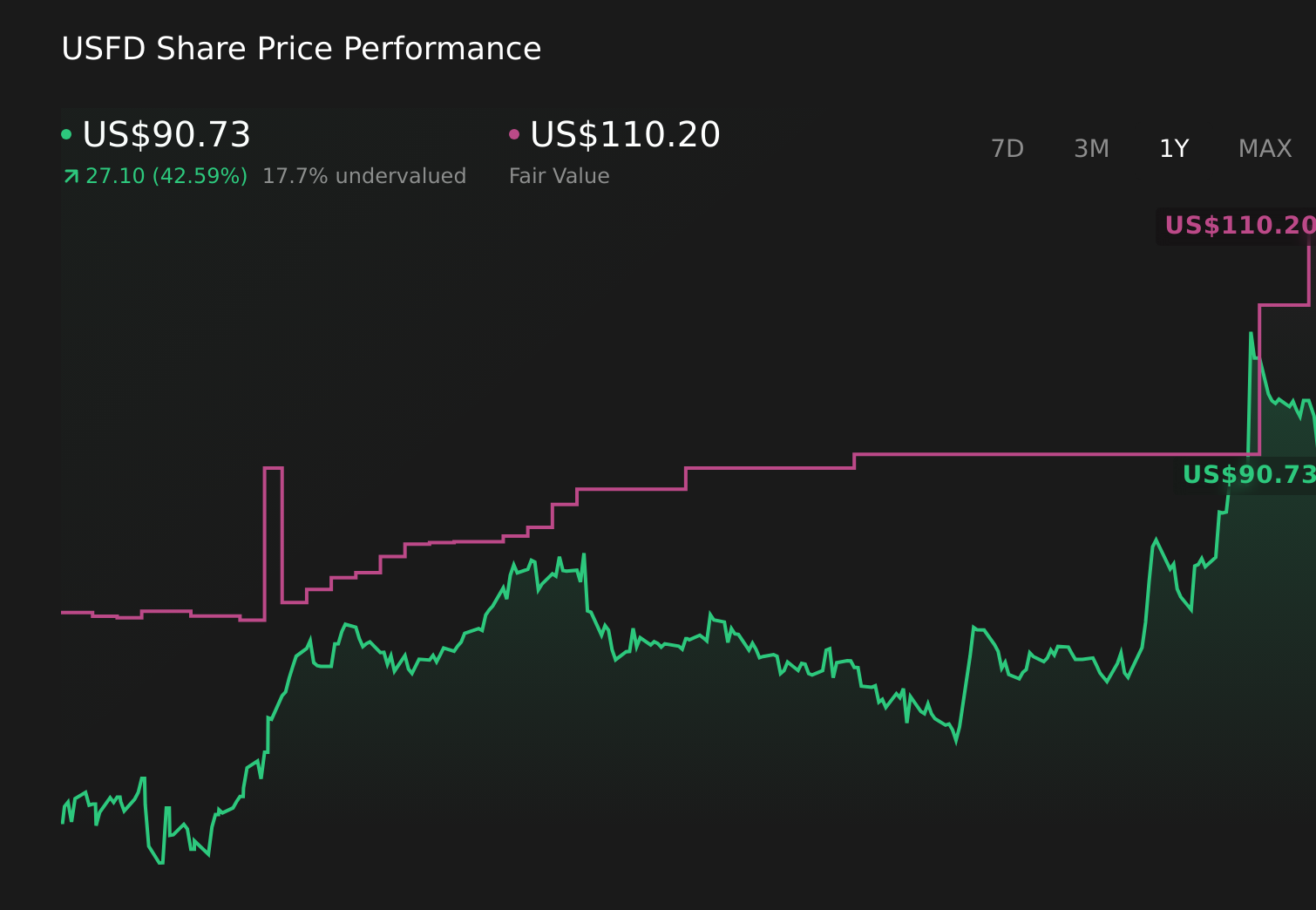

US Foods Holding's narrative projects $45.7 billion revenue and $1.2 billion earnings by 2029. This requires 4.9% yearly revenue growth and about a $523 million earnings increase from $677.0 million today.

Uncover how US Foods Holding's forecasts yield a $104.50 fair value, a 5% upside to its current price.

Exploring Other Perspectives

While index inclusion may hint at resilience, the most pessimistic analysts still see slower revenue growth near 4 percent and only US$1.1 billion of earnings by 2029, so it is worth comparing that cautious view with your own expectations and exploring how this new defensive status could shift the risk and reward balance.

Explore 2 other fair value estimates on US Foods Holding - why the stock might be worth as much as $104.50!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your US Foods Holding research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free US Foods Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate US Foods Holding's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com