Credit card stocks and payment networks are sitting at the center of a powerful tension right now, with credit card debt near record levels, average card rates around 22%, inflation at 4.2% and the Federal Reserve weighing another possible hike in 2026. Higher borrowing costs can pressure households, yet payment volumes can still run high as people lean on plastic. This article looks at three US Credit Card Issuers and Payment Networks that appear well positioned, in different ways, for these conditions and explains how the latest macro signals might matter for each stock.

Eagle Bancorp (EGBN)

Overview: Eagle Bancorp operates EagleBank, a Bethesda based regional bank that focuses on relationship lending and deposit services for businesses, investors and consumers across the Washington, D.C. area, offering everything from commercial loans and government contractor financing to personal credit cards, mortgages and digital banking.

Operations: Eagle Bancorp currently generates about US$21.4 million of revenue from its core banking operations in the United States.

Market Cap: US$818.2 million

Investors looking at credit card exposed stocks may find Eagle Bancorp interesting because it sits at the crossroads of higher card rates and recovering loan economics. It is still trading below book value on a P/B of 0.7x. Analysts expect very strong revenue and earnings growth over the next few years, helped by a shift toward commercial and consumer lending, even though the bank is currently loss making with a negative ROE of 10.92%. Recent results show improving net income alongside elevated charge offs. The completion of office credit cleanup, along with a refreshed, largely independent board and a new CEO, is described as setting the stage for a potential earnings reset that is not fully explained here.

Eagle Bancorp’s low 0.7x P/B and expected earnings reset hint that the market may be missing something. Compare that valuation gap with the DCF valuation analysis for Eagle Bancorp and see what the current multiples might be masking.

Northeast Bank (NBN)

Overview: Northeast Bank is a Portland based regional bank that offers a broad mix of traditional deposit accounts, residential and commercial real estate loans, business credit facilities, and consumer lending, supported by digital services such as online, mobile, and telephone banking for customers across Maine and the wider United States.

Operations: Northeast Bank generates about US$230.3 million in revenue from its core banking activities in the United States.

Market Cap: US$1.1b

Northeast Bank stands out in the credit cycle because it combines strong profitability with a niche in purchasing discounted and nonperforming loans, which can be attractive when credit card debt and borrowing costs are elevated. Recent results show healthy net interest income and earnings, and analysts expect solid revenue and earnings growth. The stock trades on a P/E close to the broader US Banks industry, while consensus price targets still sit above the current share price. That potential upside comes with trade offs, including higher expenses from technology investment, competition for purchased loans, and concentration risks in areas such as New York City multifamily. For investors willing to weigh those risks carefully, the full story around Northeast Bank may be more detailed than the headline numbers suggest.

Northeast Bank’s earnings story and discounted loan niche look intriguing, but the real question is how sustainable that edge is as credit conditions evolve. Get the full picture in the analysis report for Northeast Bank

