As global markets navigate through geopolitical tensions and fluctuating energy prices, the Asian market presents unique opportunities for investors seeking growth in small-cap stocks. In this environment, identifying companies with strong fundamentals becomes crucial, as they are more likely to withstand market volatility and capitalize on emerging trends.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Hyundai Home Shopping Network | 6.43% | 16.06% | -2.84% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

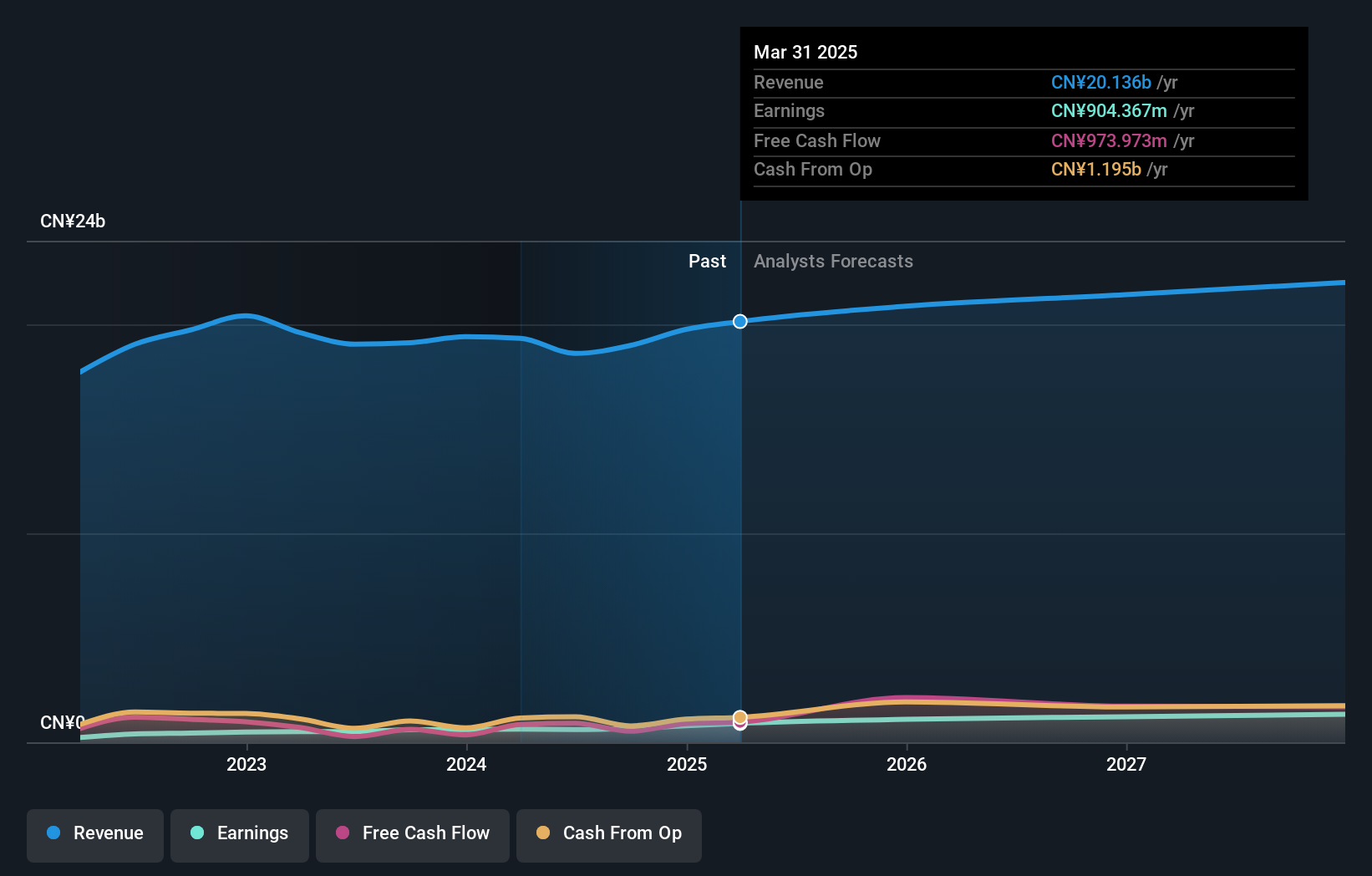

Zhuzhou Smelter GroupLtd (SHSE:600961)

