- In late June 2026, Westlake Corporation (NYSE: WLK) was removed from the Russell 1000 Defensive Index and the Russell 1000 Value-Defensive Index, marking its exit from two widely followed benchmarks. This change may alter how quantitatively driven and index-linked investors view the stock’s role in diversified, lower-volatility portfolios.

- We’ll now examine how Westlake’s removal from these Russell 1000 defensive indices could influence its investment narrative and perceived risk profile.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Westlake Investment Narrative Recap

To own Westlake today, you need to believe the company can work through industry overcapacity, cost inflation and recent losses to restore sustainable profitability. The key near term catalyst is execution on cost control and asset optimization, while the biggest risk remains prolonged weak pricing and demand across core chemical chains. Westlake’s removal from the Russell 1000 defensive indices does not meaningfully change these business fundamentals, though it may influence how some investors classify the stock’s risk.

In that context, the recent move to secure a new unsecured revolving credit facility of up to US$1,500,000,000, maturing in 2031, looks particularly relevant. It reinforces Westlake’s liquidity and financial flexibility at a time when earnings are under pressure and the company is exiting defensive indices, potentially helping it fund ongoing restructuring and cost reduction efforts that underpin its main catalysts for improvement.

Yet, while index changes may feel cosmetic, investors should be aware of how they interact with sustained losses and pressure on...

Read the full narrative on Westlake (it's free!)

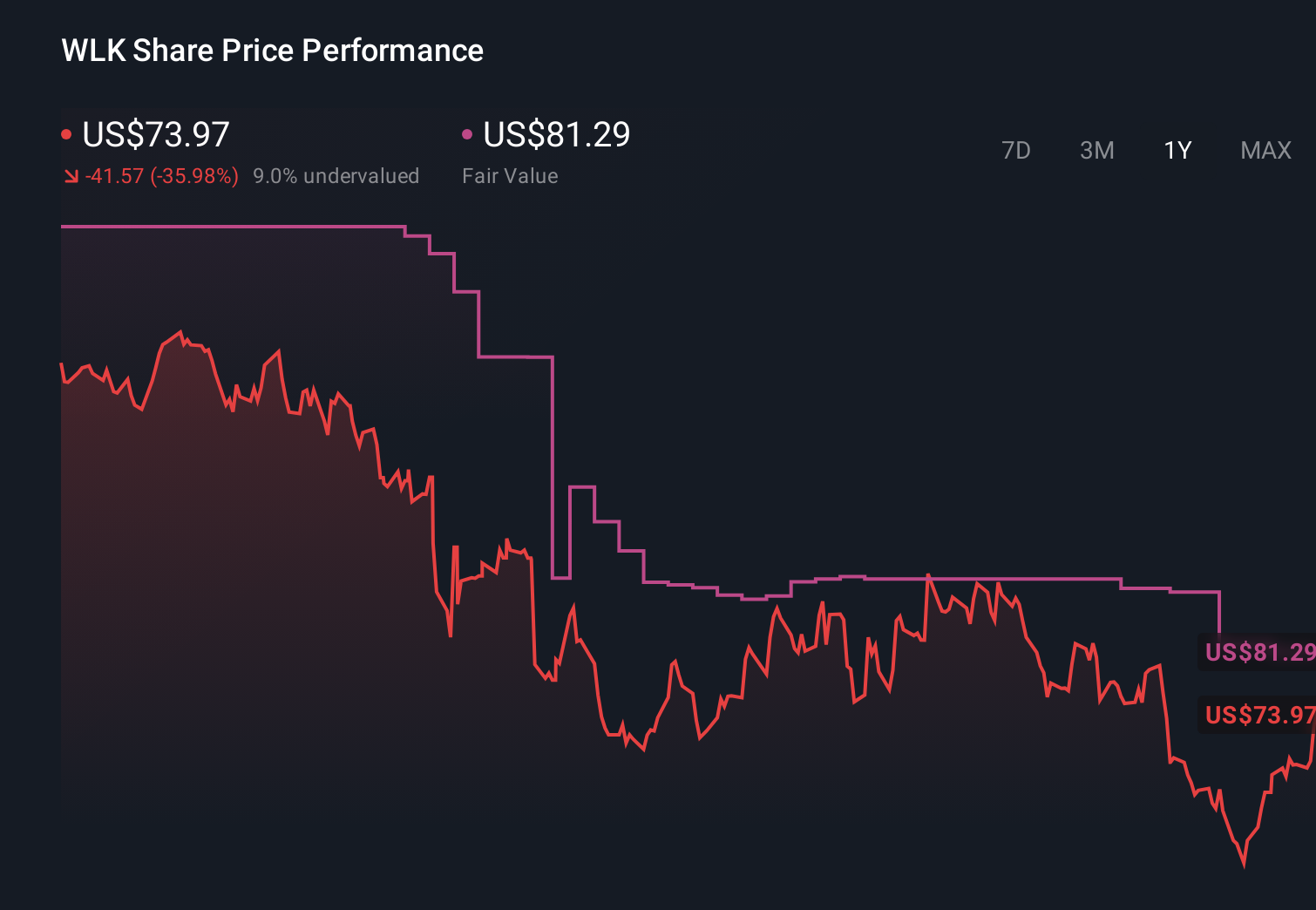

Westlake’s narrative projects $13.0 billion revenue and $605.7 million earnings by 2029.

Uncover how Westlake's forecasts yield a $105.40 fair value, a 42% upside to its current price.

Exploring Other Perspectives

While consensus focuses on near term losses and index removal, the most optimistic analysts were once penciling in about US$13.3 billion of revenue and US$546.5 million of earnings, so you can see how opinions diverge and why it is worth exploring several possible paths from here.

Explore 3 other fair value estimates on Westlake - why the stock might be worth 6% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

No Opportunity In Westlake?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com