As geopolitical tensions and energy market volatility continue to influence global markets, Asian equities have shown mixed performance, with technology stocks experiencing notable fluctuations. In this environment, identifying undervalued stocks—those trading below their intrinsic worth—can provide opportunities for investors seeking value in a complex economic landscape.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

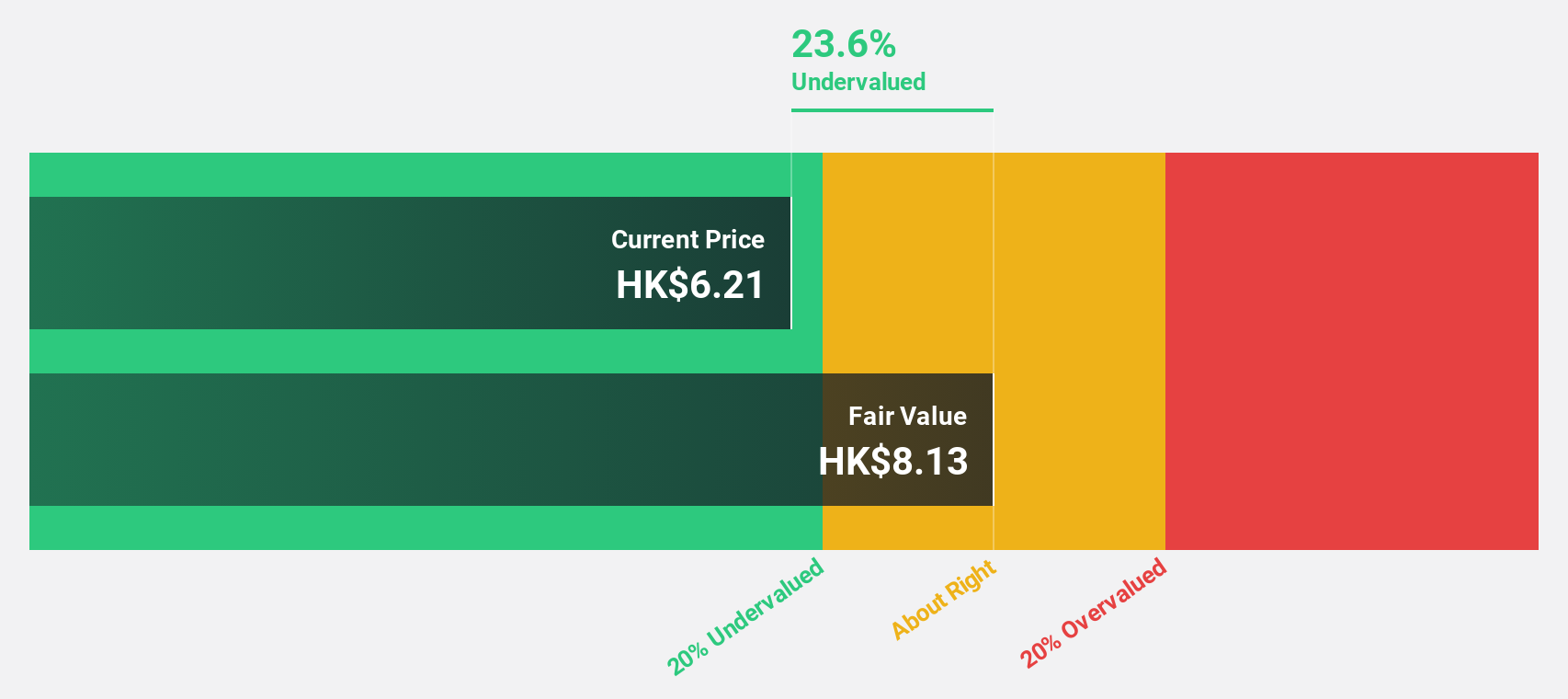

| Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$19.27 | HK$38.14 | 49.5% |

