With global growth expectations steady but risks from geopolitics, energy and interest rates still in focus, many investors are looking for clearer value in individual stocks rather than broad market bets. Strong cash generation can help companies handle mixed inflation trends, tighter policy and softer consumer data. The Undervalued Stocks Based On Cash Flows screener highlights businesses where SWS DCF valuation suggests the share price sits below estimated fair value, offering a starting point for value-oriented ideas. This article reveals three stocks from that screener, explaining why their cash flow profiles may appeal today.

Eurocell (LSE:ECEL)

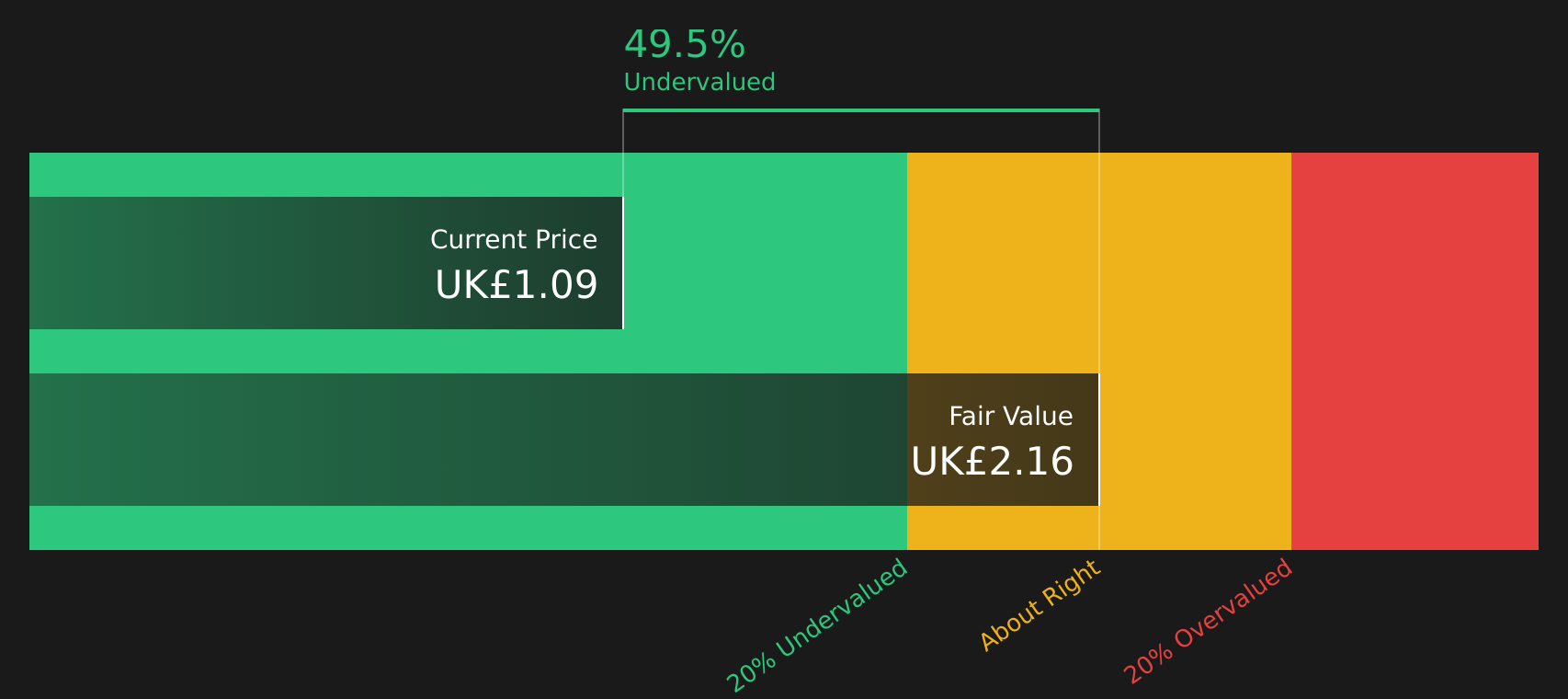

Overview: Eurocell is a UK based manufacturer, distributor, and recycler of PVC and related building products, supplying items such as windows, doors, roofline components, cladding, decking, and roofing solutions to trade and retail customers across the United Kingdom and Republic of Ireland.

Operations: Eurocell generates most of its revenue from Building Plastics at £210.5m and Profiles at £208.2m, with Alunet contributing £46.7m and inter segment revenue of £61.9m, largely concentrated in the United Kingdom at £401.3m and £2.2m from the Republic of Ireland.

