As the Canadian market navigates a landscape marked by cooling energy prices and a steadying labor market, the Bank of Canada's decision to hold interest rates offers a stable backdrop for investors. In this environment, identifying stocks with strong fundamentals and growth potential becomes crucial, especially when exploring Canada's lesser-known opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| China Gold International Resources | 22.48% | -1.05% | 7.48% | ★★★★★★ |

| Alvopetro Energy | 19.58% | 10.05% | 8.67% | ★★★★★★ |

| Total Energy Services | 7.22% | 19.55% | 43.43% | ★★★★★★ |

| Fortuna Mining | 7.42% | 12.80% | 34.67% | ★★★★★★ |

| Thor Explorations | NA | 41.85% | 64.80% | ★★★★★★ |

| Calfrac Well Services | 22.77% | 11.78% | 32.39% | ★★★★★★ |

| Santacruz Silver Mining | 23.34% | 26.91% | 51.48% | ★★★★★★ |

| Parex Resources | 9.06% | 2.33% | -12.59% | ★★★★★☆ |

| Logan Energy | 20.64% | 29.77% | 62.16% | ★★★☆☆☆ |

| Journey Energy | 14.72% | 8.95% | -32.77% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

China Gold International Resources (TSX:CGG)

Simply Wall St Value Rating: ★★★★★★

Overview: China Gold International Resources Corp. Ltd. is a mining company involved in the acquisition, exploration, development, and mining of mineral resources in China and Canada, with a market cap of CA$9.78 billion.

Operations: The company's revenue is primarily derived from its mine-produced copper concentrate and gold, with copper concentrate generating $1.10 billion and gold contributing $386.08 million.

