Penny stocks often carry a reputation for high risk, but the Financially Fit Penny Stocks screener focuses on a narrower corner of this market: companies trading below 5 with an emphasis on financial health. With investors watching inflation, interest rates, and energy prices closely, many are looking for smaller businesses that are not just cheap, but fundamentally sound. This screener is designed to highlight those stocks, aiming to filter out weaker balance sheets. In this article, you will see 3 candidates from the screener that may deserve a closer look for a diversified, higher-risk portion of your portfolio.

Swasti Vinayaka Art and Heritage (BSE:512257)

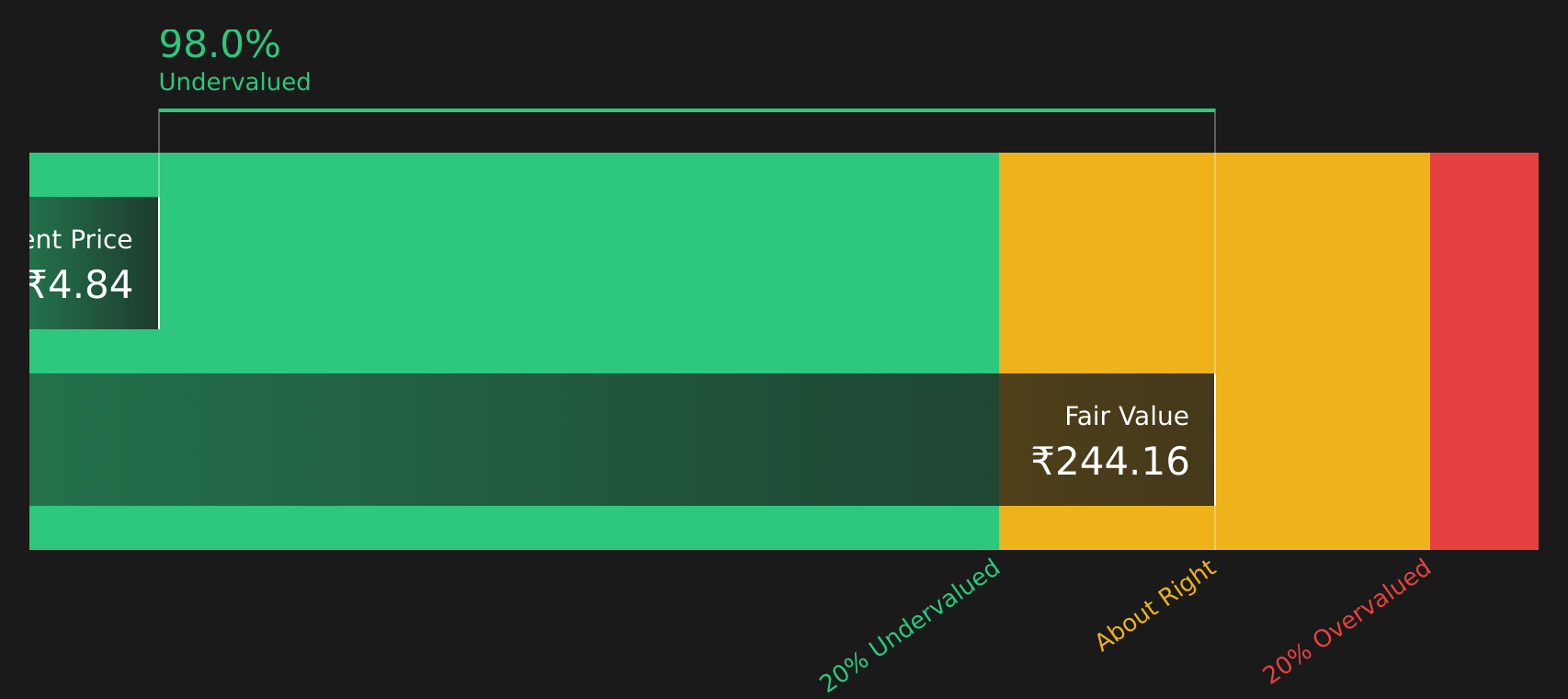

Overview: Swasti Vinayaka Art and Heritage Corporation manufactures and sells carvings in precious and semi precious stones, paintings and jewelry in India, while also participating in real estate activities. The company has been operating since 1985 and is based in Mumbai.

