Amidst a backdrop of geopolitical tensions affecting global markets, Australian investors are facing a challenging environment with the ASX showing signs of volatility due to international events. In such uncertain times, growth companies with high insider ownership can be appealing as they often signal management's confidence in the business and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Torque Metals (ASX:TOR) | 18.6% | 94.2% |

| Starpharma Holdings (ASX:SPL) | 21.8% | 91.8% |

| SKS Technologies Group (ASX:SKS) | 28.2% | 42.4% |

| Predictive Discovery (ASX:PDI) | 10.5% | 65.1% |

| Pinnacle Investment Management Group (ASX:PNI) | 25% | 21.2% |

| Forrestania Resources (ASX:FRS) | 38.3% | 126.7% |

| Austral Resources Australia (ASX:AR1) | 20% | 38.7% |

| Auric Mining (ASX:AWJ) | 19.6% | 29.2% |

| Adveritas (ASX:AV1) | 17.6% | 108.4% |

| Advanced Energy Minerals (ASX:AEM) | 35.1% | 48.5% |

Let's dive into some prime choices out of the screener.

Energy One (ASX:EOL)

Simply Wall St Growth Rating: ★★★★☆☆

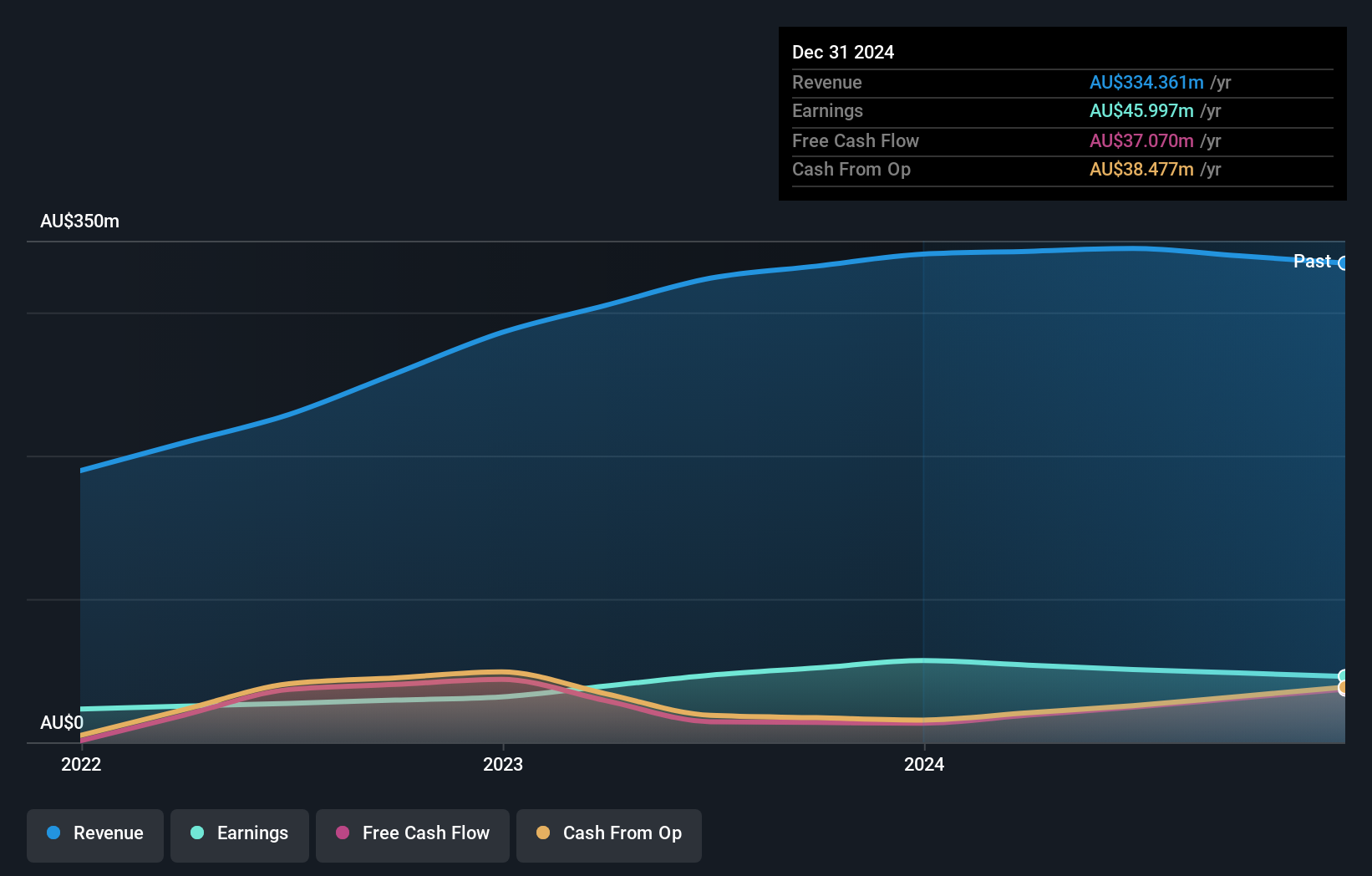

Overview: Energy One Limited provides software products, outsourced operations, and advisory services to wholesale energy, environmental, and carbon trading markets in Australasia and Europe, with a market cap of A$376.97 million.

Operations: Energy One Limited generates revenue primarily from its Energy Software Industry segment, amounting to A$67.01 million.

