With inflation worries linked to higher energy costs, shifting rate expectations across the US, Europe, and Asia, and bond yields staying elevated, many investors are looking for more predictable income from their portfolios. Consistent dividends can help, especially when those payouts are both substantial and well covered. The Dividend Powerhouses screener focuses on companies offering more than a 5% yield, with payments that appear stable and growing. This article highlights three stocks from that screener that stand out for income focused investors who want to put reliable cash flows at the center of their long term plan.

Lloyds Banking Group (LSE:LLOY)

Overview: Lloyds Banking Group is a large UK based financial institution that provides everyday banking, lending, and credit services to individuals, alongside lending, payments, and risk management solutions for businesses, as well as insurance, pensions, and investment products under brands such as Lloyds Bank, Halifax, Bank of Scotland, and Scottish Widows.

Market Cap: £64.17b

Income focused investors may find Lloyds Banking Group interesting because it combines a high dividend yield focus with efforts to reshape how it earns money, including buybacks, AI driven cost efficiencies and a push into fee based areas such as pensions and wealth. Earnings growth has recently outpaced the wider UK banks industry and net profit margins of 24.1% suggest solid profitability, yet the P/E ratio sits above sector averages, which raises questions about how much optimism is already reflected in the price. At the same time, Lloyds is tightly tied to the UK economy and faces fierce digital competition, as well as regulatory and conduct risks that could affect capital returns if conditions turn.

