- Enterprise Products Partners L.P. recently declared a second-quarter 2026 cash distribution of US$0.56 per unit (US$2.24 annualized), a 2.8% increase over the prior-year quarter, payable on August 14, 2026 to unitholders of record on July 31, 2026.

- The announcement extends Enterprise Products Partners’ long-running pattern of distribution growth, reinforcing its appeal for income-focused investors who prioritize consistent cash payouts.

- We’ll now examine how this latest distribution increase may influence Enterprise Products Partners’ investment narrative, especially around its income-generating profile.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Enterprise Products Partners Investment Narrative Recap

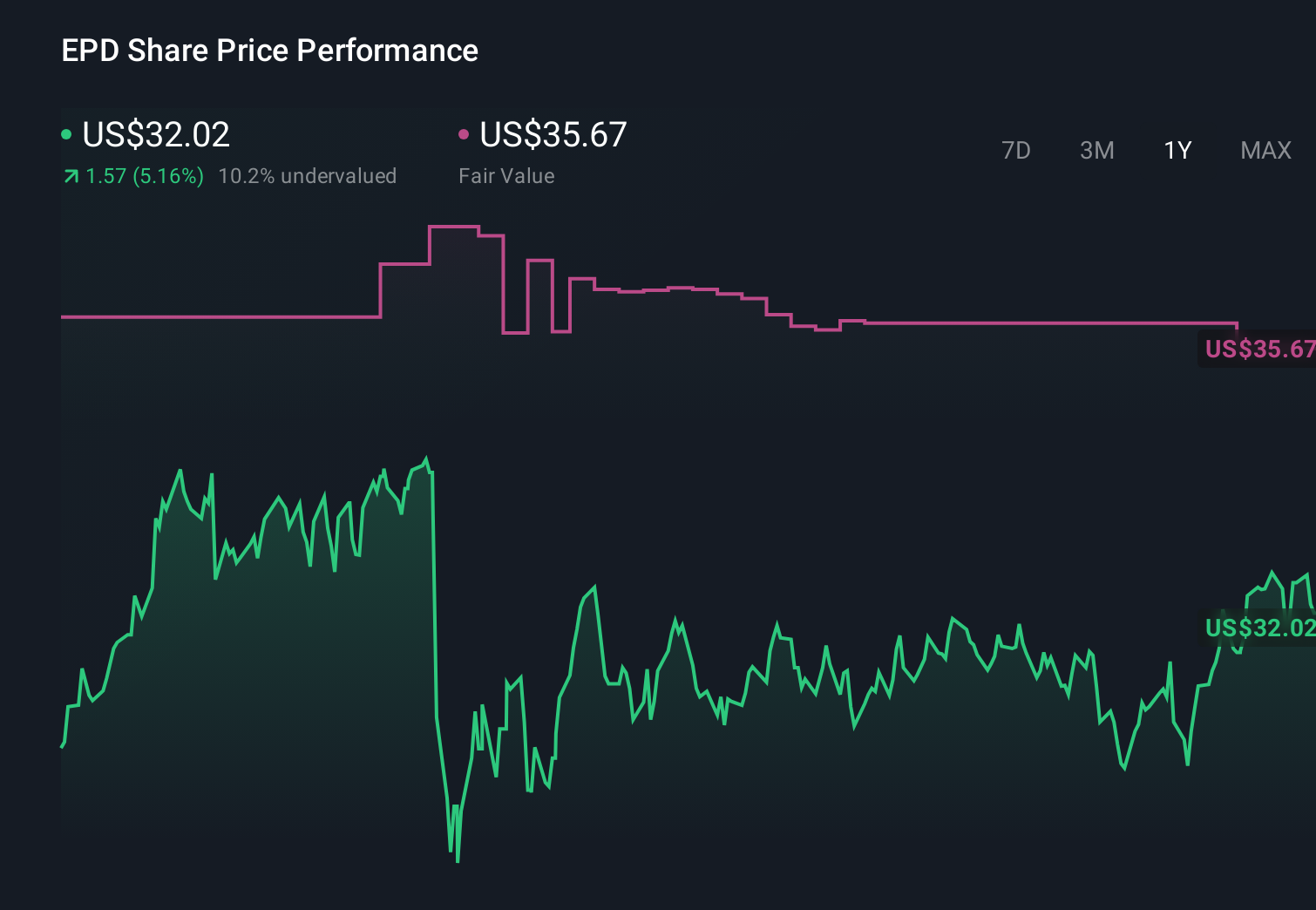

To own Enterprise Products Partners, you need to be comfortable with a midstream business that prioritizes steady cash distributions supported by large-scale infrastructure projects and long-term energy demand. The latest 2.8% distribution increase reinforces its income appeal but does not materially change the key near term story, which still centers on executing capacity expansions while managing a sizeable debt load and exposure to tariff and commodity driven volume risks.

The recent announcement of Jim Teague’s planned retirement and Randy Fowler’s transition to sole CEO is particularly relevant alongside the new distribution increase. For income focused investors, Fowler’s long tenure across finance, capital projects and executive roles may help support continuity as Enterprise works through its pipeline, processing and export growth projects that underpin future cash flow, while still leaving operational issues like prior PDH downtime as an area to watch.

Yet against this stable distribution growth, investors should be aware of how Enterprise’s sizeable debt and interest rate sensitivity could...

Read the full narrative on Enterprise Products Partners (it's free!)

Enterprise Products Partners' narrative projects $61.3 billion revenue and $7.5 billion earnings by 2029. This requires 5.9% yearly revenue growth and a $1.7 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $41.25 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community span roughly US$35 to US$96 per unit, highlighting very different expectations for Enterprise’s potential. When you weigh those views against the ongoing build out of gas processing plants, pipelines and export capacity, it underlines how much your own outlook on future volumes and tariffs may shape your view of the partnership’s longer term performance.

Explore 5 other fair value estimates on Enterprise Products Partners - why the stock might be worth 7% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

No Opportunity In Enterprise Products Partners?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com