In July 2026, global markets are navigating a complex landscape marked by geopolitical tensions in the Middle East and fluctuating energy prices, with U.S. small-cap stocks experiencing a slight decline as reflected by the Russell 2000 Index's recent dip of 0.61%. Amid this backdrop, investors are closely examining small-cap companies for potential opportunities, particularly those exhibiting strong fundamentals and insider activity that may signal confidence in their future prospects.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.6x | 4.5x | 39.18% | ★★★★★★ |

| Centurion | 11.4x | 3.9x | 34.99% | ★★★★★★ |

| Firan Technology Group | 39.2x | 2.9x | 21.39% | ★★★★☆☆ |

| NoHo Partners Oyj | 16.7x | 0.4x | 34.60% | ★★★★☆☆ |

| Primaris Real Estate Investment Trust | 13.6x | 3.9x | 44.75% | ★★★★☆☆ |

| Nexus Industrial REIT | 10.0x | 3.4x | 7.06% | ★★★★☆☆ |

| Sagicor Financial | 31.6x | 0.6x | 35.95% | ★★★★☆☆ |

| Pizza Pizza Royalty | 14.4x | 11.0x | 31.57% | ★★★☆☆☆ |

| Chinasoft International | 21.3x | 0.4x | -2605.79% | ★★★☆☆☆ |

| CVS Group | 51.8x | 1.2x | 47.87% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

