Delta Air Lines stock has returned 123.0% over the past five years, and at around US$89 per share the key question now is how that run lines up with what the valuation work is saying, especially as both the Discounted Cash Flow (DCF) intrinsic value estimate and earnings multiples currently point to the shares screening as undervalued.

- A 123.0% five year return suggests investors who held Delta Air Lines through recent cycles have already seen substantial gains, so any perceived discount today matters for fresh capital.

- Expectations for solid cash generation from premium travel, loyalty revenue and maintenance services can support the valuation case. At the same time, exposure to volatile fuel costs and airline sector sentiment may cap how much investors are willing to pay for that cash flow.

- With the company scoring 4 out of 6 on our value checks, the broader picture is a mixed one rather than a slam dunk bargain, even though both the intrinsic value work and market multiples tilt cheap.

The issue now is whether Delta Air Lines’ recent share price strength has already captured that apparent discount, or if there is still a clear margin between today’s price and the intrinsic value implied by the DCF and multiples.

Is Delta Air Lines Still Cheap on Cash Flow?

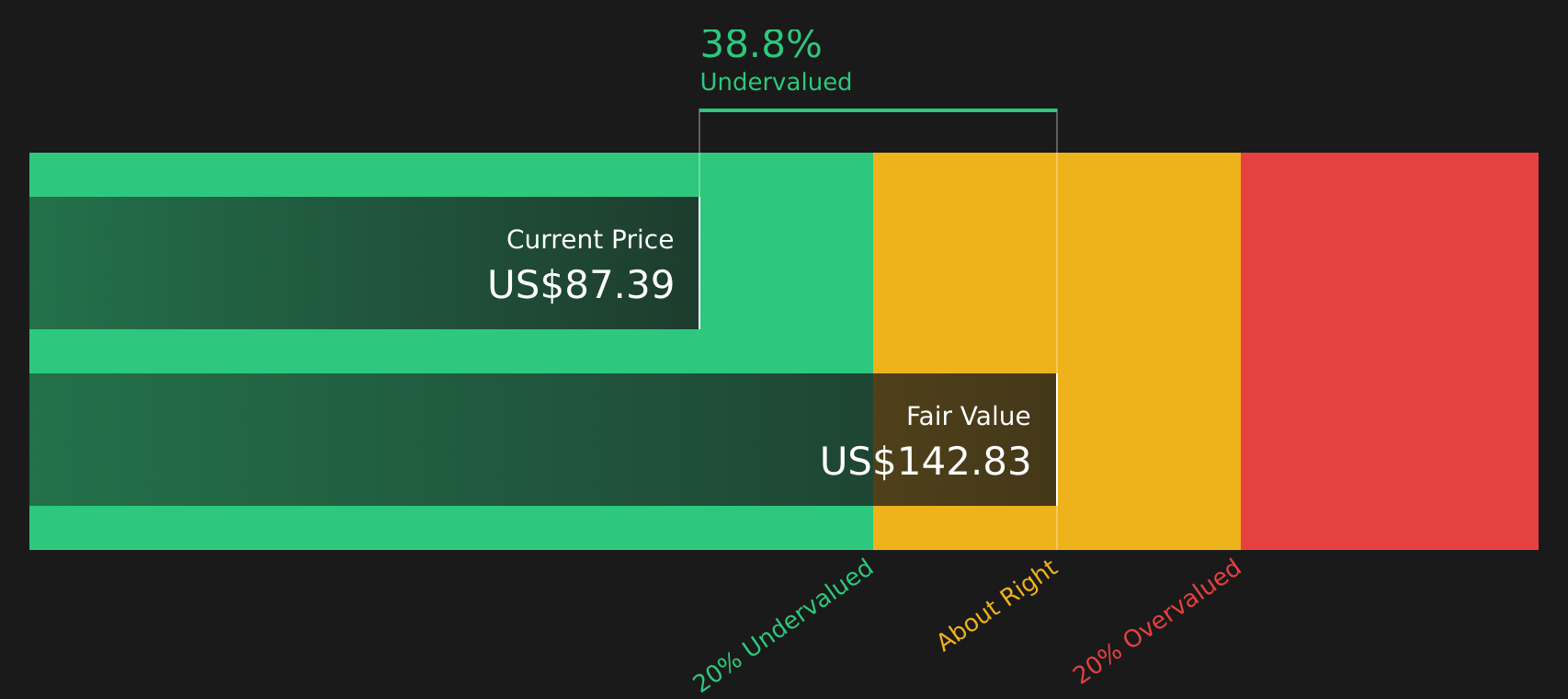

The Discounted Cash Flow (DCF) model here is built on cash flow projections rather than earnings or dividends. For Delta Air Lines, the latest twelve month free cash flow sits at about $3.1b, and the model assumes that cash generation continues to grow from this base over time rather than resetting lower.

On those assumptions, the DCF points to an estimated intrinsic value of about $113 per share, compared with a current share price around $89, implying the stock screens roughly 21.3% undervalued. Recent analyst reports highlighting higher fuel costs and short term earnings pressure are provided as a potential explanation for why the market is still pricing Delta Air Lines below what its cash flows support.

Overall, the DCF work suggests Delta Air Lines stock currently appears undervalued versus its implied intrinsic value under these assumptions.

Our Discounted Cash Flow (DCF) analysis suggests Delta Air Lines is undervalued by 21.3%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Delta Air Lines Still Cheap on Earnings?

P/E is a useful lens for Delta Air Lines because earnings are a core focus for how the market values established airlines. Delta currently trades on a P/E of about 13.0x, compared with an industry average near 9.7x and a broader peer average around 26.4x. So the stock carries a premium to the typical airline, but still sits below many larger peers in the wider group.

