In recent weeks, the European market has faced volatility amid geopolitical tensions and discussions around potential European Central Bank tightening, with the STOXX Europe 600 Index declining by 1.79%. Despite these challenges, some small-cap stocks in Europe may present opportunities for investors looking to navigate this uncertain landscape. Identifying promising small-cap stocks often involves examining factors such as insider buying trends and evaluating their resilience in fluctuating economic conditions.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.6x | 4.5x | 39.18% | ★★★★★★ |

| Ratos | NA | 0.6x | 38.44% | ★★★★★★ |

| Eurocell | 11.1x | 0.3x | 49.45% | ★★★★★☆ |

| Nyab | 17.5x | 0.7x | 40.78% | ★★★★★☆ |

| Nederman Holding | 17.0x | 0.8x | 36.45% | ★★★★★☆ |

| Close Brothers Group | NA | 0.9x | 42.94% | ★★★★★☆ |

| Bilia | 16.2x | 0.3x | 42.06% | ★★★★☆☆ |

| NoHo Partners Oyj | 16.7x | 0.4x | 34.60% | ★★★★☆☆ |

| AB Dynamics | NA | 2.3x | 33.02% | ★★★☆☆☆ |

| CVS Group | 51.8x | 1.2x | 47.87% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

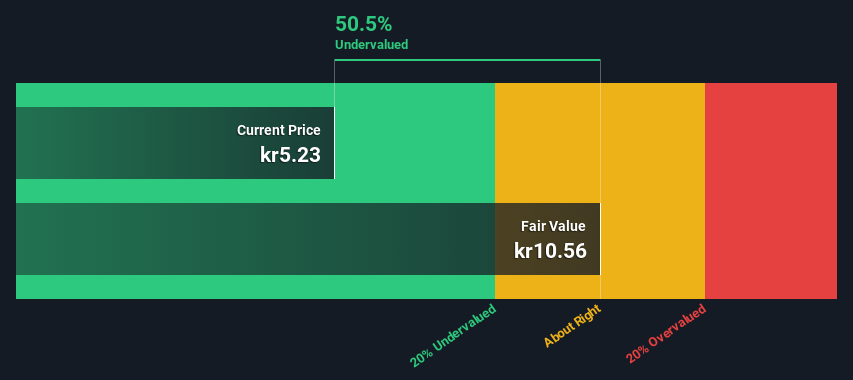

Krona Public Real Estate (DB:927)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Krona Public Real Estate focuses on rental operations within the real estate sector, with a market capitalization of approximately SEK 1.5 billion.

Operations: The company generates revenue primarily through its real estate rental segment. Over recent periods, the gross profit margin showed a downward trend from 95.50% to 83.88%. Operating expenses include general and administrative costs, which were SEK 6.25 million in the latest period, while non-operating expenses have seen fluctuations impacting net income margins significantly.

PE: 8.1x

Krona Public Real Estate, a small European company, shows potential as an undervalued stock. Recent earnings for Q1 2026 reveal sales of SEK 22.74 million and net income doubling to SEK 20.13 million from the previous year, despite a slight dip in EPS from continuing operations. Insider confidence is evident with Tomas Georgiadis purchasing shares worth approximately SEK 575,462 earlier this year. Although reliant on external borrowing, the company's financial position remains stable with manageable interest payments.

