- Tutor Perini Corporation recently completed the redemption of US$400 million of 11.875% Senior Notes due 2029, funded with proceeds from a new US$400 million 6.625% Senior Notes issue due 2033 and cash on hand, while also overhauling and extending its revolving credit facility to July 2, 2031.

- This refinancing meaningfully reduces borrowing costs, increases committed revolving capacity to US$350.0 million, and resets leverage and interest coverage covenants, potentially enhancing the company’s financial flexibility for its large project backlog.

- We’ll now examine how the lower-cost 2033 notes and expanded revolving credit facility reshape Tutor Perini’s existing investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Tutor Perini Investment Narrative Recap

To own Tutor Perini, you need to believe the company can convert its large public project backlog into durable profits while keeping execution and legal risks contained. The recent refinancing looks supportive for that near term catalyst by lowering interest costs and expanding liquidity, but it does not remove core risks around mega project performance, potential cost overruns, or exposure to government funding decisions.

Among recent developments, the award of the NAVFAC Pacific P 1181 Harden Critical Feeders project in Guam stands out, reinforcing how dependent Tutor Perini is on large public sector work. This ties directly into both the upside case around backlog conversion and the key risk that delays, budget changes, or regulatory shifts on a few big contracts could quickly affect earnings, despite the stronger balance sheet signaled by the July refinancing.

Yet investors should also be aware that if project execution stumbles or government funding priorities shift, especially given the concentration in large civil and defense contracts...

Read the full narrative on Tutor Perini (it's free!)

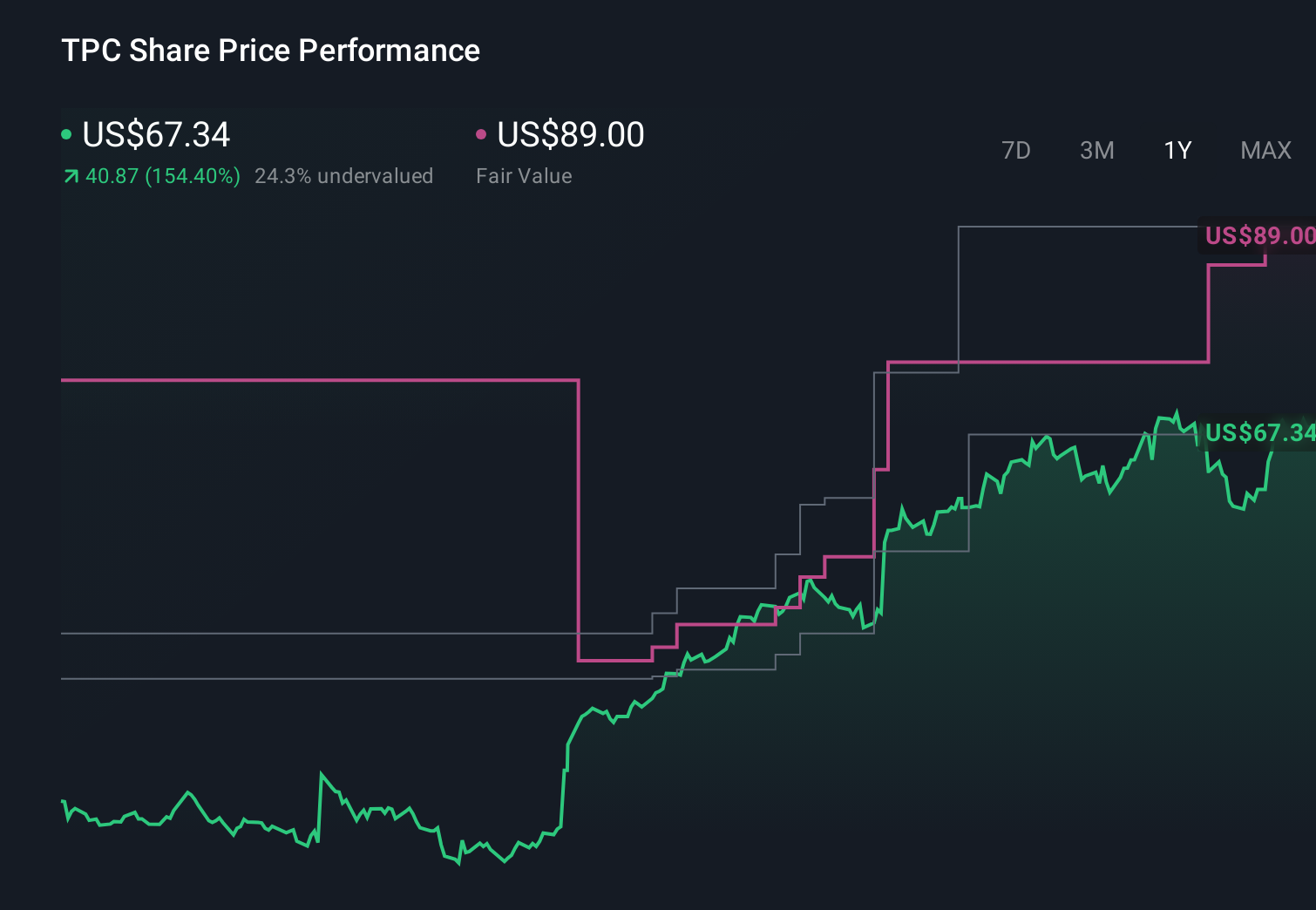

Tutor Perini's narrative projects $7.6 billion revenue and $483.9 million earnings by 2029. This requires 10.2% yearly revenue growth and about a $405.8 million earnings increase from $78.1 million.

Uncover how Tutor Perini's forecasts yield a $113.25 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already more cautious, assuming revenue of about US$7.9 billion and earnings near US$300 million by 2029, and they focus more on how labor shortages and higher technology costs could squeeze margins even with this week’s refinancing in place.

Explore 5 other fair value estimates on Tutor Perini - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Tutor Perini research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Tutor Perini research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tutor Perini's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com