The model based fair P/E ratio for Delta is 27.4x, which reflects what investors might pay given its business mix, profitability profile and risk. Set against the current 13.0x, that is a wide gap and points to the shares screening as undervalued on this metric, even after the recent share price moves and analyst sentiment.

On the P/E multiple alone, Delta Air Lines stock appears undervalued relative to what the model suggests investors might typically pay for its earnings profile.

See what the numbers say about this price — find out in our valuation breakdown.

The Delta Air Lines Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Delta Air Lines pick up where the valuation work leaves off by explaining which paths for Delta Air Lines' revenue, margins and earnings would need to occur for the stock to be worth materially more or less than it is today, and what would have to change to shift that view. Rather than focusing on a single multiple or model output, each narrative sets out the assumptions behind its fair value so you can compare them with Delta Air Lines' results as they are reported over time on the Community page.

Community views on Delta Air Lines sit on a wide spectrum, with one camp seeing meaningful upside and the other arguing the stock already reflects its strengths.

Bull case: 17% undervalued

"Delta Air Lines' focus on premium and international markets is expected to drive resilience in revenue, particularly with increases in premium and loyalty revenue, and strong Transatlantic and Pacific growth, which should offset domestic softness…"

Read the full Bull Case to see why Delta Air Lines could be undervalued

Bear case: 9% overvalued

"Economic uncertainty and stalled growth, particularly in domestic and main cabin travel, pose risks to Delta's revenue growth and net margins as demand softens…"

Read the full Bear Case to see why Delta Air Lines could be overvalued

Do you think there's more to the story for Delta Air Lines? Head over to our Community to see what others are saying!

The Bottom Line

For Delta Air Lines, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple work point in the same direction, with each suggesting the stock screens as undervalued rather than fully priced. The DCF implies a sizeable discount, while the current P/E still sits below what the model indicates investors might typically pay for this earnings profile.

The key question from here is whether Delta can sustain the cash generation and earnings quality that sit behind those models, in the face of fuel cost swings and shifting travel demand. That tension will help determine whether today’s discount reflects opportunity or a value trap that the market has already judged correctly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com