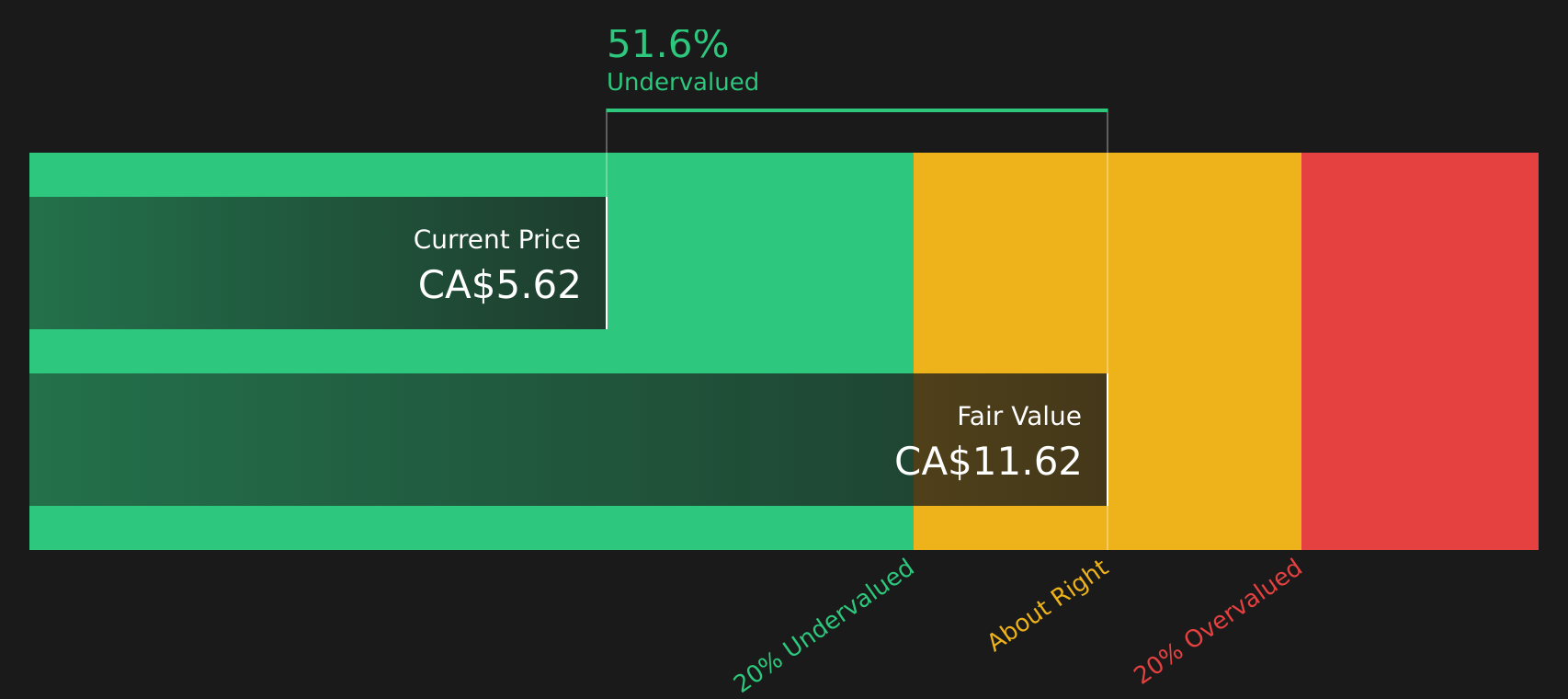

Hemlo Mining (TSX:HMMC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hemlo Mining is a Canadian company focused on the exploration and development of gold mining projects, with a market capitalization of C$2.35 billion.

Operations: Hemlo Mining's revenue is primarily derived from its operations, with a significant portion of costs attributed to the cost of goods sold (COGS) and operating expenses. The company's gross profit margin exhibited fluctuations, reaching 43.77% in March 2021 and dipping to lower levels during other periods. Operating expenses are consistently present, with general and administrative expenses being a notable component. Non-operating expenses have also been substantial in certain periods, impacting net income results significantly.

PE: -90.2x

Hemlo Mining, a smaller company in the mining sector, has shown potential for growth with its recent updates. The company announced an increase in gold resources at its Hemlo Gold Mine, highlighting a 34% rise in measured and indicated resources compared to last year. Insider confidence is evident as Jonathan Awde purchased 55,000 shares valued at US$357,416. Despite past shareholder dilution and reliance on external borrowing for funding, the company's strategic drilling program and new board appointments suggest efforts toward enhancing resource value and governance.

- Delve into the full analysis valuation report here for a deeper understanding of Hemlo Mining.

Gain insights into Hemlo Mining's past trends and performance with our Past report.

