Geopolitics is back on every investor’s screen, with US Iran tensions, disputed ceasefires, and uncertainty around the Strait of Hormuz all feeding into questions about global infrastructure, energy flows, and major construction projects. Sudden shifts in risk perceptions can change how capital is priced for large engineering and infrastructure groups, whether they are tied to energy routes, rebuilding efforts, or longer term development. This article focuses on three stocks from our Global Infrastructure and Engineering Companies screener that appear positively exposed to the latest news and may help you assess whether they align with your own risk tolerance and portfolio goals.

GenusPlus Group (ASX:GNP)

Overview: GenusPlus Group is an Australian contractor that plans, builds, upgrades, and maintains power and communications infrastructure for electricity utilities, miners, telecom operators, and renewable energy projects across the country.

Operations: GenusPlus Group generates most of its A$953.8m revenue in Australia, primarily from Infrastructure at about A$568.0m, Energy and Engineering at about A$282.1m, and Services at about A$129.3m.

Market Cap: A$1.70b

GenusPlus Group sits at the heart of Australia’s push to modernise and harden its power grid, which is front of mind when geopolitical tensions highlight how critical resilient energy and communications networks are. The company is tightly linked to large renewables and transmission projects and has been growing earnings quickly, supported by a high 25.7% ROE and a healthy pipeline of utility and grid work. At the same time, you need to weigh its relatively high P/E multiple, reliance on external borrowing, and exposure to a handful of big, long term projects and government spending. If you want to understand how these positives and risks could affect long term returns, there is much more beneath the surface of GenusPlus Group’s story.

GenusPlus Group’s fast growing earnings and 25.7% ROE raise big questions about what the market is really pricing in. Check how that story stacks up against the analyst forecasts for GenusPlus Group before one key assumption shifts.

