- In recent weeks, lululemon athletica inc. filed a US$728.53 million shelf registration for 6,300,000 common shares tied to an ESOP offering, faced a new consumer-protection lawsuit over tariff-related price increases, was removed from several Russell growth and defensive indices, and confirmed plans to enter India by end-2026 via Tata CLiQ.

- Together, these developments highlight a company balancing capital-raising flexibility, legal and index-related headwinds, and expansion into a large new market that could reshape its international mix.

- Next, we’ll examine how the India entry via Tata CLiQ fits with Lululemon’s reset narrative and evolving growth-risk tradeoff.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

lululemon athletica Investment Narrative Recap

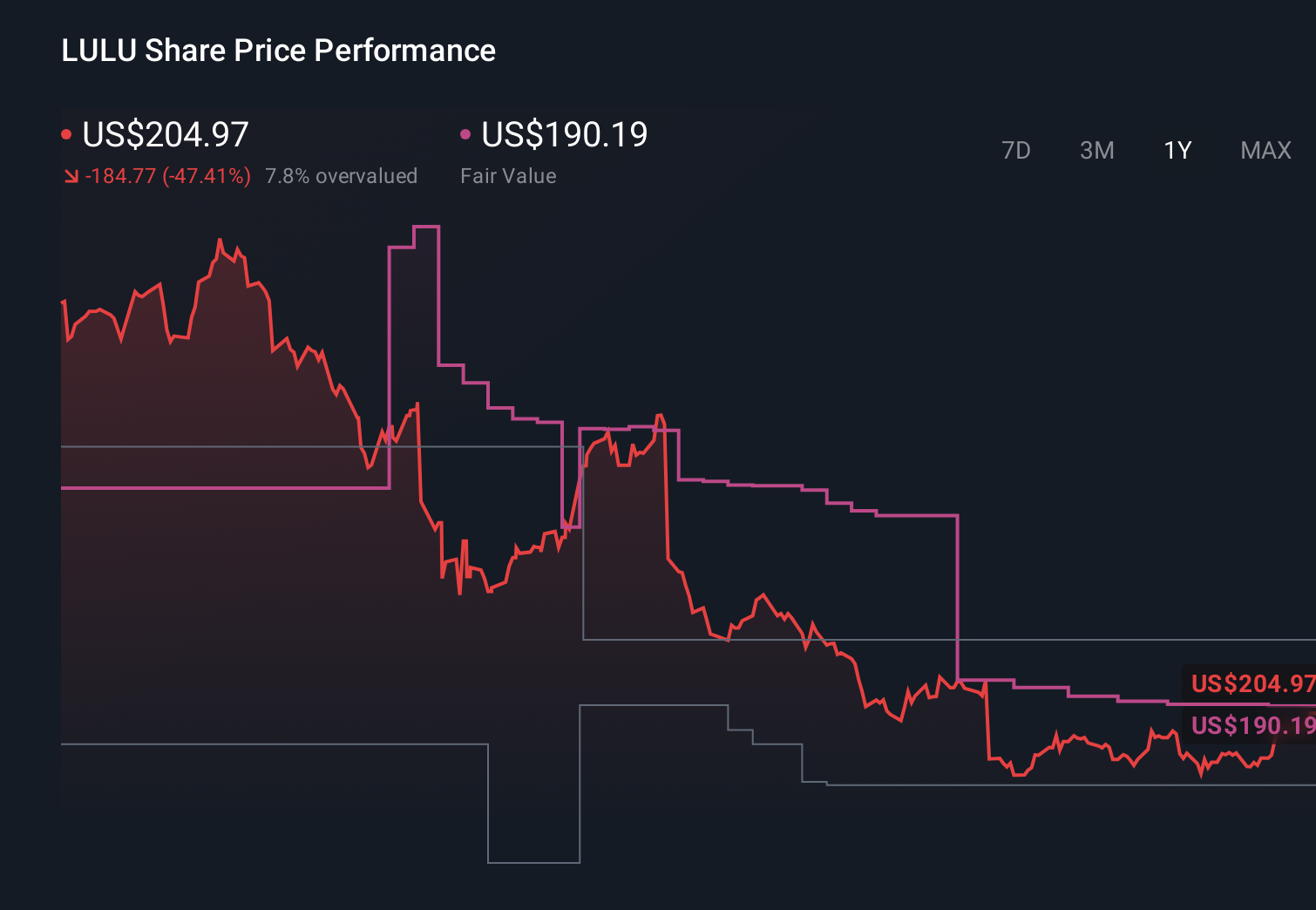

To own lululemon today, you need to believe the brand can reinvigorate product demand, defend margins under tariff pressure, and extend its reach outside a softening U.S. market. The new tariff-related lawsuit and Russell index removals add legal and technical overhangs, but do not fundamentally alter the near term focus on product reset and U.S. traffic. The biggest incremental risk now is whether tariff-related legal and regulatory issues expand in scope or financial impact.

Among recent developments, the consumer-protection lawsuit over tariff-linked price increases is most relevant, because it directly intersects with the core margin risk already flagged around higher import costs. Any settlement costs, refunds, or required pricing changes could compound the existing tariff and de minimis headwinds that analysts expect to weigh on gross and operating margins, and may influence how investors think about the payoff from lululemon’s product refresh and international expansion plans.

But against that, investors should be aware that the new tariff lawsuit could further pressure margins and brand trust if...

Read the full narrative on lululemon athletica (it's free!)

lululemon athletica's narrative projects $12.3 billion revenue and $1.6 billion earnings by 2029. This requires 3.2% yearly revenue growth and about a $0.1 billion earnings increase from $1.5 billion today.

Uncover how lululemon athletica's forecasts yield a $132.16 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting about US$13.8 billion of revenue and US$2.2 billion of earnings by 2028, yet the latest tariff lawsuit and international expansion risks show how far those views can sit from current uncertainties, so it is worth considering how your own expectations compare before you decide what story you believe.

Explore 40 other fair value estimates on lululemon athletica - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your lululemon athletica research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com