General Motors stock has delivered a 100.7% return over the past three years, yet its valuation signals are split, with a Discounted Cash Flow (DCF) estimate pointing to meaningful upside while traditional market multiples suggest the shares screen as expensive. That tension is sharpened by a low overall value score, leaving investors weighing a strong share price record against mixed valuation checks.

- Over the past three years, General Motors has returned 100.7%, which puts more pressure on today’s valuation to be supported by future cash flows rather than past share gains.

- Efforts to build higher margin revenue streams through areas like Ultium batteries, GM Energy and software subscriptions can support the DCF based intrinsic value, while intense competition in key markets such as China and the capital needs of automation and EV programs may limit how much of that value is realised for shareholders.

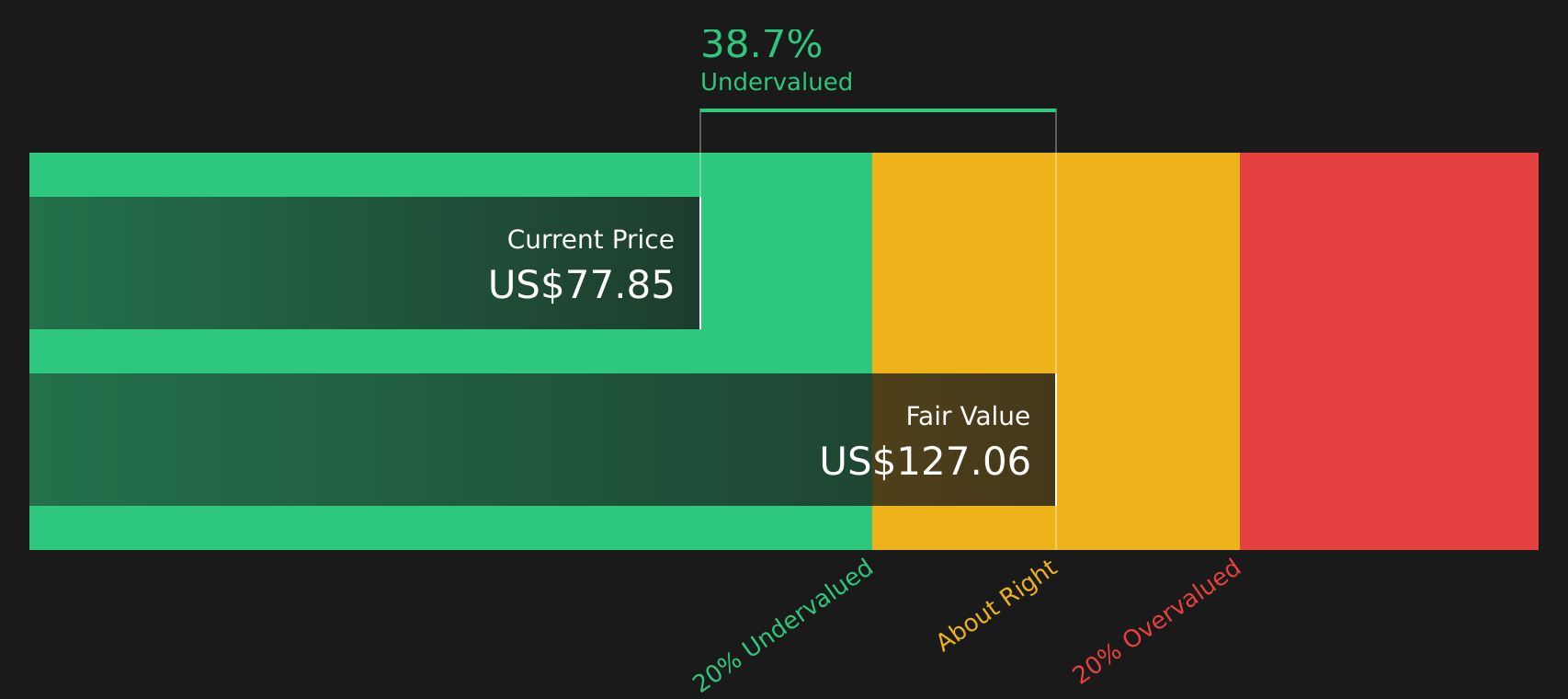

- With a valuation score of 2 out of 6, General Motors does not screen as a clear bargain on the broader checks even though the intrinsic value estimate suggests the stock is undervalued by 38.7%.