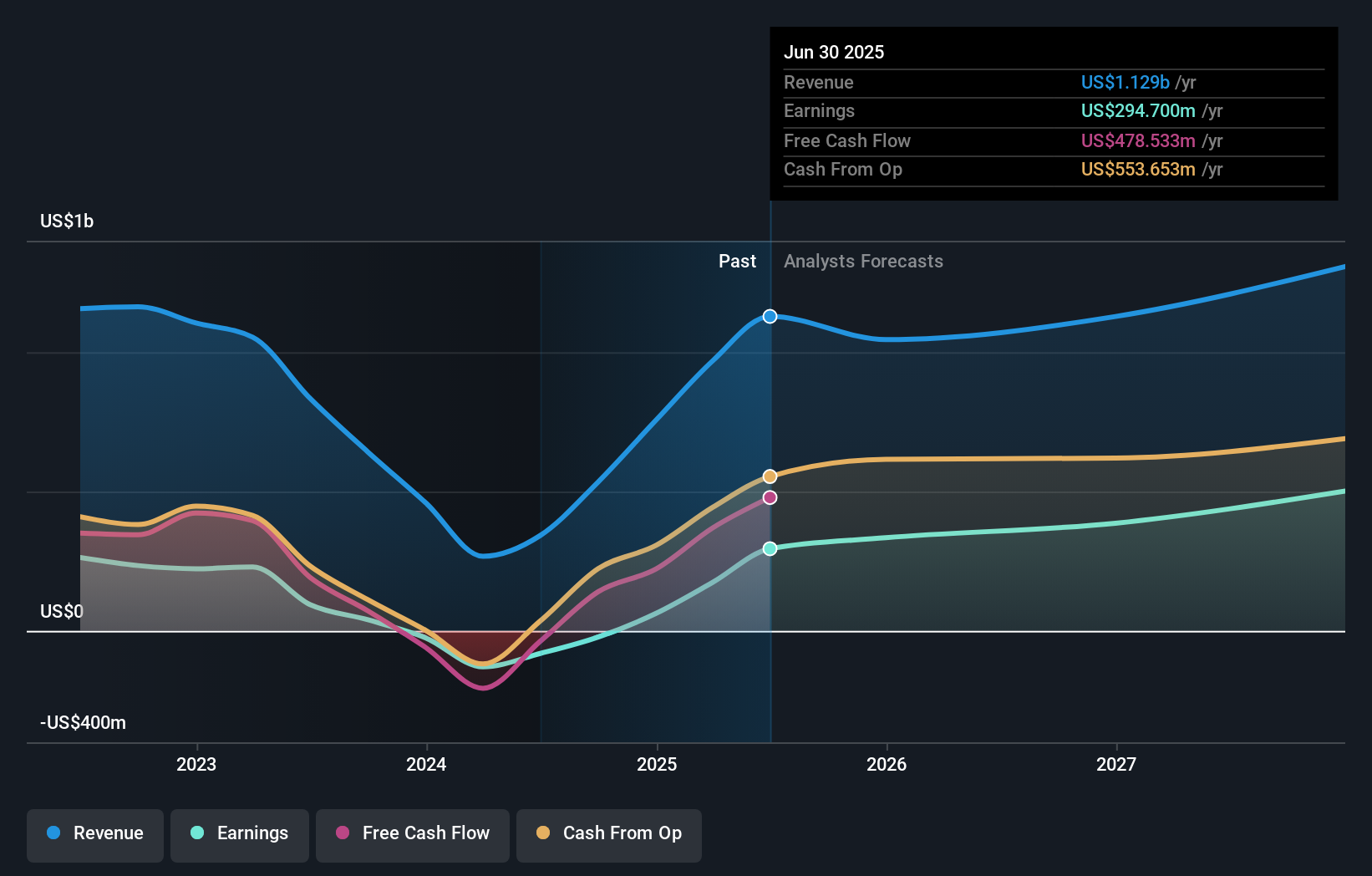

China Gold International Resources, a smaller player in the mining sector, has recently showcased significant financial and operational strides. Over the past five years, its debt-to-equity ratio improved from 73.9% to 22.5%, indicating stronger financial health. The company's earnings surged by 253.9% last year, outpacing the broader Metals and Mining industry growth of 129.4%. Additionally, a recent update to their Jiama Copper Polymetallic Project revealed a substantial increase in mineral resources and reserves—measured resources skyrocketed by over fivefold to 623 million tonnes—highlighting its potential for long-term production expansion and value creation.

- Delve into the full analysis health report here for a deeper understanding of China Gold International Resources.

Understand China Gold International Resources' track record by examining our Past report.

Fortuna Mining (TSX:FVI)

Simply Wall St Value Rating: ★★★★★★

Overview: Fortuna Mining Corp. is involved in precious and base metal mining operations across Argentina, Côte d'Ivoire, Mexico, Peru, and Senegal with a market capitalization of approximately CA$3.49 billion.

Operations: Fortuna Mining's revenue is primarily derived from its Sango, Bateas, and Mansfield segments, with Sango contributing $621.10 million and Mansfield $342.55 million.

Fortuna Mining, a nimble player in the mining sector, is making waves with its strategic projects and robust financial health. The company recently reported a significant earnings growth of 250% over the past year, outperforming the industry average of 136.8%. Its debt-to-equity ratio has impressively dropped from 21.2% to 7.4% over five years, showcasing prudent financial management. Fortuna's ambitious Diamba Sud Gold Project in Senegal promises strong returns with an after-tax NPV of US$1 billion at US$3,500/oz gold price and an IRR of 60%. Additionally, their share buyback program saw repurchases amounting to CA$112 million this year alone.

Parex Resources (TSX:PXT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Parex Resources Inc. is involved in the exploration, development, production, and marketing of oil and natural gas primarily in Colombia, with a market capitalization of CA$2.12 billion.

