Etsy (ETSY) shares are back in focus after the company reported its first sequential increase in active buyers in two years, along with higher spending per buyer and strong growth in app-based sales.

See our latest analysis for Etsy.

The recent buyer metrics appear to have shifted sentiment around Etsy. The 30 day share price return of 13.03% and 90 day share price return of 47.50% have contributed to a year to date share price return of 35.68%. This indicates strong recent momentum compared with a weaker long term picture, as the 5 year total shareholder return is down 57.37%.

If this recovery story has you thinking more broadly about where growth could show up next, it may be worth checking out 18 top founder-led companies

Etsy now looks more like a business finding its footing again, yet the share price has already moved a long way in a short period. Is the stock still offering value at today’s levels, or mainly pricing in the good news?

Most Popular Narrative: 7.3% Overvalued

The current Etsy share price of $77.72 sits above the most widely followed fair value estimate of $72.40, which is built using a 9.97% discount rate and detailed cash flow assumptions.

The analysts have a consensus price target of $72.4 for Etsy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $85.0, and the most bearish reporting a price target of just $58.0.

Curious what powers that $72.40 fair value for Etsy? The narrative focuses on expectations for future earnings, potential margin uplift, and a re rated profit multiple. Want the full blueprint behind those assumptions?

Result: Fair Value of $72.40 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Etsy still faces pressure from declining gross merchandise sales and softer buyer engagement, which could challenge the earnings and margin assumptions behind that $72.40 fair value.

Find out about the key risks to this Etsy narrative.

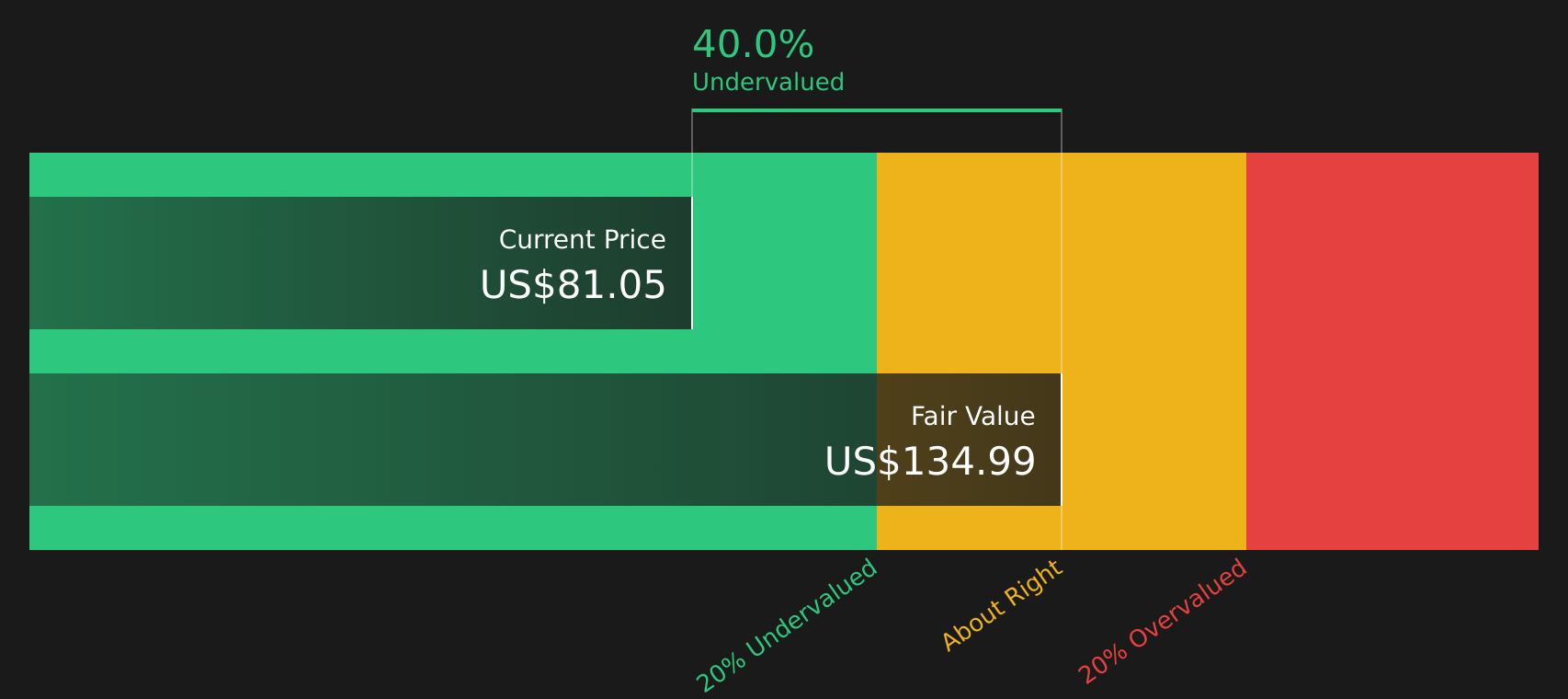

Another View: Etsy Through a Cash Flow Lens

While the analyst narrative suggests Etsy is around 7.3% overvalued at $77.72 versus a fair value of $72.40, the Simply Wall St DCF model points in the opposite direction. On that framework, Etsy is trading at a 42.4% discount to an estimated future cash flow value of $134.93, implying the market is putting a much lower price on those projected cash flows.

When one approach flags modest overvaluation and another suggests a wide discount, it puts the spotlight on your own assumptions around growth durability, margins, and risk. Consider which set of expectations lines up more closely with how you see Etsy's business developing, and how that perspective might influence your next move.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Etsy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Etsy clearly mixed, this is a moment to move quickly, review the full picture, and weigh both sides for yourself using 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Etsy?

If you are reassessing Etsy, it can be useful to line it up against other opportunities so you are not relying on a single story for your portfolio.

Use the Simply Wall St Screener to spot fresh setups, compare quality, and pressure test your thesis before prices move without you.

- Target potential mispricings by scanning 44 high quality undervalued stocks that combine solid fundamentals with attractive valuations.

- Build a sturdier core in your portfolio by reviewing companies in the solid balance sheet and fundamentals stocks screener (47 results) that may better handle tougher conditions.

- Hunt for off the radar potential by browsing the screener containing 19 high quality undiscovered gems before they land on everyone else's watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com