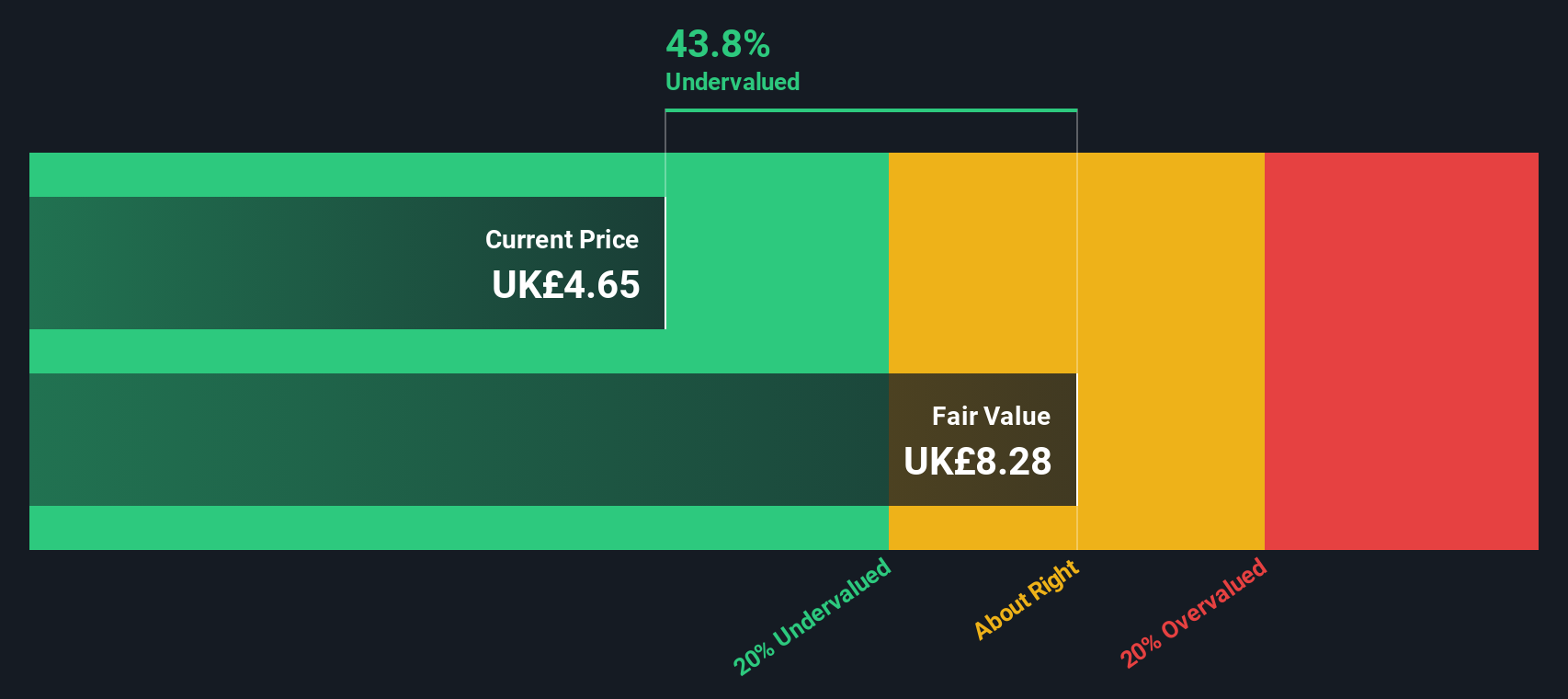

PayPoint (LSE:PAY)

Simply Wall St Value Rating: ★★★★★☆

Overview: PayPoint is a company that operates in the payment and consumer services industry, providing solutions such as bill payments, top-ups, and retail services with a market cap of approximately £0.45 billion.

Operations: The company's revenue streams are primarily driven by its Love2shop and Pay Point segments, with recent figures showing a combined revenue of £337.01 million. The gross profit margin has experienced fluctuations, reaching as high as 66.44% in the past but recently recorded at 42.83%. Operating expenses have been a significant component, with general and administrative expenses consistently forming a substantial part of these costs over time.

PE: 9.0x

PayPoint, a smaller company in Europe, has shown significant financial progress with sales reaching £305.62 million and net income doubling to £39.33 million for the year ending March 2026. The company completed a substantial share repurchase program, buying back 10.6% of shares for £45 million since June 2024, indicating strong insider confidence. Despite relying on riskier external borrowing, PayPoint's earnings are projected to grow over 10% annually, suggesting potential value in its future trajectory.

- Take a closer look at PayPoint's potential here in our valuation report.

Examine PayPoint's past performance report to understand how it has performed in the past.