Simply Wall St Value Rating: ★★★★★★

Overview: Zhuzhou Smelter Group Co., Ltd. operates in China, producing and selling zinc and its alloy products under the Torch brand, with a market cap of CN¥27.30 billion.

Operations: Zhuzhou Smelter Group Co., Ltd. generates revenue primarily from its lead and zinc products, amounting to CN¥24.45 billion. The company's net profit margin is a critical metric to consider when evaluating its financial performance.

Zhuzhou Smelter Group, a nimble player in the metals and mining sector, has shown impressive growth with its earnings surging 120.3% over the past year, outpacing the industry average of 21.7%. The company reported a significant rise in net income to CNY 1.14 billion for Q1 2026 from CNY 276.92 million a year earlier, reflecting robust operational performance. Trading at about 34.2% below estimated fair value suggests potential upside for investors seeking undervalued opportunities. Despite recent share price volatility, Zhuzhou's financial health is underscored by its strong cash position exceeding total debt and well-covered interest obligations (108x EBIT coverage).

- Dive into the specifics of Zhuzhou Smelter GroupLtd here with our thorough health report.

Assess Zhuzhou Smelter GroupLtd's past performance with our detailed historical performance reports.

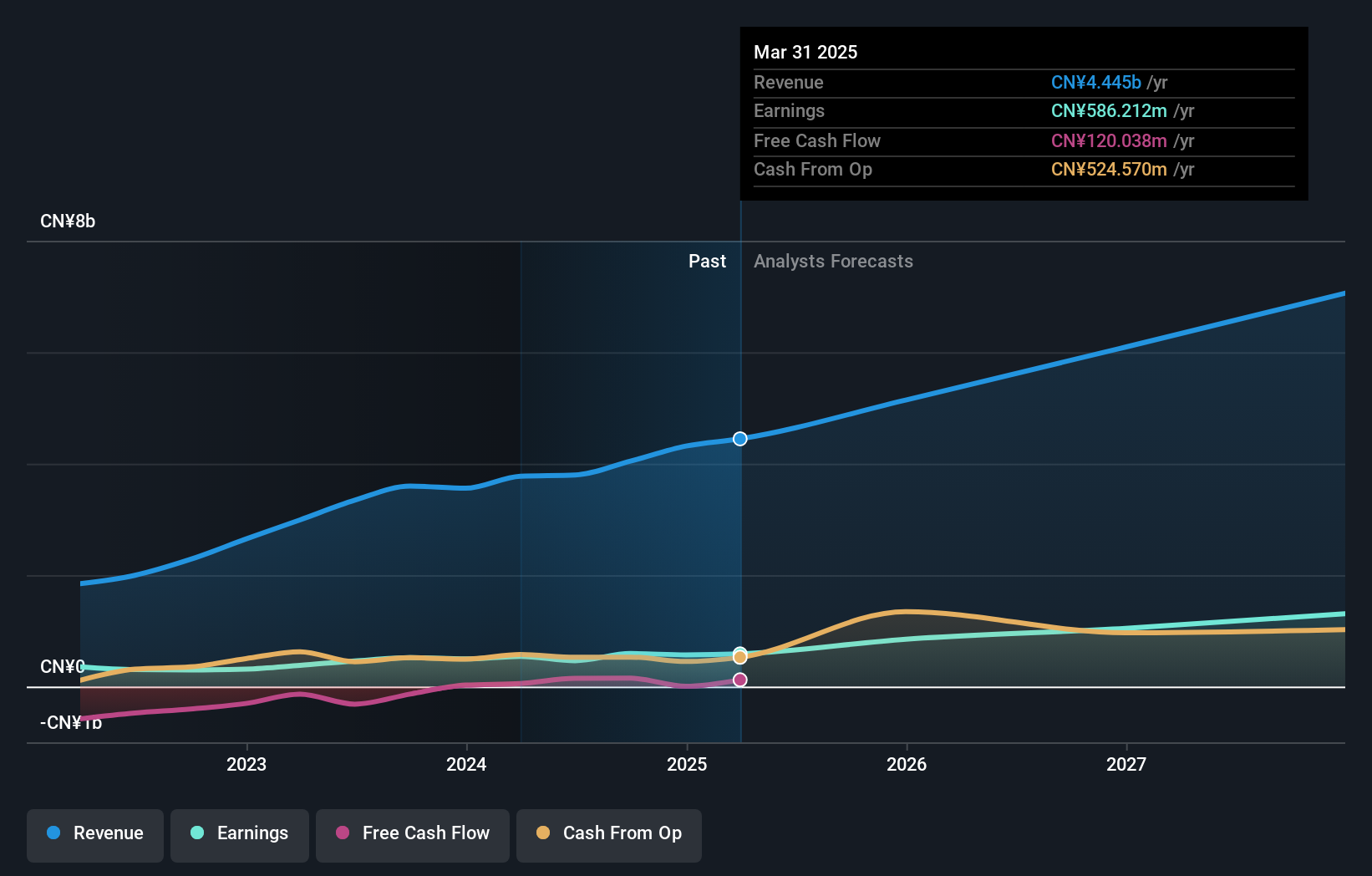

Raytron TechnologyLtd (SHSE:688002)

Simply Wall St Value Rating: ★★★★★☆

Overview: Raytron Technology Co., Ltd. specializes in the design and manufacturing of application-specific integrated circuits and special chips, with a market capitalization of CN¥65.36 billion.

Operations: Raytron Technology generates revenue primarily from the design and manufacturing of application-specific integrated circuits and special chips. The company has a market capitalization of CN¥65.36 billion.

Raytron Technology, a nimble player in the infrared imaging space, has shown impressive momentum with its earnings surging by 148.6% over the past year, far outpacing the electronic industry's growth of 9.6%. This financial leap is underscored by a net income of CNY 478.74 million for Q1 2026 compared to CNY 145.82 million last year. Despite a debt-to-equity ratio increase to 17.5% over five years, Raytron's interest payments are comfortably covered at an impressive EBIT coverage of 349 times. Trading at about 70% below estimated fair value suggests potential upside for investors keeping an eye on this promising entity in Asia's tech landscape.

- Get an in-depth perspective on Raytron TechnologyLtd's performance by reading our health report here.

Gain insights into Raytron TechnologyLtd's past trends and performance with our Past report.