Market Cap: ₹320.4 million

Swasti Vinayaka Art and Heritage stands out in the penny stock space because its low share price sits alongside a very large gap to one cash flow based fair value estimate, a low P/E of 5.5x relative to luxury peers, and an 18.3% net profit margin. Revenue of ₹330.7 million and net income of ₹58.08 million for FY2026, with earnings growth that has exceeded its own 5 year average, point to improving fundamentals. At the same time, all liabilities come from higher risk external borrowing and the business still operates off a relatively small revenue base, while the stock has lagged the broader Indian market. For investors, the mix of valuation discount, earnings strength and funding risk makes Swasti Vinayaka a company worth closer inspection.

Swasti Vinayaka Art and Heritage looks like a valuation story hiding in plain sight, with a low P/E and healthy margins raising more questions than answers around what the DCF valuation analysis for Swasti Vinayaka Art and Heritage might reveal about the real risk here

Elegant Floriculture & Agrotech (India) (BSE:526473)

Overview: Elegant Floriculture & Agrotech (India) produces and exports cut flowers and indoor plants ranging from Dutch roses and Gerbera to orchids and foliage varieties, supplying both domestic buyers and overseas customers from its base in Gandhinagar.

Operations: Elegant Floriculture & Agrotech (India) generates revenue of approximately ₹1,600.3 million from its Floriculture and Agri Products segment.

Market Cap: ₹96 million

Elegant Floriculture & Agrotech (India) sits in an unusual spot for a penny stock, combining very low pricing relative to one cash flow based fair value estimate with rapid earnings growth and a P/E multiple that is well below many Indian food peers. At the same time, profit margins have swung sharply, recent quarterly results included a small loss, and all liabilities currently rely on higher risk external borrowing. As a result, funding and earnings quality need careful attention. A largely new board and management team add another layer of uncertainty. For investors willing to research further, the mix of apparent valuation gap, expanding full year revenue and evolving governance makes Elegant Floriculture & Agrotech (India) a company that may merit deeper analysis.

Elegant Floriculture & Agrotech (India) looks like an earnings story that the market has not fully priced, with a low P/E and volatile margins raising important questions answered in the analysis report for Elegant Floriculture & Agrotech (India)

Shangar Décor (BSE:540259)

Overview: Shangar Décor Limited provides event decoration, planning and catering services in India, covering pre wedding functions, themed weddings, corporate and religious events, property decor and lighting, with operations based in Ahmedabad since 1995.

Operations: Shangar Décor generates approximately ₹232.6 million in revenue from its Event Management business in India.

Market Cap: ₹117.5 million

Shangar Décor catches the eye in this penny stock screener because strong recent earnings growth of 82.3% and a low P/E of 8x sit alongside a modest revenue base of around ₹233 million, a 6.3% net margin and low 2.5% return on equity. The stock has lagged both the wider Indian market and Consumer Services sector, and the share price has been volatile, while all liabilities currently rely on higher risk external borrowing. On the other hand, there are indications of higher quality earnings and a recent refresh of independent directors. Investors doing deeper work may find an events business where the balance between value, funding risk and governance is not immediately obvious from the headline numbers.

Shangar Décor’s earnings surge and low P/E suggest the stock may be quietly decoupling from its modest 6.3% margin and 2.5% ROE, and the 2 key rewards and 2 important warning signs could reveal what that contrast is really signaling

The three financially fit penny stocks in this article are just a starting point, with the full Financially Fit Penny Stocks screener surfacing 113 more companies that pair low share prices with balance sheets and earnings profiles that may support equally compelling stories. Use Simply Wall St to identify, filter and analyze the specific catalysts, funding risks and valuation narratives that matter to you so you can focus on the highest conviction opportunities in this part of the market.

Take Control of Your Investment Journey

If Elegant Floriculture & Agrotech (India) or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Penny Stocks

Some of the most interesting breakout stories start quietly, then momentum builds and prices are flying before most notice. Scan these fresh ideas under the radar for now and review them carefully.

- Consider aiming for steadier income potential by reviewing 468 dividend fortresses that focus on durable cash flows and balance sheets while yields are still compelling and before wider attention tightens entry points.

- Explore structural shifts in computing by checking 26 quantum computing stocks featuring companies positioned around quantum hardware, software and infrastructure while many investors are still looking the other way.

- Evaluate long term infrastructure demand by scanning 34 power grid technology and infrastructure stocks built around businesses tied to grid upgrades, network reliability and transmission capacity before momentum fully catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com