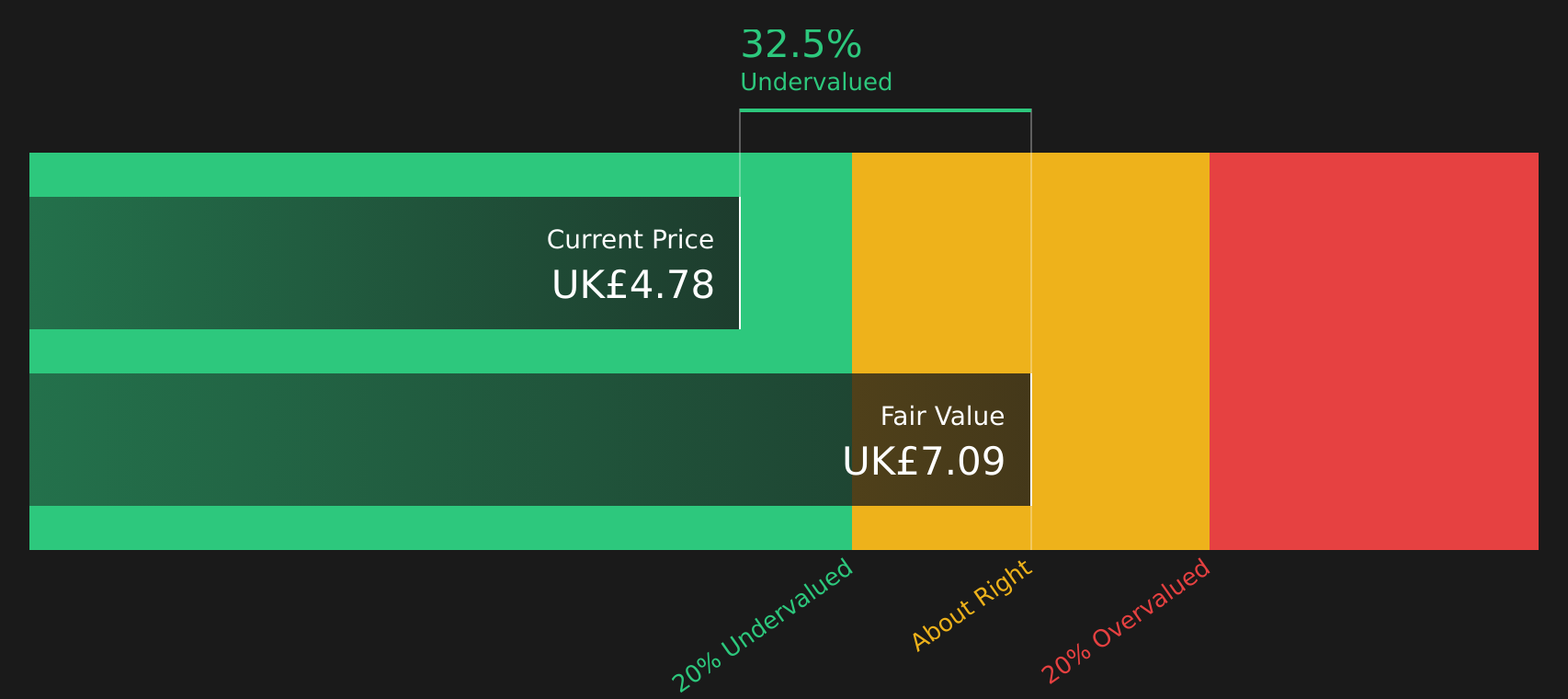

Lloyds Banking Group’s rich yield and premium P/E suggest investors are betting on more than just cost cuts and buybacks, so it is worth seeing how the valuation stacks up in the DCF valuation analysis for Lloyds Banking Group

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity and listed funds, with a focus on renewable energy projects, social and digital infrastructure, and backing smaller growth companies across the UK, Europe and Australia for both institutional and retail investors.

Operations: Foresight Group Holdings generates most of its revenue from Real Assets at £114.8m, with Private Equity contributing £50.1m, and the United Kingdom providing the bulk of its £126.4m geographic revenue alongside smaller contributions from Australia at £25.7m and several European markets.

Market Cap: £506.4m

Income investors looking beyond traditional banks may find Foresight Group Holdings appealing because its infrastructure and private equity focus is tied to long term themes such as energy transition and social infrastructure. Current earnings quality and return on equity metrics are described as strong. The stock is trading below some fair value estimates and analyst targets, with buybacks steadily shrinking the free float. However, the business still relies heavily on variable performance fees and borrowings rather than customer deposits. When combined with rising administrative costs and exposure to UK and European policy and regulatory shifts, this creates a higher risk, higher reward profile that might be of interest if you are seeking yield plus growth potential from a specialist asset manager.

Foresight Group Holdings sits at the crossroads of yield, energy transition and infrastructure. Yet the real story may be how its current price, buybacks and earnings quality line up in the analysis report for Foresight Group Holdings

3i Group (LSE:III)

Overview: 3i Group is a London based private equity and infrastructure investor that buys stakes in mature, often market leading businesses and infrastructure assets, then works with management to improve operations and eventually realise gains for its own shareholders.

Operations: 3i Group generates the majority of its revenue from Private Equity at about £5.3b, with additional contributions from Infrastructure at £193m, the Scandlines ferry business at £55m, and £32m of unallocated IFRS adjustments.

Market Cap: £27.0b

Income investors may want to pay attention to 3i Group because it combines a 3.15% dividend with exposure to a portfolio that includes high margin private equity holdings, the fast growing Action discount retailer and infrastructure assets, while trading at a large discount to some fair value estimates. Recent net income of £5,294m, high net profit margins and a sizeable buyback programme point to strong cash generation and an intent to return capital. At the same time, reliance on external borrowing, currency swings and sector specific weakness in areas like automotive and North American recruitment introduce real risk. The key question is whether that risk profile, together with evolving margins and ROE, justifies the sizable valuation gap investors see today.