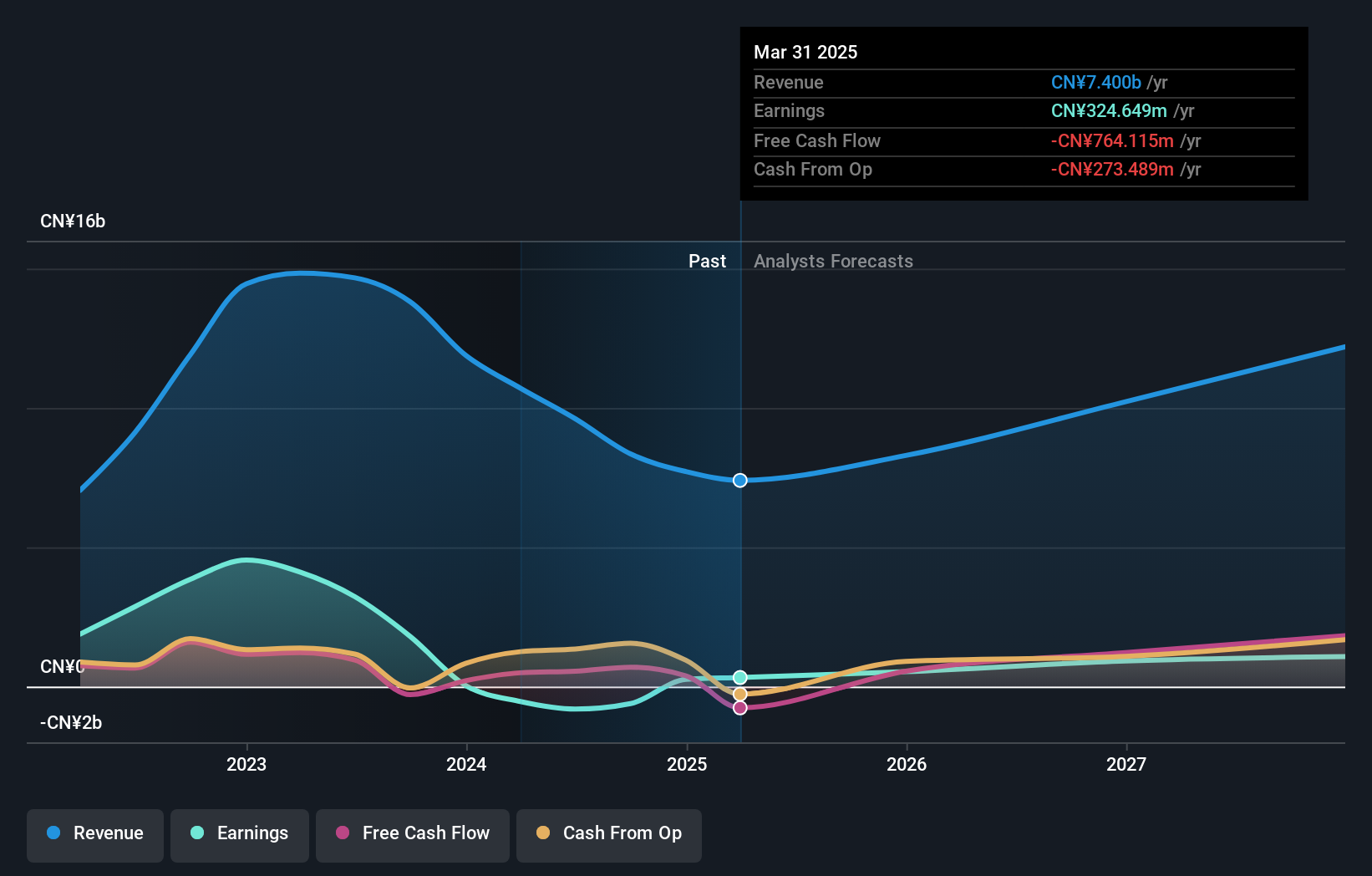

Sichuan Yahua Industrial Group (SZSE:002497)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Sichuan Yahua Industrial Group Co., Ltd. operates in the lithium and civil explosives sectors both domestically and internationally, with a market capitalization of CN¥20.72 billion.

Operations: The company generates revenue primarily from its lithium and civil explosives segments. The net profit margin has shown fluctuations, indicating variability in profitability.

Yahua Industrial, a notable player in the chemicals sector, has demonstrated remarkable growth with earnings surging 173.8% over the past year, surpassing industry averages. The company reported a significant net income increase to CNY 338.82 million for Q1 2026 from CNY 82.46 million the previous year, reflecting robust operational performance. Despite its debt-to-equity ratio rising from 5.1% to 9.9% over five years, Yahua still maintains more cash than total debt, indicating financial stability and resilience against interest obligations. Trading at a value significantly below its estimated fair value suggests potential investment appeal amidst recent dividend increases approved at their AGM in May 2026.

Make It Happen

- Click here to access our complete index of 110 Asian Undiscovered Gems With Strong Fundamentals.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com