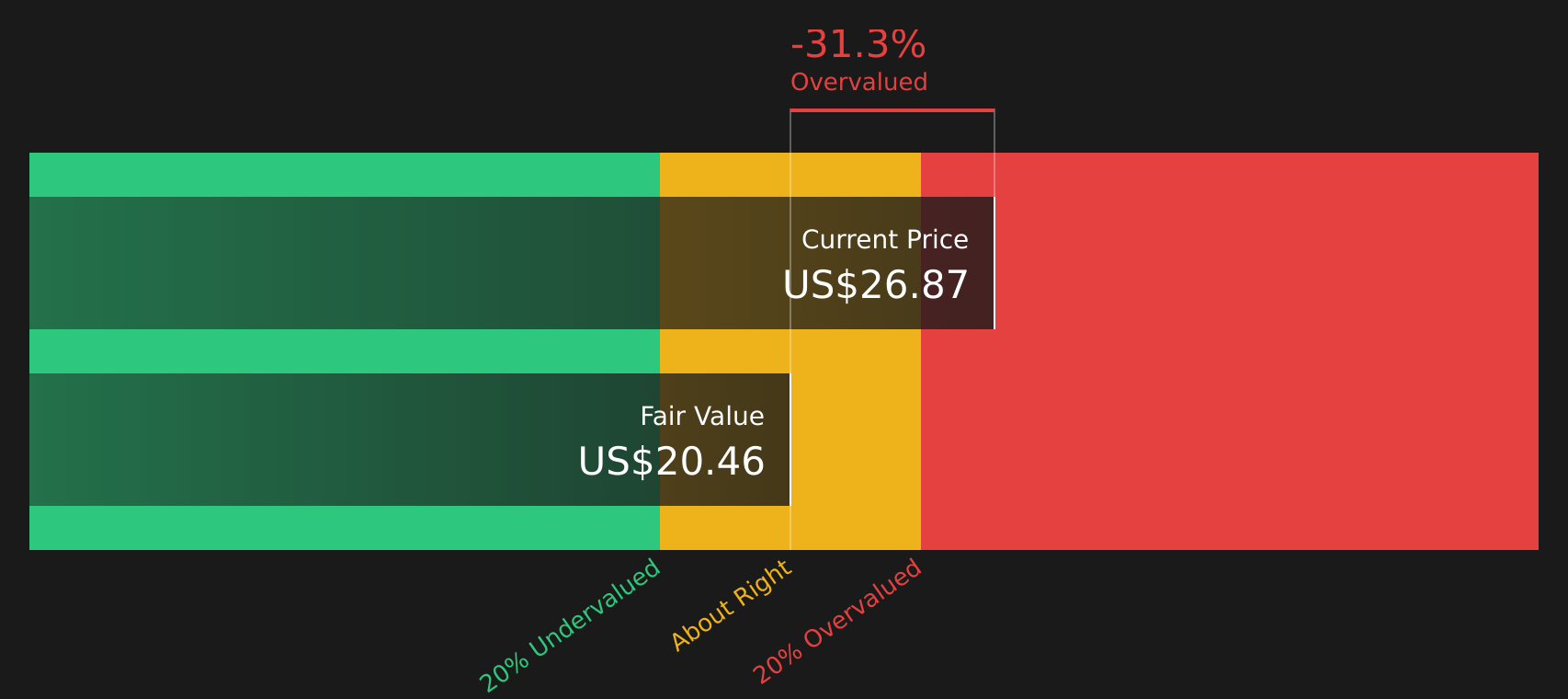

Alerus Financial (ALRS)

Overview: Alerus Financial is a Grand Forks based financial services company that combines a community bank with retirement and benefits administration and wealth management, serving businesses and consumers with deposits, loans, credit cards and a wide range of advisory and trust services.

Operations: Alerus Financial generates about US$143.8 million from Banking including mortgage activities, US$67.2 million from Retirement and Benefit Services, US$28.6 million from Wealth Advisory Services, and a US$3.0 million loss in Corporate Administration, all from the United States.

Market Cap: US$775.7 million

Investors watching credit card exposed banks may find Alerus Financial interesting because it blends traditional lending with fee based retirement and wealth businesses. As a result, it participates in higher card and loan yields while still collecting recurring noninterest revenue. Recent results show earnings growth, a 2.68% dividend and active buybacks, but also rising charge offs and a relatively low allowance for bad loans, which leave less room for error if credit quality weakens. With strong earnings forecasts together with a high P/E and analyst targets clustered close to the current price, the key consideration is whether the mix of technology investment, credit discipline and fee income can justify today’s valuation as rates and consumer stress build.

Alerus Financial’s mix of fee income, a 2.68% dividend, and buybacks could be masking a more complex credit story. Weigh that balance of opportunity and pressure in the 3 key rewards and 1 important warning sign

The stocks covered here are just a starting point, with the full US Credit Card Issuers and Payment Networks screener surfacing 39 more companies that carry equally compelling narratives and different ways to gain exposure to transaction driven revenue, so make sure you check the US Credit Card Issuers and Payment Networks screener. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter most to you, so you can focus on the highest conviction ideas instead of sifting through everything on your own.

Take Control of Your Investment Journey

If Eagle Bancorp or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Picks?

Some of the sharpest breakout stories start quietly, then move fast once momentum hits and the crowd catches on. Scan these fresh ideas while it matters and get in early.

- Spot resilient businesses before sentiment turns by running the 76 resilient stocks with low risk scores and keep your focus on companies built to handle tougher conditions without drama.

- Tap into structural demand for AI infrastructure by reviewing the 52 AI infrastructure stocks and see which enablers could benefit as data centers and workloads keep scaling.

- Ride the potential shift in energy and power policy by checking the curated 89 nuclear energy infrastructure stocks and find companies positioned for long term nuclear projects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com