The issue now is whether the current US$77.85 share price already reflects the risks around General Motors or whether the Discounted Cash Flow (DCF) implied upside offers a margin of safety.

Is General Motors Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model values General Motors by projecting future free cash flows and discounting them back to today. For General Motors, the latest twelve month free cash flow is about $13.6b, and the model assumes these cash flows continue growing rather than swinging sharply up or down.

On that basis, the DCF model arrives at an estimated intrinsic value of about $127 per share, compared with the current $77.85 share price, implying the stock is 38.7% undervalued in this framework. GM's push into Ultium batteries, GM Energy and software subscriptions is one factor used to frame the cash flow outlook in the model, even as GM faces competitive and capital pressures in areas such as China and automation.

Because the launch of Ultium Cells' LFP battery production broadens GM's energy storage footprint, the current discount suggests the market is still cautious about how much of that opportunity will reliably translate into future cash flows.

Overall, this DCF analysis indicates that, under its assumptions, General Motors stock appears undervalued relative to the cash flows implied in the model.

Our Discounted Cash Flow (DCF) analysis suggests General Motors is undervalued by 38.7%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Has General Motors Run Too Far on Earnings?

The P/E ratio is a useful way to look at General Motors because earnings are still a core anchor for how the stock is priced. At the current share price of US$77.85, General Motors trades on a P/E of about 28.9x, which is well above the auto industry average of 14.4x and also above the peer average of 21.9x.

On the platform’s fair P/E estimate of 24.7x, which blends factors such as the company’s scale, profitability profile and risk, General Motors screens as expensive, with the current multiple sitting a few turns higher. Even allowing for its push into Ultium batteries, GM Energy and software subscriptions, the market is already paying a premium to what this framework suggests as a more balanced earnings multiple.

Taken together, the P/E comparison indicates General Motors stock currently looks overvalued on an earnings basis.

See what the numbers say about this price — find out in our valuation breakdown.

The General Motors Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for General Motors sit between the DCF upside and the richer P/E multiple. They spell out what paths for General Motors' growth, margins and earnings would make the stock worth materially more or less than today’s price, and they sit on Simply Wall St’s Community page. Each narrative links its number to a clear view on where General Motors' growth, profitability and risks could go next, giving you something specific to revisit as new information arrives.

Community views on General Motors are sharply split, with one camp focused on upside from energy storage and software while the other zooms in on the cost and risk of the transition.

Bull case: 18% undervalued

"The growing monetization of software and services such as Super Cruise and OnStar, evidenced by $4 billion in deferred revenue and rapid subscriber growth, creates higher-margin recurring revenue streams…"

Read the full Bull Case to see why General Motors could be undervalued

Bear case: 16% overvalued

"EVs are still margin-dilutive for GM. Battery costs, manufacturing inefficiencies, and supply chain constraints continue to pressure profitability…"

Read the full Bear Case to see why General Motors could be overvalued

Do you think there's more to the story for General Motors? Head over to our Community to see what others are saying!

The Bottom Line

For General Motors, the Discounted Cash Flow (DCF) intrinsic value estimate points to meaningful undervaluation, while the earnings based view flags the stock as overvalued on its current P/E multiple. That split largely comes down to how you weigh future cash flows against today’s expectations for growth and risk. The low overall value score is a reminder that most broad checks are not yet backing the intrinsic value signal. The crux from here is whether General Motors can turn its capital heavy push into batteries, energy and software into durable, high quality cash flows rather than a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com