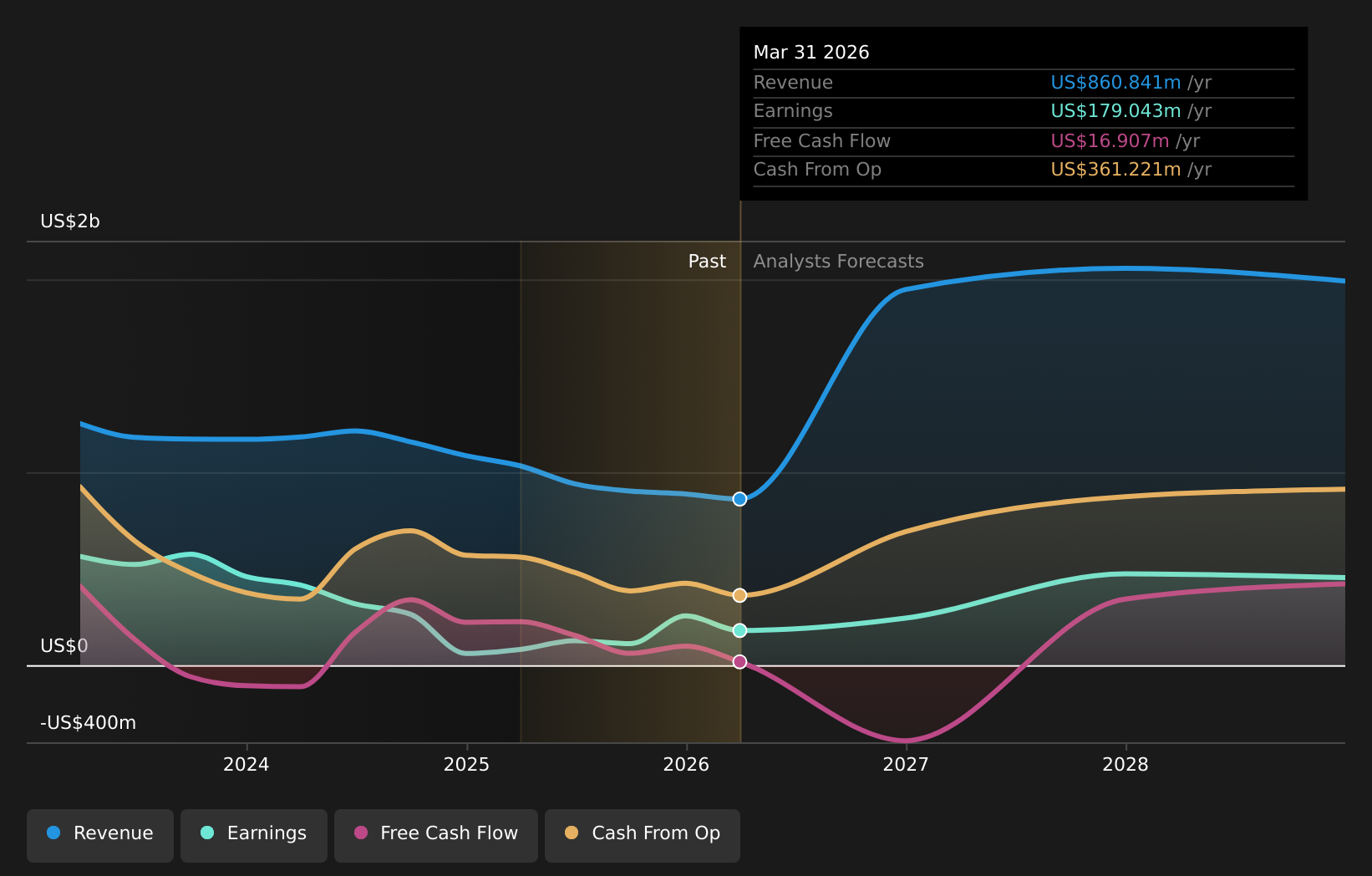

Operations: Parex Resources generates revenue primarily from its oil and gas exploration and production segment, amounting to $860.84 million.

Parex Resources, a nimble player in Canada's energy sector, is making waves with its robust earnings growth of 120.5% over the past year, outpacing the industry average. Trading at 90.7% below its estimated fair value, Parex offers attractive investment potential despite having increased its debt to equity ratio from 0% to 9.1% over five years. Recent production results highlight an average of 54,090 boe/d for Q2 and successful acquisitions like Frontera E&P bolster future prospects. However, reliance on Colombian assets poses regulatory risks that could affect long-term stability amidst evolving market conditions and geographic concentration challenges.

Seize The Opportunity

- Navigate through the entire inventory of 11 TSX Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com