Market Cap: £107.1m

Eurocell catches the eye because its cash flow based valuation suggests the stock trades well below estimated fair value while analysts still see earnings growing faster than the wider UK market. The acquisition of Alunet expands its aluminium offering and, together with an enlarged branch network and ERP upgrade, is aimed at sharpening operations and supporting higher quality earnings. At the same time, investors need to weigh cost inflation, thinner current margins around 2.4%, an unstable dividend record, and recent earnings pressure. Governance questions around pay rising as profits fell and reliance on external funding add to the risk checklist, but they also make Eurocell a richer story for investors willing to dig deeper into the numbers and the roadmap.

Eurocell’s cash flow gap to estimated fair value and the Alunet expansion hint at a story the market may be underpricing, but the real twist sits in the 3 key rewards and 1 important warning sign

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity, venture capital and listed funds, giving institutional and retail investors access to renewable energy projects, social and digital infrastructure, and smaller growth companies across the UK, Europe and Australia.

Operations: Foresight Group Holdings generates around £114.8m of revenue from Real Assets and £50.1m from Private Equity, with most income tied to infrastructure and related investment management activities.

Market Cap: £506.4m

Foresight Group Holdings stands out because it combines strong fundamentals with clear growth levers, as assets under management expand in areas like renewable energy and private credit while the business earns a high 27.7% net margin and 47.8% ROE. Revenue and earnings growth have recently been solid, and ongoing share buybacks reduce the free float, which can amplify the impact of any future profit gains. On the flip side, investors need to keep an eye on rising administrative costs, reliance on external funding and the heavy exposure to UK and European regulation around infrastructure and green assets. The more detailed story about how cash flows, growth expectations and risks fit together is where the real interest begins.

Foresight Group Holdings’ high 27.7% net margin and 47.8% ROE suggest a stronger engine than many investors realise, but the full picture of its growth drivers sits in the analyst forecasts for Foresight Group Holdings

BAE Systems (LSE:BA.)

Overview: BAE Systems is a UK based defence, aerospace, and security company that designs and builds combat aircraft, submarines, ships, armoured vehicles, munitions, advanced electronics, and cyber solutions for governments and defence customers around the world.

Operations: BAE Systems generates most of its revenue from Electronic Systems at £7.5b, Air at £7.4b, Maritime at £6.6b, and Platforms & Services at £5.0b, with smaller contributions from Cyber & Intelligence at £2.4b and Head Quarter activities at £52m, partly offset by £592m of intra group revenue.

Market Cap: £52.2b

BAE Systems attracts attention because it combines a £75b order backlog and exposure to higher value areas like electronic warfare, missiles, and satellites with forecasts for earnings and revenue to grow faster than the wider UK market, yet the stock still trades below estimated fair value with a P/E below the sector average. At the same time, the business leans heavily on long running contracts with a small group of governments, faces capacity and supply chain strains, and operates under ESG scrutiny. Any of these factors could affect how quickly that backlog turns into cash. For investors who want to understand whether that mix of visibility, growth and risk justifies the current valuation, the deeper analysis of BAE Systems is where the story gets interesting.

BAE Systems’ £75b backlog and below sector average P/E suggest the market may not fully appreciate its earnings potential, and the real puzzle sits inside the analysis report for BAE Systems

The three stocks highlighted here are just a sample of what this idea uncovers, with the full Undervalued Stocks Based On Cash Flows list surfacing 36 more companies where discounted cash flow suggests equally compelling stories through the Undervalued Stocks Based On Cash Flows screener. Use Simply Wall St to identify and analyze the specific cash flow trends, re rating catalysts and risk factors that matter to you so you can focus on the highest conviction opportunities from that group.

Take Control of Your Investment Journey

If BAE Systems or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

New ideas can start breaking out quietly while attention stays elsewhere, and once momentum builds, ideal entry points can be gone. Scan these fresh candidates under the radar for now and consider them carefully.

- Target sturdier income streams by reviewing a curated set of high yield companies in the 2 dividend fortresses before payout momentum gets fully priced in.

- Spot potential structural winners early by checking a hand picked 34 power grid technology and infrastructure stocks as grids modernize and capital flows toward upgraded energy systems.

- Track where real cash generation meets balance sheet strength with a focused list of solid balance sheet and fundamentals (19 results) before the crowd catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com