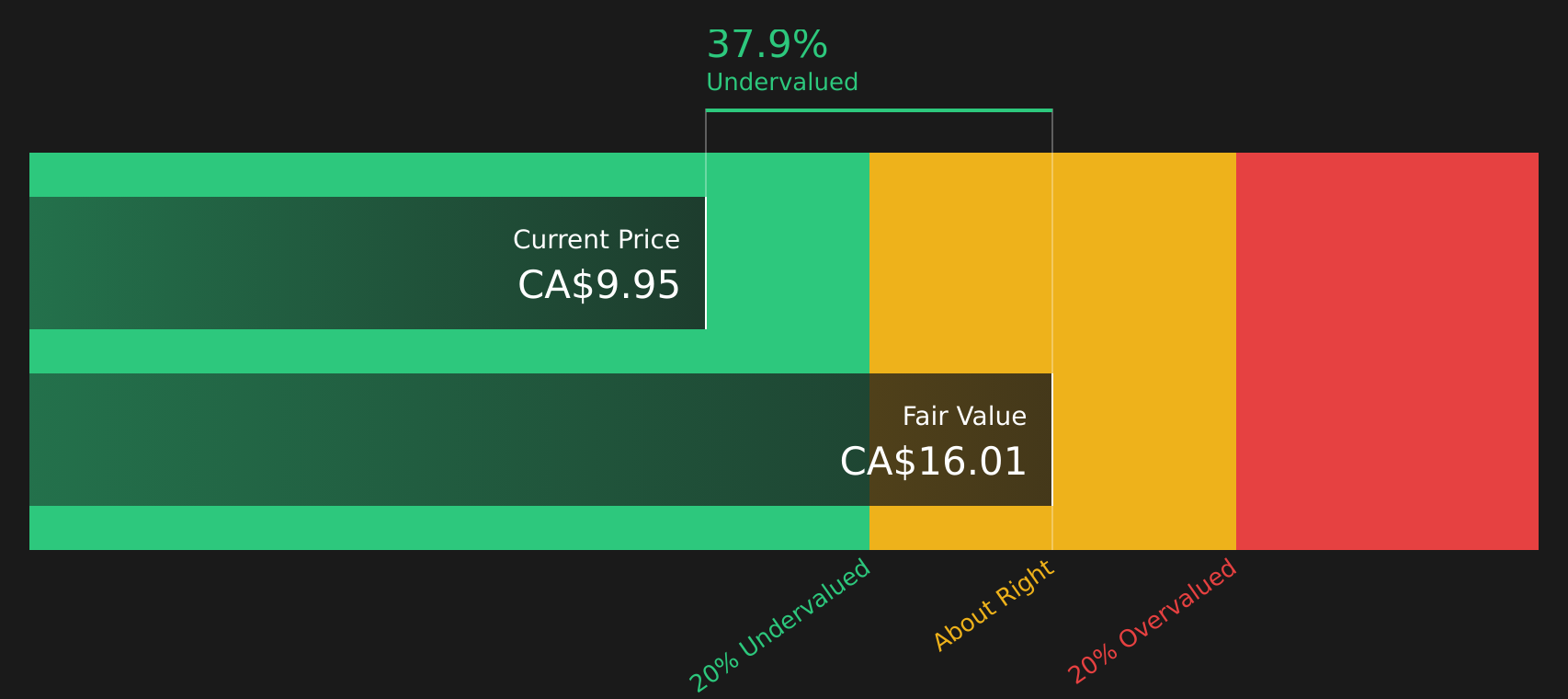

Martinrea International (TSX:MRE)

Simply Wall St Value Rating: ★★★★★★

Overview: Martinrea International is a Canadian company specializing in the production of automotive parts and accessories, with a market capitalization of CA$1.17 billion.

Operations: The company generates revenue primarily from the Auto Parts & Accessories segment, with recent figures showing CA$4.78 billion in revenue. The cost of goods sold (COGS) is CA$3.86 billion, leading to a gross profit of CA$922.24 million and a gross profit margin of 19.30%. Operating expenses are significant at CA$661.49 million, impacting net income figures which show some variability over time with the latest net income being CA$117.37 million and a net income margin of 2.46%.

PE: 6.0x

Martinrea International, a smaller company in its sector, has shown significant insider confidence with recent share purchases. Between January and March 2026, they repurchased 1.9 million shares for C$19 million under their buyback program. Despite high debt levels due to reliance on external borrowing, the firm reported Q1 net income of C$27.85 million, up from C$17.47 million the previous year. With projected sales between $4.5 billion and $4.9 billion for 2026, Martinrea's growth potential remains promising amidst current financial challenges.

- Dive into the specifics of Martinrea International here with our thorough valuation report.

Learn about Martinrea International's historical performance.

