Brinker International stock has logged a very large 3 year gain while both the Discounted Cash Flow (DCF) intrinsic value estimate and traditional earnings multiples still suggest the shares trade at a discount to what the business may be worth.

- Over the last 3 years, Brinker International has delivered a very large total return of 406.6%, which puts extra focus on whether the current price still leaves room for more upside based on fundamentals.

- Index inclusion in the Russell 2000 Defensive indexes and fresh marketing around Chili’s new margarita promotion can support sentiment and revenue, while rising wage and commodity costs remain a key risk for margins and cash generation.

- Brinker International screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and market multiples, yet its broader valuation checks are mixed, with the stock passing 4 of 6 tests, which you can see in more detail at 4/6.

The issue now is whether Brinker International’s recent share price strength has already captured this apparent discount or if the gap between market price and intrinsic value still offers a margin of safety.

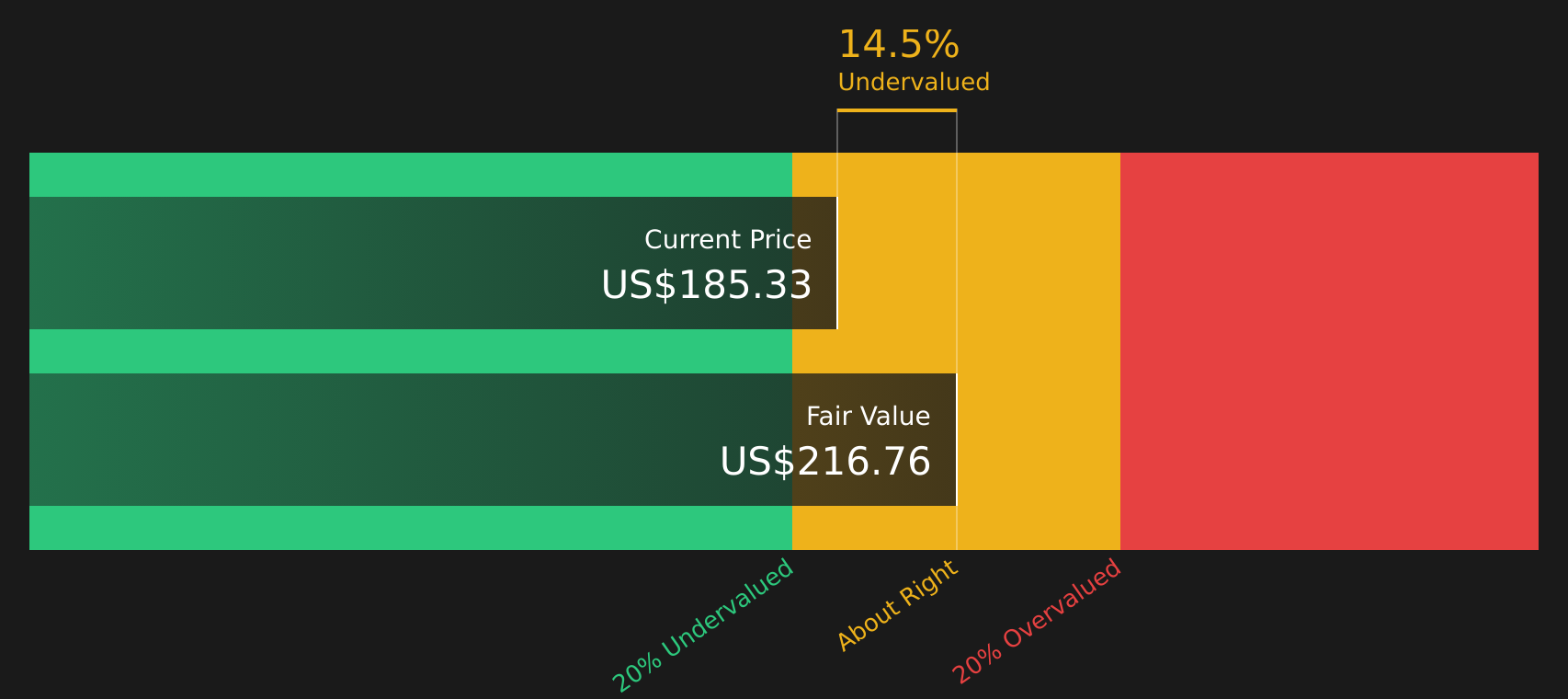

Does Brinker International Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) approach estimates what Brinker International might be worth based on the cash it can generate for shareholders. The model uses the latest twelve month free cash flow of about $498.3 million and assumes that cash flows continue growing from this base, resulting in an intrinsic value estimate of about $216 per share. That outcome is roughly 12.4% above the current share price, so under this framework the stock appears to trade at a discount to its projected cash generation in dollars.

Brinker International’s inclusion in the Russell 2000 Defensive indexes helps explain why interest in the stock has picked up. However, the DCF outcome suggests the market price still sits below the level supported by its modeled cash flows. This type of model depends on steady execution and on free cash flow remaining close to the projected path instead of being pressured by factors such as higher wage or commodity costs.

On balance, the Discounted Cash Flow analysis indicates that Brinker International stock currently appears undervalued relative to this estimate of intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Brinker International is undervalued by 12.4%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Is Brinker International Still Cheap on Earnings?

P/E is a useful way to look at Brinker International because earnings are a key focus for mature restaurant operators. The stock trades on a P/E of about 17.5x, compared with an industry average of roughly 24.2x and a peer group average of 74.5x in the wider Hospitality space, which places Brinker International toward the lower end of the earnings valuation range.

On Simply Wall St’s fair P/E estimate of 20.0x, which reflects the company’s sector, size and risk profile, Brinker International also trades below what this framework suggests might be reasonable. The difference between a current 17.5x and a fair 20.0x indicates the market is assigning a discount to the stock’s earnings, even after its 3 year share price performance and recent index inclusion.

Taken together, these earnings multiples indicate that Brinker International stock appears undervalued on a P/E basis.

See what the numbers say about this price — find out in our valuation breakdown.

The Brinker International Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Brinker International valuation puzzle leaves off by spelling out which paths for growth, margins and earnings would need to play out for the stock to be worth materially more or less than today’s price, and they sit on the company’s Community page. Rather than relying on a single multiple or model output, each Narrative lays out the assumptions behind its fair value view so you can compare them with Brinker International’s actual results over time.

Community narratives on Brinker International sit far apart, with one side seeing meaningful upside while the other questions how much earnings power the current price assumes.

Bull case: 10% undervalued

"JPMorgan, in particular, has framed Chili's current performance as a potential engine for reinvestment and expansion, which bullish analysts see as strengthening the case for Brinker to sustain its operating improvements and support its current multiple..."

Read the full Bull Case to see why Brinker International could be undervalued

Bear case: 28% overvalued

"The full-service casual dining model faces increasing threat from fast casual and limited service competitors, who capture a growing share of out-of-home dining spend; as market fragmentation intensifies, Brinker's core business could experience structural margin compression and underlying declines in both traffic and earnings power..."

Read the full Bear Case to see why Brinker International could be overvalued

Do you think there's more to the story for Brinker International? Head over to our Community to see what others are saying!

The Bottom Line

For Brinker International, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiples still point to an undervalued stock, even after a very large 3 year move. The key question is whether the discount reflects lingering concern that wage and commodity pressures could squeeze margins and free cash flow, or whether the market is underestimating the company’s ability to hold its operating improvements. From here, the crux of the bull versus bear debate is whether Chili’s performance and broader execution can support margins well enough for that apparent valuation gap to close, rather than become a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com