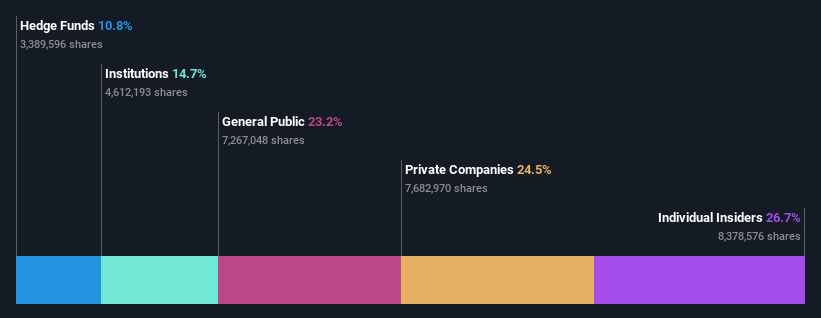

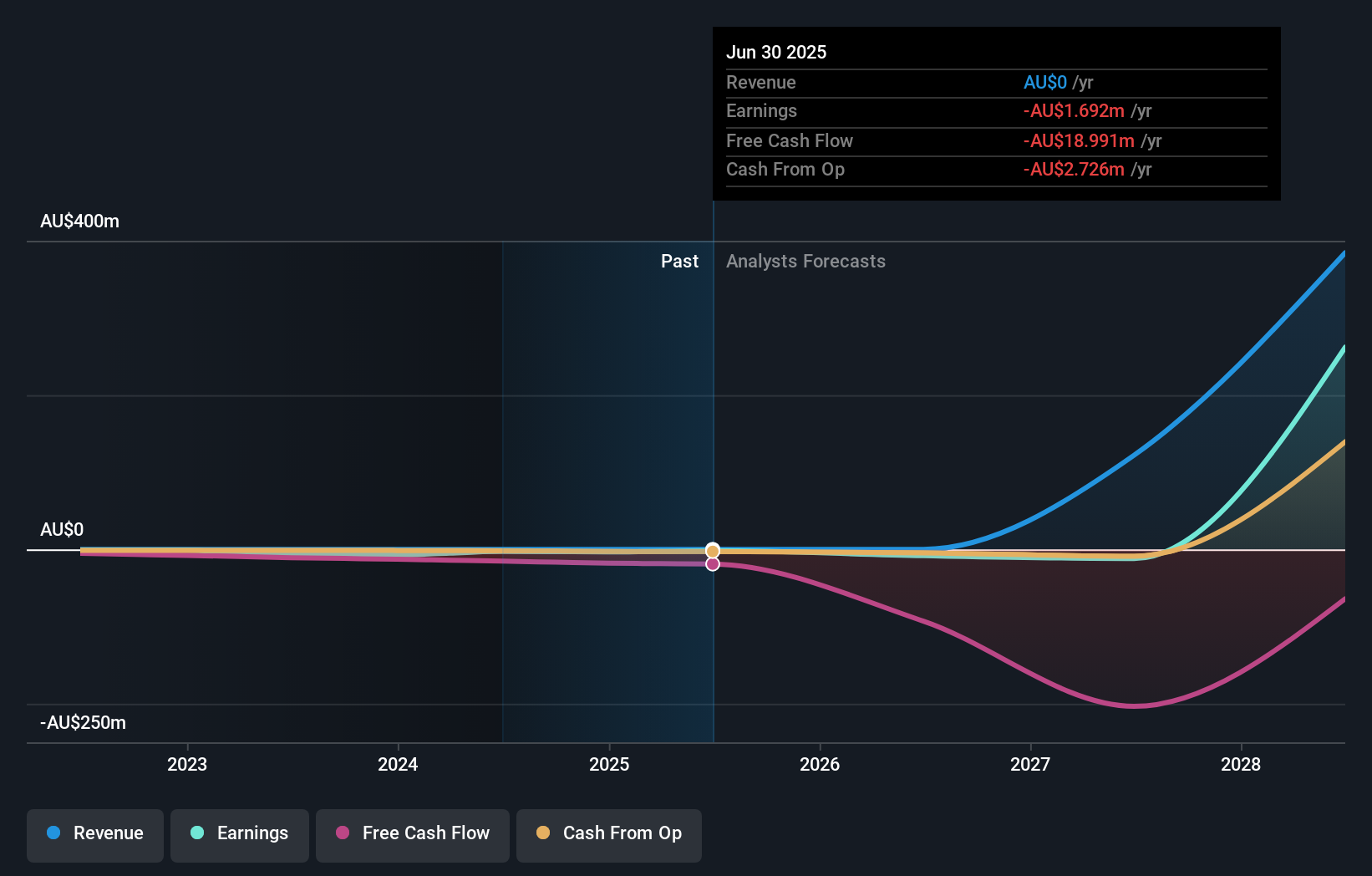

Insider Ownership: 23.9%

Revenue Growth Forecast: 12.2% p.a.

Energy One demonstrates strong growth potential with earnings expected to increase significantly at 26.4% annually, outpacing the Australian market. Despite a forecasted low return on equity of 18.5%, the company's valuation appears attractive, trading below fair value and analyst price targets suggesting a rise of 51.5%. Recent executive changes bring in Jason Mabee as CFO, leveraging his extensive finance experience to support Energy One's global expansion and disciplined financial governance.

- Click to explore a detailed breakdown of our findings in Energy One's earnings growth report.

- The valuation report we've compiled suggests that Energy One's current price could be inflated.

Lycopodium (ASX:LYL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lycopodium Limited offers engineering and project delivery services across the resources, rail infrastructure, and industrial processes sectors in Australia, with a market cap of A$721.07 million.

Operations: The company's revenue segments include engineering and project delivery services in the resources, rail infrastructure, and industrial processes sectors, totaling A$375.36 million.

Insider Ownership: 32.8%

Revenue Growth Forecast: 17% p.a.

Lycopodium's growth prospects are underscored by forecasts of revenue and earnings increasing at 17% and 16.4% annually, respectively, outpacing the broader Australian market. The company trades at a significant discount to its estimated fair value, enhancing its appeal. Lycopodium's return on equity is projected to reach a robust 27.6% in three years. Recent insider trading data is unavailable, but the company's financial outlook remains strong without substantial insider buying or selling activity reported recently.

- Click here to discover the nuances of Lycopodium with our detailed analytical future growth report.

- Our expertly prepared valuation report Lycopodium implies its share price may be lower than expected.

Santana Minerals (ASX:SMI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Santana Minerals Limited is involved in the exploration and evaluation of gold properties across New Zealand, Cambodia, and Mexico, with a market cap of A$448.52 million.

Operations: The company focuses on the exploration and evaluation of gold properties in New Zealand, Cambodia, and Mexico.

Insider Ownership: 12.1%

Revenue Growth Forecast: 59.1% p.a.

Santana Minerals is poised for significant growth, with revenue expected to increase by over 59% annually, surpassing market averages. The company anticipates becoming profitable within three years, driven by robust earnings growth forecasts of 145.15% per year. Recent insider activity shows substantial buying with no major selling, indicating confidence in the company's prospects. Santana's recent high-grade gold intercepts at the Rise and Shine deposit support potential expansion and value creation for shareholders.

- Navigate through the intricacies of Santana Minerals with our comprehensive analyst estimates report here.

- Our valuation report here indicates Santana Minerals may be overvalued.

Make It Happen

- Discover the full array of 101 Fast Growing ASX Companies With High Insider Ownership right here.

- Want To Explore Some Alternatives? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com