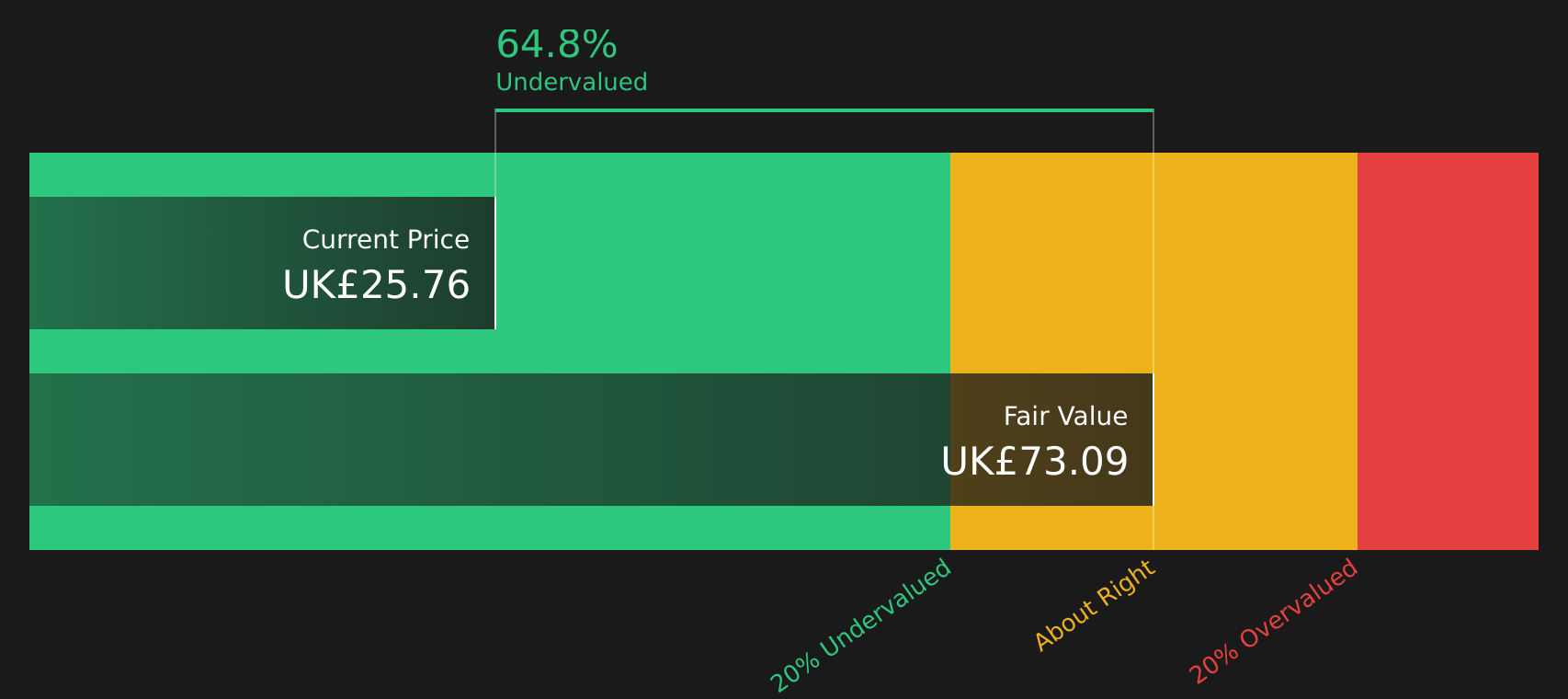

3i Group’s substantial valuation gap and high-margin portfolio raise a clear question: is the market misreading this story or seeing something others are missing in the analysis report for 3i Group?

The three dividend stocks covered here are only a starting point, with the full Dividend Powerhouses screen surfacing 43 more companies that pair yields above 5% with stories that could be just as compelling as anything you have seen so far in the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to unlock that full set of ideas, then identify and analyze companies by the exact catalysts and narratives that matter to you so you can focus on the highest conviction dividend opportunities.

Take Control of Your Investment Journey

If Lloyds Banking Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do?

Fresh ideas move fast, and the stocks leading the next breakout can be hard to catch once momentum builds. Scan these focused shortlists before the crowd and consider your options promptly.

- Spot under the radar quality companies trading at appealing valuations by sweeping through a curated pool of 10 high quality undervalued stocks while that pricing gap still matters.

- Follow the structural shift toward next generation data centers and hardware by tracking hand picked infrastructure leaders in the 52 AI infrastructure stocks before attention broadens.

- Review carefully filtered producers in the 8 top copper producer stocks while sentiment is still catching up to the story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com