Amid ongoing geopolitical tensions and energy market volatility, Asian markets have shown mixed performance, with some indices facing downward pressure due to external factors such as higher oil prices. In this environment, identifying undervalued stocks can be crucial for investors looking to capitalize on potential growth opportunities. A good stock in these conditions may be one that is trading below its intrinsic value estimates, offering a potential margin of safety while benefiting from strong fundamentals and resilience against broader market fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zhongji Innolight (SZSE:300308) | CN¥1184.05 | CN¥2344.19 | 49.5% |

| Samsung Electro-Mechanics (KOSE:A009150) | ₩1260000.00 | ₩2496659.82 | 49.5% |

| Rakuten Bank (TSE:5838) | ¥5800.00 | ¥11510.04 | 49.6% |

| Matrix Design (SZSE:301365) | CN¥37.02 | CN¥72.74 | 49.1% |

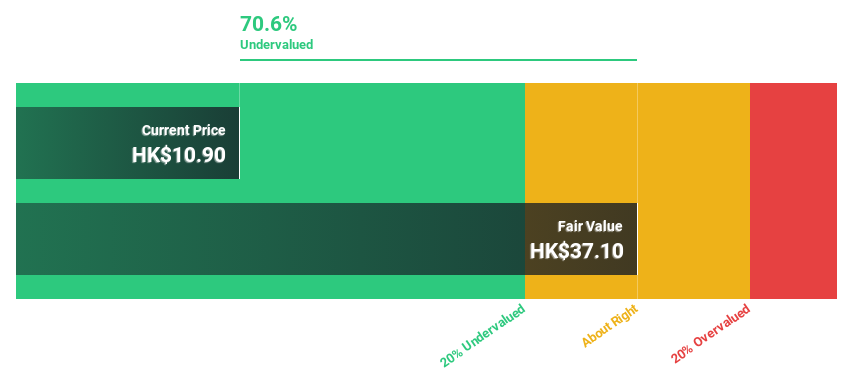

| Laopu Gold (SEHK:6181) | HK$373.80 | HK$746.45 | 49.9% |

| Hanwha Engine (KOSE:A082740) | ₩43500.00 | ₩86226.60 | 49.6% |

| GreenEnergy (TSE:1436) | ¥1374.00 | ¥2699.11 | 49.1% |

| CSPC Innovation Pharmaceutical (SZSE:300765) | CN¥37.39 | CN¥74.24 | 49.6% |

| BEAUTY GARAGE (TSE:3180) | ¥1453.00 | ¥2876.45 | 49.5% |

| Addvalue Technologies (SGX:A31) | SGD0.133 | SGD0.26 | 49% |

Let's take a closer look at a couple of our picks from the screened companies.

