Intuitive Machines (LUNR) is back in focus after securing a firm fixed price NASA contract worth up to US$148.3 million to deliver a production line qualified Nova C lunar lander by 2028.

See our latest analysis for Intuitive Machines.

Even with the new NASA award, Intuitive Machines shares have been under pressure recently, with the stock down 38.48% on a 30 day share price return and softer 90 day performance. However, the 1 year total shareholder return of 51.16% still points to strong longer term gains as investors weigh contract wins against index removals and insider selling.

If this kind of contract driven story has your attention, it could be a good moment to scan other space and robotics plays using the 30 robotics and automation stocks

Intuitive Machines now sits between two stories: a fresh NASA contract and a share price that has fallen sharply in recent weeks. Are you looking at a weaker business, or just sentiment resetting the valuation?

Most Popular Narrative: 26.5% Undervalued

Against the last close of $16.90, the most followed narrative on Intuitive Machines argues for a higher fair value, anchored in a shift toward higher margin space infrastructure and data services.

Balancing High-Growth Potential with Capital Dilution Intuitive Machines (LUNR) has successfully shifted from a high-risk startup to a Lunar Infrastructure Prime, backed by a $943M backlog and a strategic pivot toward high-margin data services via the Lanteris acquisition. While the trajectory toward positive Adjusted EBITDA in 2026 is clear, the current stock price reflects a "perfection premium" that overlooks recent share dilution.

The narrative hangs on a sharp ramp up in revenue, a turn in profitability, and a specific fair value per share that relies on these projections lining up. Want to see exactly how those moving parts are stitched together, and which assumptions matter most for Intuitive Machines.

Result: Fair Value of $23 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Intuitive Machines still faces clear risks, including any slip in the projected revenue ramp or execution issues that challenge the assumed shift toward higher margin services.

Find out about the key risks to this Intuitive Machines narrative.

Another View: Intuitive Machines Through The Fair Ratio Lens

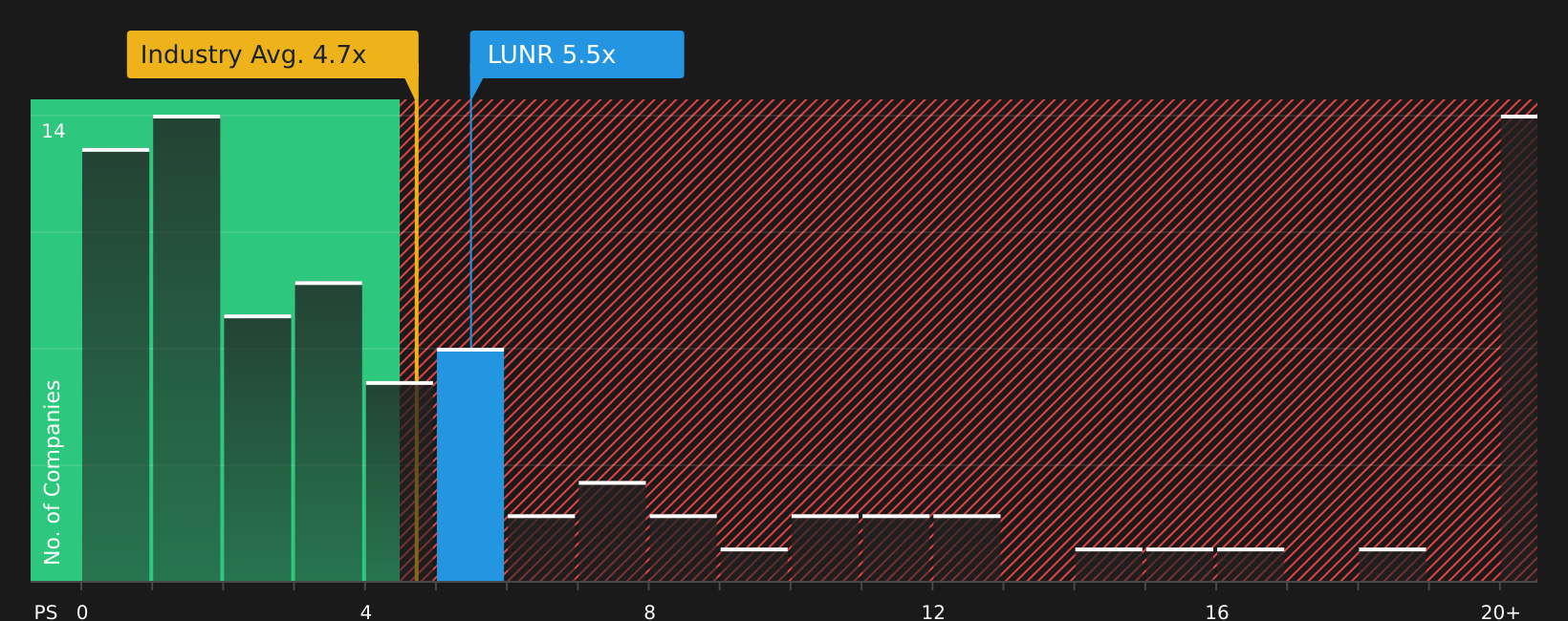

The first narrative leans on future revenue and a target P/S multiple for Intuitive Machines, but the fair ratio view paints a tougher picture. LUNR trades on a P/S of 8.1x, compared with a fair ratio of 4.2x, the US Aerospace & Defense average of 5.3x, and a 3.5x peer average.

That gap suggests the stock carries valuation risk if expectations cool or peers re rate closer to their own fair ratio. How comfortable are you paying a premium while the business is still loss making?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment split between opportunity and caution, it helps to move fast and review the underlying data yourself so you are not relying solely on headlines. To weigh up the mix of concerns and bright spots around Intuitive Machines, start by reviewing the 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Intuitive Machines?

Do not stop with Intuitive Machines. Widen your watchlist now so you are not looking back later wishing you had sized up more opportunities earlier.

- Spot potential bargains early by scanning screener containing 19 high quality undiscovered gems that combine solid fundamentals with the chance to be noticed by the market later.

- Strengthen your core holdings by focusing on companies in the solid balance sheet and fundamentals stocks screener (47 results) that can better handle tougher conditions.

- Reduce portfolio stress by checking stocks in the 73 resilient stocks with low risk scores that score well on resilience and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com