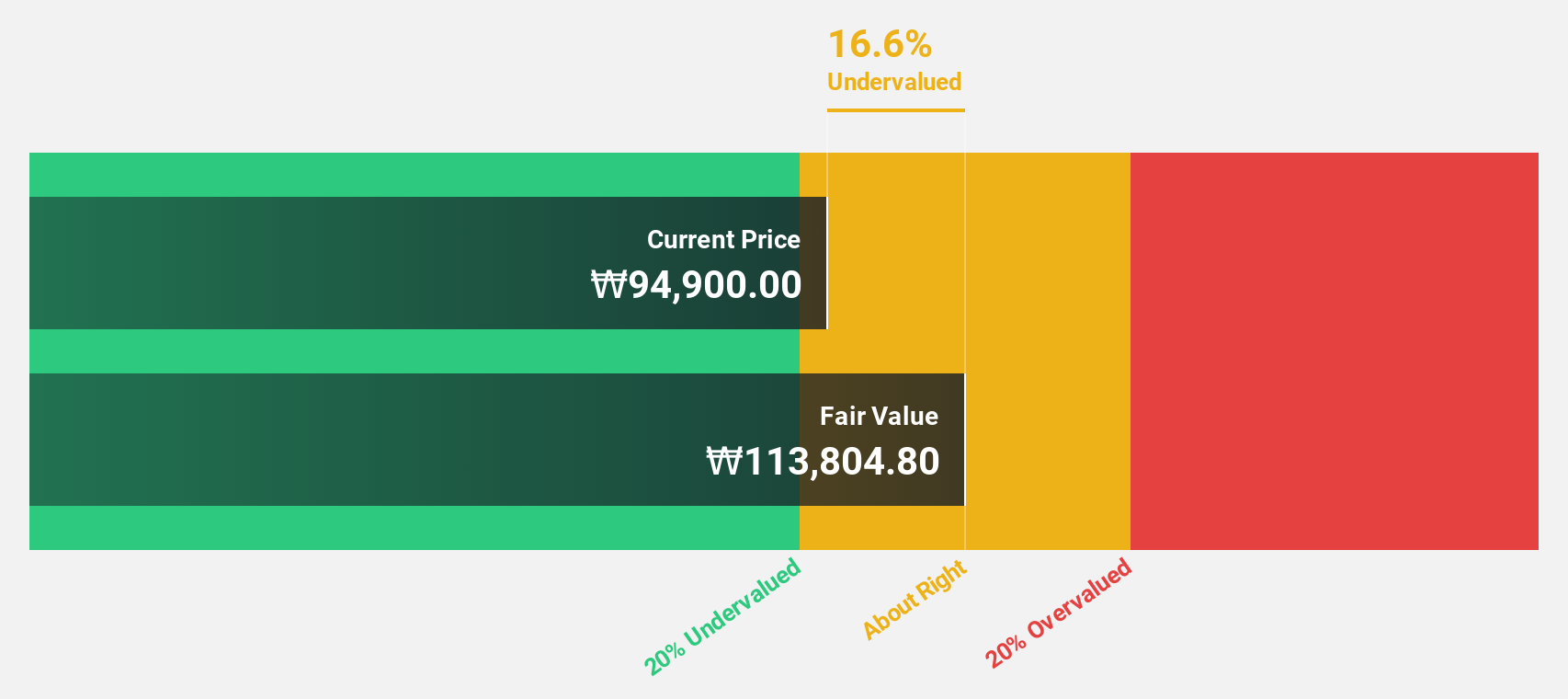

| VINA TECHLtd (KOSDAQ:A126340) | ₩71800.00 | ₩140975.05 | 49.1% |

| Rakus (TSE:3923) | ¥1036.50 | ¥2014.23 | 48.5% |

| Moshi Moshi Retail Corporation (SET:MOSHI) | THB39.00 | THB75.90 | 48.6% |

| Mao Geping Cosmetics (SEHK:1318) | HK$50.65 | HK$100.59 | 49.6% |

| JNTC (KOSDAQ:A204270) | ₩17810.00 | ₩34582.85 | 48.5% |

| DIO (KOSDAQ:A039840) | ₩12830.00 | ₩25566.73 | 49.8% |

| COVER (TSE:5253) | ¥1612.00 | ¥3143.38 | 48.7% |

| Citicore Renewable Energy (PSE:CREC) | ₱4.39 | ₱8.48 | 48.2% |

| Addvalue Technologies (SGX:A31) | SGD0.132 | SGD0.26 | 49.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

KoMiCo (KOSDAQ:A183300)

Overview: KoMiCo Ltd. is a company that offers semiconductor equipment cleaning and coating products across South Korea, the United States, China, Taiwan, and Singapore with a market cap of ₩1.68 trillion.

Operations: The company's revenue is primarily derived from its semiconductor equipment and services segment, amounting to ₩626.21 billion.

Estimated Discount To Fair Value: 13.5%

KoMiCo is trading at ₩83,300, which is 13.5% below its fair value estimate of ₩96,346.5 based on discounted cash flow analysis. The stock recently underwent a 2:1 split in May 2026. While revenue growth at 18% annually outpaces the Korean market's average, earnings growth forecasts are slightly behind market expectations. Despite high Return on Equity projections and significant earnings growth potential, KoMiCo's debt coverage by operating cash flow remains suboptimal.

- Upon reviewing our latest growth report, KoMiCo's projected financial performance appears quite optimistic.

- Take a closer look at KoMiCo's balance sheet health here in our report.

Plover Bay Technologies (SEHK:1523)

Overview: Plover Bay Technologies Limited is an investment holding company that designs, develops, and markets software-defined wide area network routers and related products, with a market cap of HK$8.93 billion.

Operations: The company's revenue segments include Sales of SD-WAN Routers - Fixed First Connectivity at $17.74 million, Sales of SD-WAN Routers - Mobile First Connectivity at $73.08 million, and Software Licenses and Warranty and Support Services totaling $39.32 million.

Estimated Discount To Fair Value: 12.2%

Plover Bay Technologies is trading at HK$8.07, slightly below its estimated future cash flow value of HK$9.19, indicating a modest undervaluation. Earnings are forecast to grow 15.18% annually, surpassing the Hong Kong market average of 12.6%. However, its dividend yield of 4.28% isn't fully supported by free cash flows. Recent board changes bring experienced leadership in electronics and logistics, potentially enhancing strategic direction and governance effectiveness.