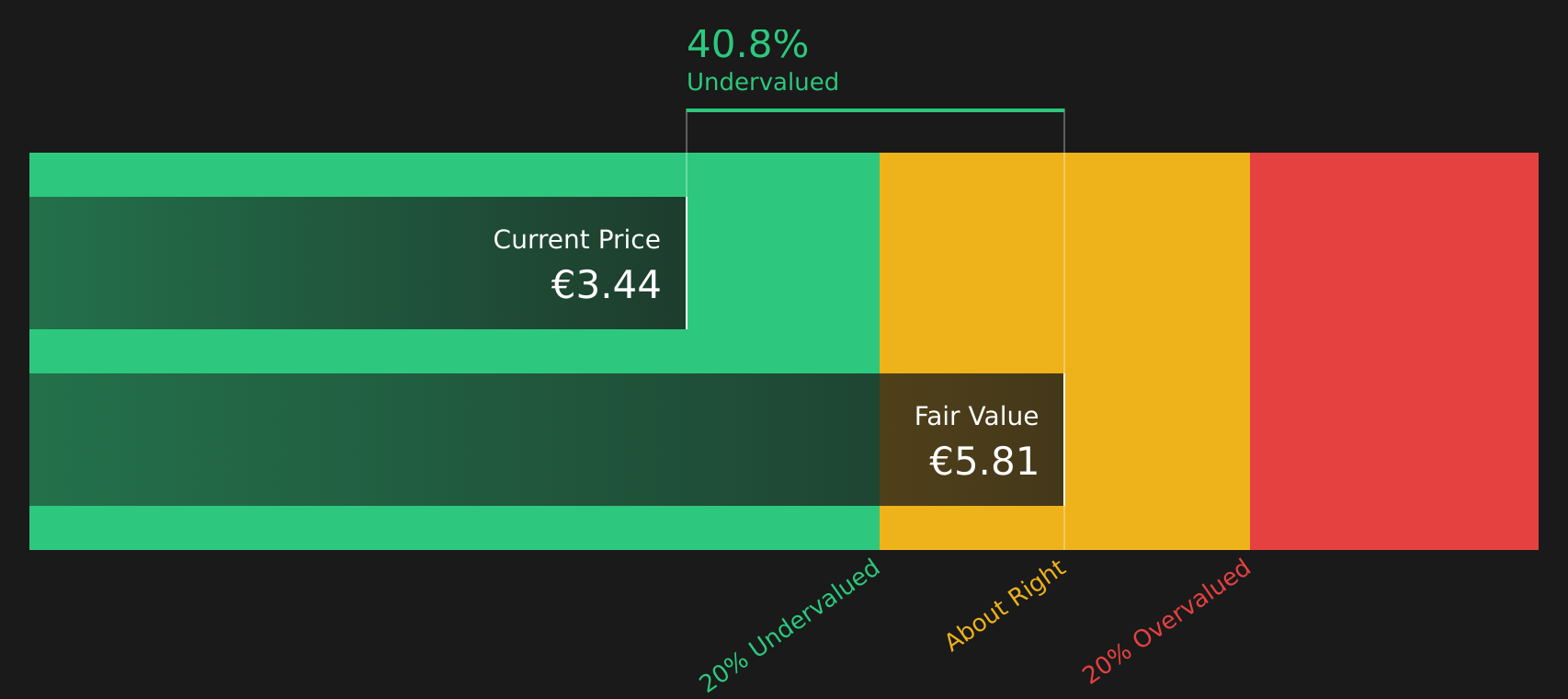

Nyab (OM:NYAB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Nyab is a company engaged in consulting and civil engineering services, with a market capitalization of €1.45 billion.

Operations: Nyab generates revenue primarily from its consulting and civil engineering segments, with civil engineering contributing the majority. The company's cost of goods sold (COGS) often represents a significant portion of its revenue, affecting the gross profit margin which has fluctuated around 21.68% to 24.64% over recent periods. Operating expenses include notable general and administrative costs, alongside depreciation and amortization expenses that impact overall profitability.

PE: 17.5x

Nyab, a European construction firm, is capturing attention with its recent contracts and insider confidence. The company secured a SEK 6.5 billion order for the Uppsala tramway project and an agreement to expand the Arlanda express maintenance depot in Sweden. Insiders have shown confidence by purchasing shares over the past year, indicating potential value recognition within this small company. Despite reliance on external borrowing for funding, Nyab's earnings are projected to grow annually by 12.72%, suggesting promising prospects ahead.

- Get an in-depth perspective on Nyab's performance by reading our valuation report here.

Gain insights into Nyab's past trends and performance with our Past report.

Next Steps

- Reveal the 58 hidden gems among our Undervalued European Small Caps With Insider Buying screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com