Volkswagen’s plan to cut tens of thousands of jobs and trim production is a sharp reminder that industrial giants can change course quickly when costs look out of line. For investors, this kind of restructuring risk, and potential efficiency gain, can reshape the outlook for companies far beyond VW itself. The screener used for this article focuses on larger Industrials and Automobiles stocks that are explicitly talking about restructuring or operational efficiency. Below, you will see 3 stocks that could be positively exposed to the same pressures now bearing down on Volkswagen.

ATS (TSX:ATS)

Overview: ATS is a Canada based automation specialist that designs, builds, and services complex manufacturing systems, helping clients in areas such as life sciences, transportation, food and beverage, and energy run more reliable and efficient production lines.

Operations: ATS generates all of its CA$2.97b revenue from Automation Systems, with key markets including the United States (CA$1.27b), other European countries (CA$628.7m), Germany (CA$283.4m), and Canada (CA$196.4m).

Market Cap: CA$3.9b

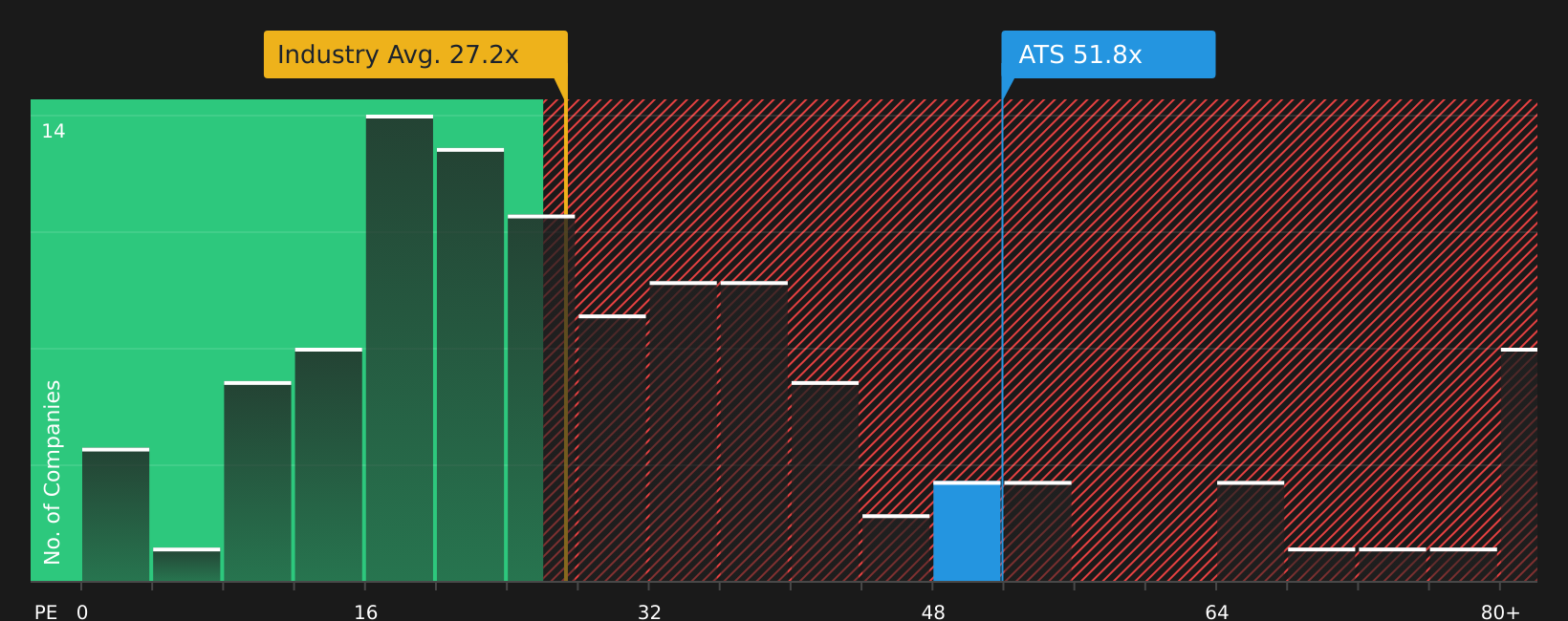

Volkswagen’s cost cuts highlight why investors are watching ATS closely, as carmakers and other manufacturers look for automation partners that can help trim overhead without hollowing out core capabilities. ATS sits at the center of this shift, with automation systems, digital tools, and lifecycle services that aim to improve margins and reduce downtime. Recent restructuring is intended to redeploy staff into higher growth areas like life sciences. At the same time, high leverage, interest coverage concerns, and a P/E that sits well above the industry mean the stock is not a low risk story. ATS is also coming off weaker historical earnings and softer orders in transportation, which raises the stakes for its efficiency push and the new CEO’s playbook.