- According our earnings growth report, there's an indication that Plover Bay Technologies might be ready to expand.

- Delve into the full analysis health report here for a deeper understanding of Plover Bay Technologies.

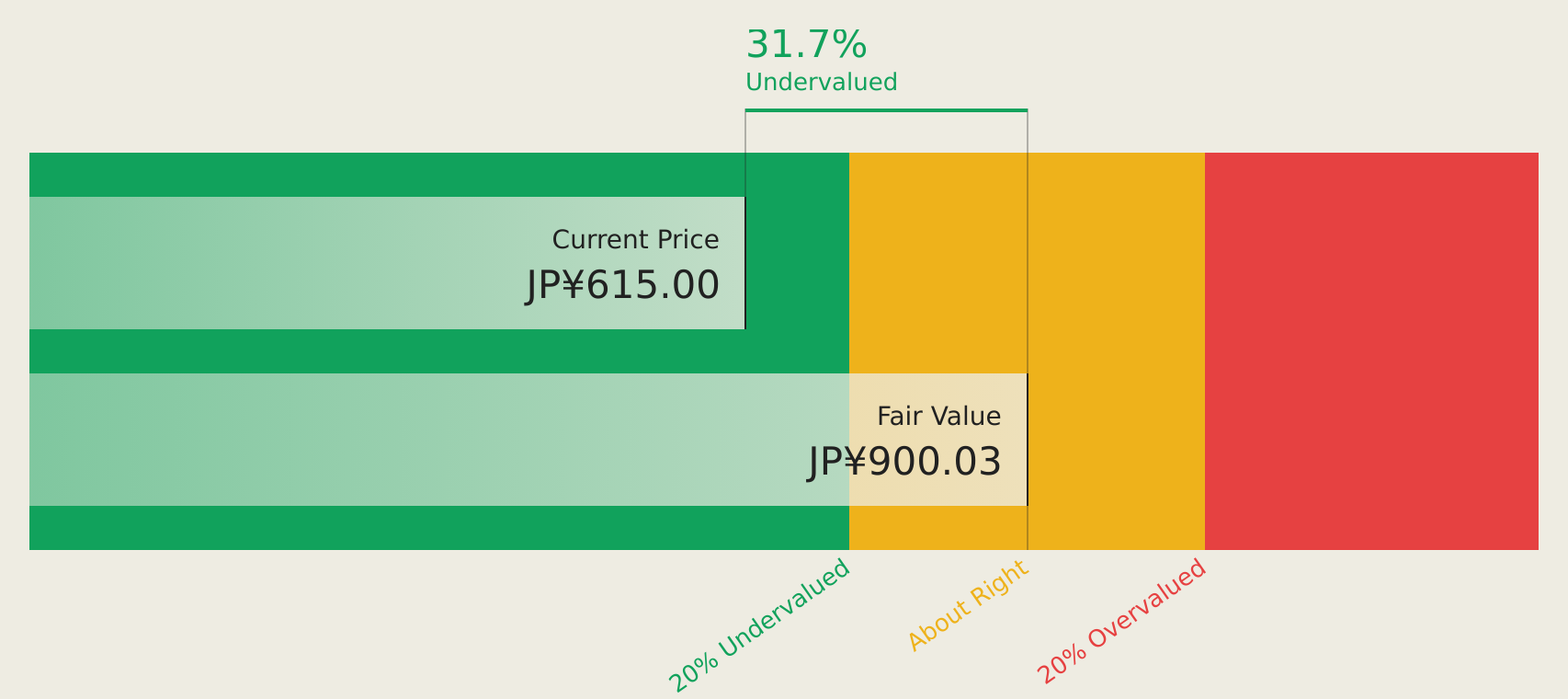

GENDA (TSE:9166)

Overview: GENDA Inc., with a market cap of ¥108.95 billion, operates amusement arcades like GiGO and the karaoke chain BanBan across North America, mainland China, Hong Kong, Taiwan, the United Kingdom, Vietnam, the Netherlands, Canada, and Singapore.

Operations: The company's revenue is primarily derived from its Entertainment Platform segment, which accounts for ¥171.42 billion, followed by the Entertainment Content segment contributing ¥23.56 billion.

Estimated Discount To Fair Value: 34.9%

GENDA is trading at ¥580, significantly below its estimated future cash flow value of ¥891.38, highlighting undervaluation potential. Despite recent share price volatility and debt concerns relative to operating cash flow, earnings are projected to grow significantly over the next three years, outpacing the Japanese market. Recent activities include a completed buyback of 177,100 shares for ¥108.77 million and a fixed-income offering of ¥7 billion in corporate bonds due April 2028.

- Our growth report here indicates GENDA may be poised for an improving outlook.

- Get an in-depth perspective on GENDA's balance sheet by reading our health report here.

Key Takeaways

- Delve into our full catalog of 187 Undervalued Asian Stocks Based On Cash Flows here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com