The renewal of Baytex Energy (TSX:BTE) normal course issuer bid, which allows repurchases of up to 70.9 million shares over the next year, has put fresh attention on what this buyback might mean for existing shareholders.

See our latest analysis for Baytex Energy.

At a share price of CA$5.97, Baytex Energy has seen a 31.5% year to date share price return, while its 1 year total shareholder return of 135.12% points to strong momentum despite a 1 month share price decline of 7.73%.

If you are looking beyond Baytex Energy for other opportunities in the energy space, this could be a good moment to check out 89 nuclear energy infrastructure stocks

With Baytex Energy up 31.5% year to date and a renewed buyback in place, the stock already reflects a lot of optimism. The real issue now is whether the current price still offers an attractive risk reward as you look at valuation.

Most Popular Narrative: 21.1% Undervalued

Against Baytex Energy's last close of CA$5.97, the most followed narrative pegs fair value near CA$7.57, framing the renewed buyback within a broader earnings and cash flow story.

Baytex Energy's continuous improvement in drilling and completion efficiencies, particularly in the Eagle Ford and Pembina Duvernay plays, is expected to lead to improved capital costs and better production performance, which will likely impact revenue and net margins positively. The ongoing replacement of over 100% of production on both 1P and 2P reserve bases suggests sustainable reserve growth, which supports future production levels and could result in increased revenue and long-term company valuation.

Want to see what is behind that fair value gap for Baytex Energy? The narrative leans on a sharp swing in profitability and a future earnings multiple that is far from generous. Curious which revenue path and cash flow assumptions need to line up for that story to hold?

Result: Fair Value of CA$7.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story of Baytex Energy could change quickly if oil prices remain near US$60 or lower for an extended period, or if U.S. tariffs on Canadian energy tighten.

Find out about the key risks to this Baytex Energy narrative.

Another View on Baytex Energy's Valuation

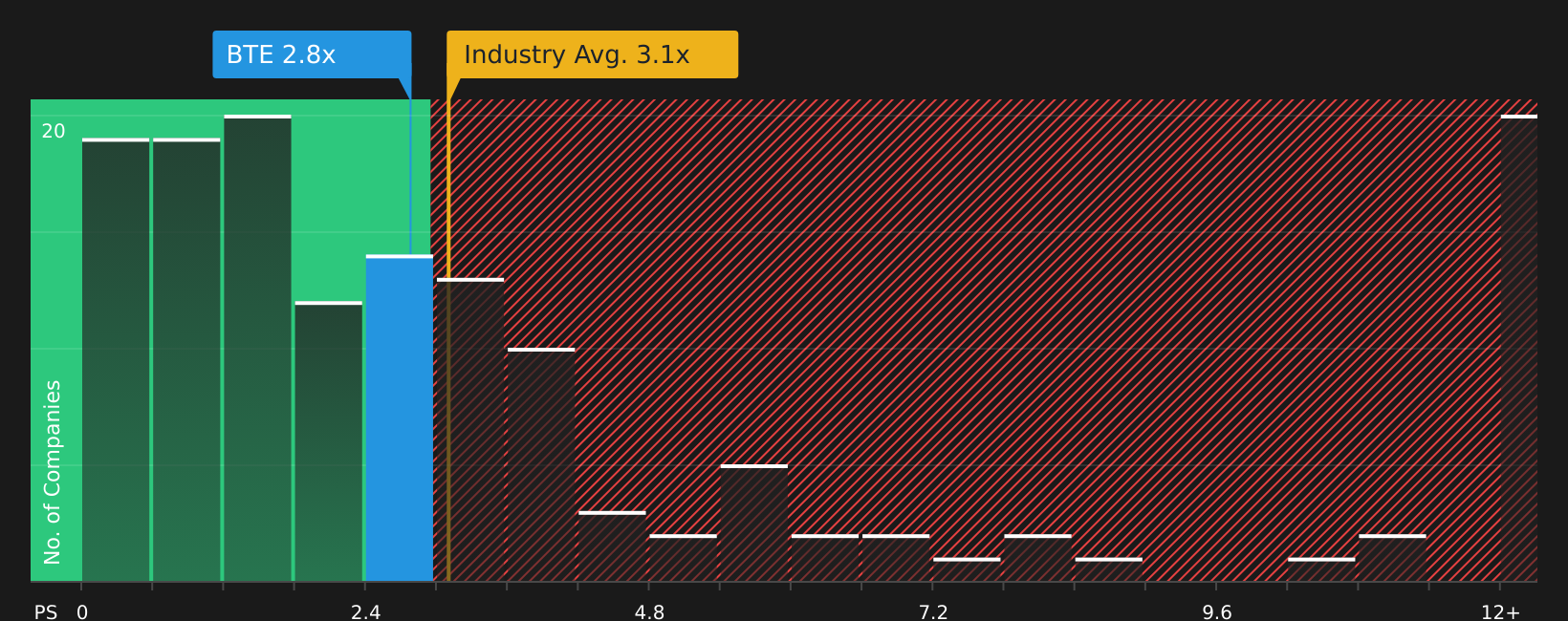

The fair value narrative for Baytex Energy leans heavily on future earnings and cash flow, but the current P/S ratio tells a more mixed story. The stock trades at 2.9x sales, above a fair ratio estimate of 2.1x, yet still below peers at 6.7x. That gap suggests investors need to think carefully about whether they see more valuation risk or opportunity from here.

To see how those sales based signals stack up against cash flow assumptions, it is worth lining this up with the SWS DCF model. That model also points to Baytex Energy trading below an estimated future cash flow value of CA$7.31 per share. The key question for investors is which set of assumptions they trust more over time.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Baytex Energy's story mixing optimism and caution, this is a good moment to move fast, review the key data, and shape your own view using the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Baytex Energy?

If Baytex Energy has sharpened your focus on where to put fresh capital, do not stop here. Broaden your watchlist with other focused stock ideas using the Simply Wall Street Screener.

- Target steady compounding potential by checking companies with consistent payouts and high yields through the 6 dividend fortresses.

- Hunt for quality at a sensible price by using the 5 high quality undervalued stocks to spot stocks where fundamentals and valuation still appear out of sync.

- Prioritize sleep at night holdings by scanning the 10 resilient stocks with low risk scores for businesses that pair resilience scores with cleaner balance sheet profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com