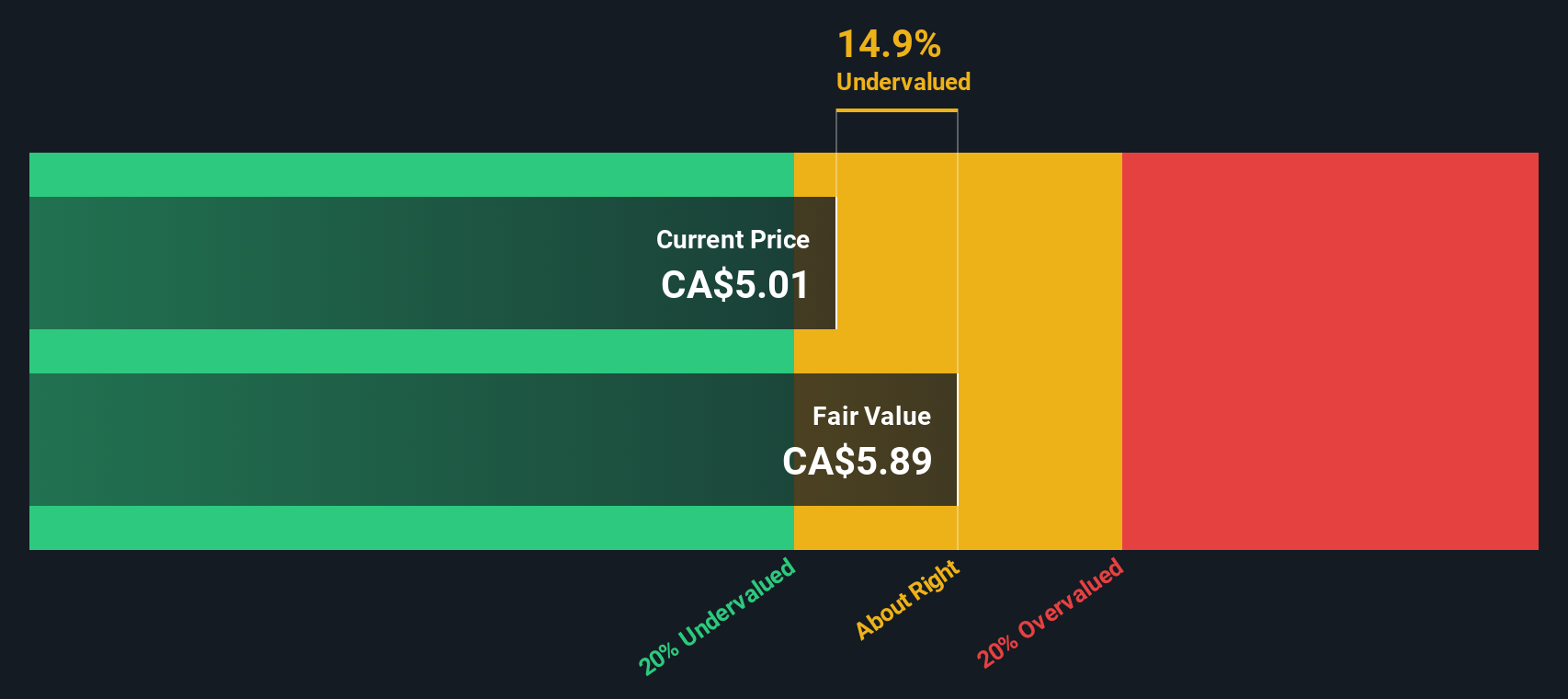

Vital Infrastructure Property Trust (TSX:VITL.UN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Vital Infrastructure Property Trust operates in the healthcare real estate sector with a focus on managing properties, and it has a market capitalization of CA$1.24 billion.

Operations: The company generates revenue primarily from the healthcare real estate sector, with a recent quarterly revenue of CA$426.66 million. The cost of goods sold (COGS) was CA$102.47 million, leading to a gross profit margin of 75.98%. Operating expenses were reported at CA$56.27 million, contributing to a net income loss of -CA$55.81 million and a net income margin of -13.08%.

PE: -25.3x

Vital Infrastructure Property Trust, a smaller company in its field, faces challenges with its reliance on external borrowing for funding. Despite being dropped from several indices in June 2026, the trust maintains a steady monthly dividend of CAD 0.03 per share. Earnings forecasts suggest significant growth at 132% annually, indicating potential for future recovery and expansion. However, recent financials show decreased sales of CAD 74 million and a net loss of CAD 3.85 million for Q1 2026 compared to last year.

- Click here to discover the nuances of Vital Infrastructure Property Trust with our detailed analytical valuation report.

Understand Vital Infrastructure Property Trust's track record by examining our Past report.

Turning Ideas Into Actions

- Unlock our comprehensive list of 131 Undervalued Global Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com