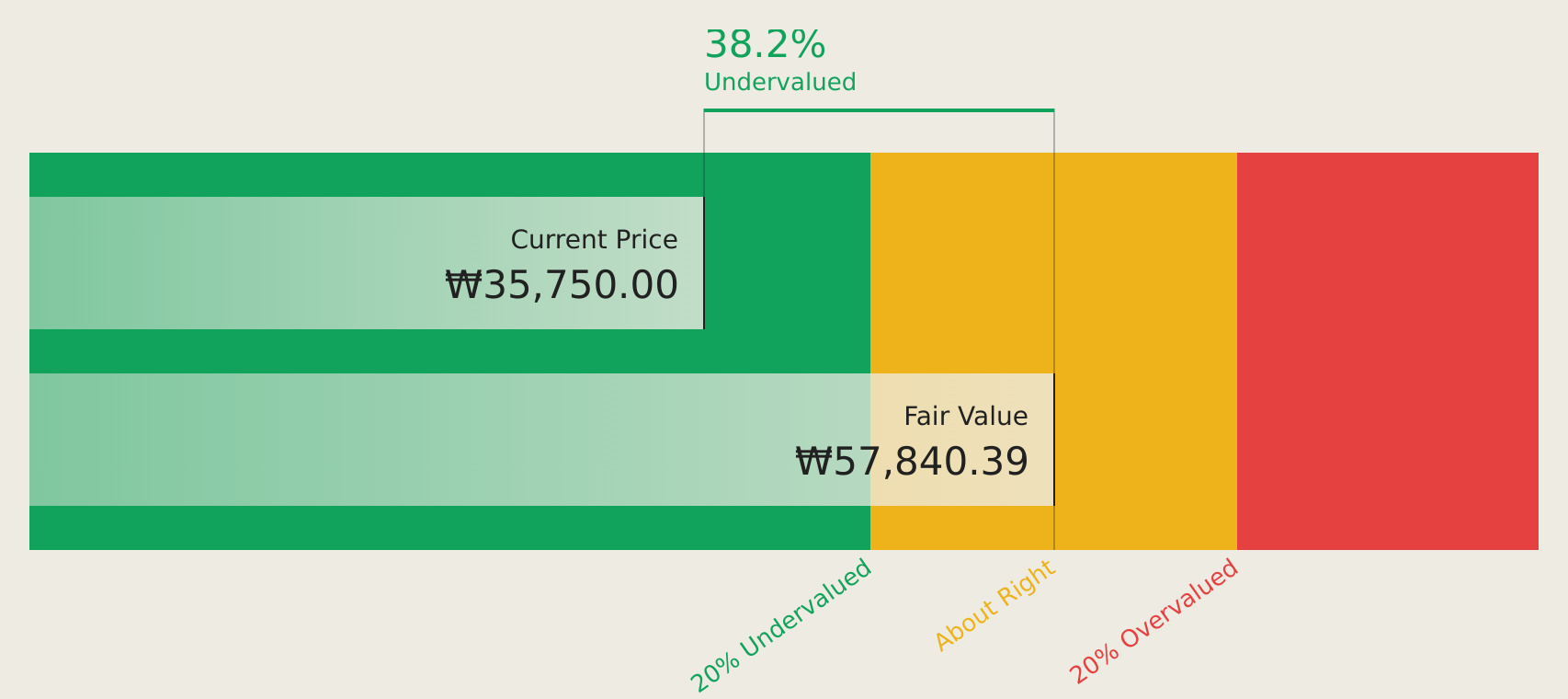

HANA Micron (KOSDAQ:A067310)

Overview: HANA Micron Inc. offers semiconductor back-end process packaging solutions in South Korea and has a market cap of approximately ₩2.29 trillion.

Operations: The company's revenue is primarily derived from Semiconductor Manufacturing at ₩2.64 trillion, followed by Semiconductor Material at ₩307.05 million, and New Technology Business financing at ₩1.23 million.

Estimated Discount To Fair Value: 33.9%

HANA Micron, currently trading at ₩38,250, is undervalued based on discounted cash flow analysis with an estimated future value of ₩57,840.39. Despite a volatile share price recently, its revenue is expected to grow 24% annually—outpacing the Korean market's 16.1%. However, earnings growth at 28.6% lags behind the market's 32%, and interest payments are not well covered by earnings despite recent profitability improvements.

- The growth report we've compiled suggests that HANA Micron's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of HANA Micron.

Kingdee International Software Group (SEHK:268)

Overview: Kingdee International Software Group Company Limited is an investment holding company that focuses on the subscription and sale of software globally, with a market cap of HK$23.75 billion.

Operations: The company's revenue segments include CN¥4.23 billion from subscription and software sales, and CN¥2.78 billion from implementation, consulting, and maintenance services.

Estimated Discount To Fair Value: 35.5%

Kingdee International Software Group is trading at HK$6.76, significantly below its estimated future cash flow value of HK$10.48, highlighting potential undervaluation. The company's earnings are forecast to grow 31.3% annually, outpacing the Hong Kong market's 12.5%. However, revenue growth at 11.5% per year lags behind a high benchmark of 20%, and future return on equity is projected to be modest at 10.4%. Recent bylaw changes were approved in May 2026.

- The analysis detailed in our Kingdee International Software Group growth report hints at robust future financial performance.

- Take a closer look at Kingdee International Software Group's balance sheet health here in our report.

Shanghai Liangxin ElectricalLTD (SZSE:002706)

Overview: Shanghai Liangxin Electrical Co., LTD. manufactures and sells low-voltage electrical appliances both in China and internationally, with a market cap of CN¥11.23 billion.

Operations: Shanghai Liangxin Electrical Co., LTD. generates its revenue by producing and distributing low-voltage electrical appliances across domestic and international markets.

Estimated Discount To Fair Value: 14.5%

Shanghai Liangxin Electrical Co., LTD. is trading at CN¥10.22, slightly below its estimated future cash flow value of CN¥11.95, indicating potential undervaluation based on cash flows. Despite a decline in net income to CNY 56.5 million from CNY 103.14 million year-on-year, earnings are forecast to grow significantly at 39% annually, surpassing the Chinese market's average growth rate of 27%. However, profit margins have decreased from last year's figures and share price volatility remains high.

- Insights from our recent growth report point to a promising forecast for Shanghai Liangxin ElectricalLTD's business outlook.

- Unlock comprehensive insights into our analysis of Shanghai Liangxin ElectricalLTD stock in this financial health report.

Make It Happen

- Dive into all 199 of the Undervalued Asian Stocks Based On Cash Flows we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com