ATS is working to translate higher-margin automation demand into a broader opportunity than its recent earnings softness might indicate, but the more detailed picture is examined in the 4 key rewards and 1 important major warning sign

Alstom (ENXTPA:ALO)

Overview: Alstom is a France based rail manufacturer that supplies trains, signaling systems, digital control solutions, and long term maintenance services to rail operators and asset owners across Europe, the Americas, Asia Pacific, and Africa. Its portfolio covers high speed and commuter trains, metros, trams, and infrastructure equipment that keep passenger and freight rail networks running.

Operations: Alstom generates all of its €19.17b revenue from Transport, with Europe excluding France (€8.10b), France (€3.51b), the Americas (€3.23b), Asia/Pacific (€2.55b), and Africa/Middle East/Central Asia (€1.78b) as key regions.

Market Cap: €7.1b

Alstom is in focus for investors watching how industrial restructuring can reshape returns, as the company works through legacy rolling stock contracts and project execution issues while placing more emphasis on higher margin Services and Signaling. Analysts note earnings growth forecasts above both the French market and machinery peers, a large order pipeline spanning Egypt and the AMECA region and projects such as TGV-M, and improving net profit margins as potential drivers of upside if execution improves. At the same time, funding is heavily reliant on external borrowings, low margin contracts still weigh on results, and supply chain and project delays have already led to one off hits. The key question for investors is whether Alstom’s operational changes and evolving business mix can justify its current P/E and the analysts’ higher price targets over time.

Alstom’s earnings forecasts and order pipeline suggest the real story may be how quickly profits could decouple from past project issues; get the full picture in the analyst forecasts for Alstom to see what might be hiding behind the headline risks

Kawasaki Heavy Industries (TSE:7012)

Overview: Kawasaki Heavy Industries is a Japan based industrial group that builds everything from aircraft, rail cars, ships and energy systems to motorcycles, construction machinery components and industrial robots, serving customers in transport, energy, manufacturing and defense around the world.

Operations: Kawasaki Heavy Industries generates most of its ¥2,311,267m revenue from Power Sports & Engine (¥683,960m), Aerospace Systems (¥627,944m), Energy Solution & Marine Engineering (¥460,145m) and Precision Machinery & Robot (¥279,925m), with smaller contributions from Rolling Stock (¥236,291m) and Others (¥116,345m).

Market Cap: ¥2.27t

Kawasaki Heavy Industries gives you exposure to several long term themes in one stock, with hydrogen infrastructure, energy solutions, robotics and aerospace all contributing to earnings that grew 22.9% in the last year and a profit margin of 4.7% that is moving in the right direction. The company is also working to build more recurring, service based revenue in areas such as rolling stock. It is tightening its balance sheet after deleveraging, even as debt coverage and reliance on external funding remain key risks to watch. With analysts expecting steady revenue growth, improving margins and a P/E that sits between the wider machinery sector and some higher priced peers, the central question is how much of Kawasaki’s restructuring and efficiency potential is already reflected in the current share price.

Kawasaki Heavy Industries has earnings growing and margins moving in the right direction, but the real story could be how its restructuring and funding risks interact in the 4 key rewards and 2 important warning signs (1 is major!)

The three stocks covered here are only a starting point, as the full Industrial Restructuring and Operational Efficiency screener surfaced 9 more companies that are also leaning into cost controls, workforce reshaping, or production changes in different ways in the Industrial Restructuring and Operational Efficiency screener. Use Simply Wall St to identify and analyze the specific catalysts, restructuring narratives, and financial traits that match your own highest conviction ideas so you can focus on the opportunities that fit your approach.

Take Control of Your Investment Journey

If ATS or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh breakouts and quiet momentum rarely stay under the radar for long. The best entry points can be captured early, so review these focused stock lists and consider your options promptly.

- Spot potential turnaround stories early by scanning companies with resilient balance sheets in the list of solid balance sheet and fundamentals (12 results) that can keep funding operations if conditions get tougher.

- Follow the AI infrastructure build out by tracking the 52 AI infrastructure stocks where demand for data centers, chips, and supporting equipment may be influencing the next wave of momentum.

- Focus on companies already generating cash from AI by reviewing the 63 profitable AI stocks that aren't just burning cash so you concentrate on businesses with existing earnings rather than ideas that might not scale.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com