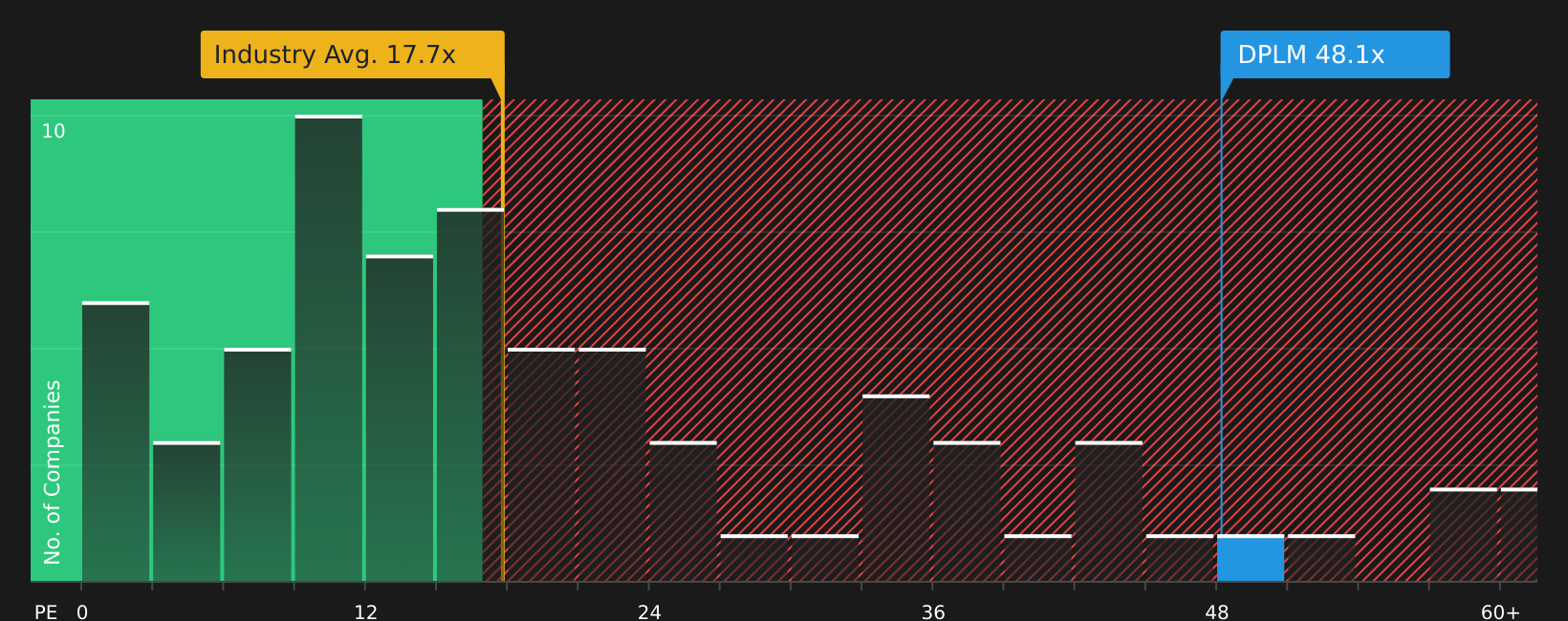

Diploma (LSE:DPLM)

Overview: Diploma is a London based group that supplies specialist controls, seals, and life sciences products and services, from cables, fasteners, and fluid power components to surgical instruments and diagnostic equipment, to industrial customers and healthcare providers around the world.

Operations: Diploma generates most of its £1.65b revenue from Controls at £940.4m, alongside Seals at £454.2m and Life Sciences at £252.5m, with meaningful exposure across the USA, UK, Europe and other international markets.

Market Cap: £9.12b

Diploma stands out in the Global Infrastructure and Engineering Companies screener because it sits at the junction of several critical themes that matter when geopolitical tensions threaten supply chains and energy routes. The company focuses on specialist, often mission critical parts and services, has grown earnings historically, and is targeting further gains through acquisitions and integration in areas like seals and life sciences. At the same time, a high P/E multiple, reliance on external funding, and a relatively new management team raise the bar for execution, especially if acquisition driven growth or key industrial end markets slow. For investors, the key consideration is whether Diploma’s mix of resilient niche products and global reach justifies the premium that the market is currently paying.

Diploma’s premium P/E and global reach suggest investors see more ahead, but the real question is whether earnings quality matches the price. The full analyst forecasts for Diploma could reveal what the headline numbers are not saying yet.

Austal (ASX:ASB)

Overview: Austal is an Australian shipbuilder that designs, constructs, and supports defence and commercial vessels worldwide, supplying naval ships, patrol boats, passenger ferries, offshore service vessels, and advanced control systems to governments and commercial operators.

Operations: Austal generates most of its A$2.11b revenue from USA Shipbuilding at about A$1.25b and USA Support at about A$303.9m, with Australasia Shipbuilding contributing around A$344.3m and Australasia Support about A$210.6m.

Market Cap: A$1.56b

Austal sits at the intersection of rising maritime security concerns and demand for reliable naval infrastructure, which takes on particular significance when tensions flare around vital routes such as the Strait of Hormuz. The company combines a large order book and expanding shipyard capacity with growing higher margin support and sustainment work. This aims to smooth what can be a lumpy, contract driven earnings profile. At the same time, heavy reliance on government defence contracts, high external borrowing, and governance questions around board turnover and executive pay present risk factors to consider. With earnings forecasts, valuation estimates, and recent technology deals in play, the key issue is how much of this mix of opportunity and risk is already reflected in Austal’s share price.

Austal’s expanding defence work and support revenue could be masking a far bigger story about how contracts, balance sheet pressure, and valuation all intersect right now, and the full analysis report for Austal stops just as the crucial risk twist appears

The three stocks here are just the starting point, and the full Global Infrastructure and Engineering Companies screener surfaces 20 more companies with equally compelling infrastructure and engineering narratives that could fit different risk profiles and time horizons. Use Simply Wall St to identify and analyze the exact catalysts, balance sheet traits, and business narratives discussed in this article so you can focus on the ideas that best match your own portfolio strategy.

Take Control of Your Investment Journey

If GenusPlus Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh opportunities do not stay quiet for long, and once momentum builds the best entry points can vanish before the crowd catches on. Scan these ideas now to review them while they are still developing.

- Track income-focused companies in the 6 dividend fortresses to monitor yields and price movements over time.

- Look for resilient compounders using the curated 8 resilient stocks with low risk scores while they remain relatively under the radar.

- Review the hand picked 8 top copper producer stocks to stay informed on materials-focused companies as demand trends evolve.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com