United Parcel Service stock has delivered a 32.9% decline over the past five years. However, current valuation checks and an intrinsic value estimate based on a Discounted Cash Flow (DCF) approach both indicate the shares may now sit at a discount to what the underlying cash flows suggest.

- Over the last five years, United Parcel Service stock is down 32.9%, which frames any current discount as a potential reset rather than a recent surge.

- UPS’s focus on higher margin, end to end logistics solutions can support earnings quality. At the same time, the call from the USPS Inspector General to reassess a major air cargo contract highlights a revenue and volume risk that could affect how durable those cash flows are.

- Across Simply Wall St’s broader checks, United Parcel Service scores 4 out of 6 on value, which points to a mixed picture rather than a simple cheap or expensive label.

The issue now is whether United Parcel Service’s current share price already reflects these contract and margin pressures, or if the discount implied by the intrinsic value estimate still offers room for upside.

Find out why United Parcel Service's 22.1% return over the last year is lagging behind its peers.

Is United Parcel Service Still Cheap on Cash Flow?

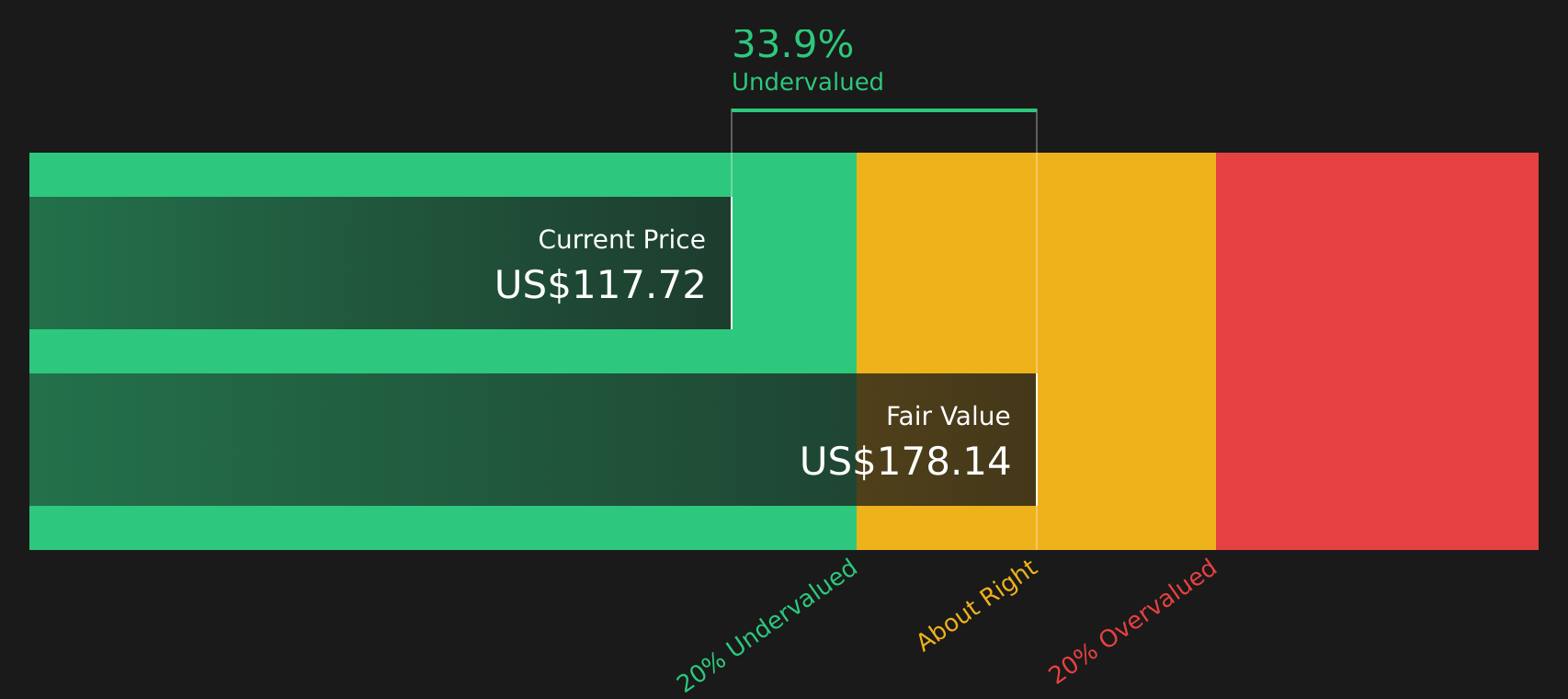

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what United Parcel Service might be worth today. On this model, United Parcel Service generated about $4.0b of free cash flow over the last twelve months, with projections assuming recovering, growing cash flows rather than aggressive expansion or sharp decline.

Those projections translate into an estimated intrinsic value of about $177.84 per share, which is roughly 36.1% above the current share price, so the stock screens as undervalued on this basis. The USPS Inspector General’s push to reconsider the large air cargo contract helps explain why the market is hesitant, even though the cash flow profile in the DCF still points to more value than the price reflects.

Overall, the DCF workup suggests United Parcel Service stock currently looks undervalued relative to the cash flows analysts expect it to generate.

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 36.1%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does United Parcel Service Look Undervalued on Earnings?

The P/E ratio is a useful yardstick for United Parcel Service because earnings still sit at the center of how investors assess large, mature logistics groups. United Parcel Service currently trades on a P/E of about 18.4x, compared with an industry average of roughly 15.3x and a peer average near 24.4x, so the stock sits between the broader sector and closer peers.

Simply Wall St’s model suggests a fair P/E of about 25.4x for United Parcel Service given its mix of margins, scale and risk. This is meaningfully higher than the current 18.4x. That gap indicates the market is pricing the stock below what this framework implies, even after factoring in the USPS contract uncertainty and the focus on higher margin, end to end logistics solutions.

On this earnings multiple, United Parcel Service stock appears undervalued relative to what the fair P/E suggests investors might be willing to pay.

See what the numbers say about this price — find out in our valuation breakdown.

The United Parcel Service Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for United Parcel Service give you a clearer link between the apparent valuation discount and the assumptions that would need to hold on United Parcel Service's growth, margins and earnings for the stock to be worth materially more or less than today’s price, using structured scenarios on the Community page. Each one sets out fair value as a thesis about how the business might perform over time, so you can monitor how that view holds up as new information emerges.

Community views on United Parcel Service sit far apart, with one camp leaning into the transformation story and another focused on execution and balance sheet strain.

Bull case: 16% undervalued

"The company's expanding healthcare logistics business, including cold chain, pharma, and SMB healthcare, has an $82 billion addressable market. With the pending Andlauer acquisition, best-in-class service levels, and differentiated tech capabilities, UPS is poised to accelerate high-margin, recurring revenue streams that can support long-term earnings stability and growth.…"

Read the full Bull Case to see why United Parcel Service could be undervalued

Bear case: 19% overvalued

"These pressures, combined with declining revenue and earnings per share across recent quarters, suggest that profitability will continue to struggle.…"

Read the full Bear Case to see why United Parcel Service could be overvalued

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

The Bottom Line

For United Parcel Service, both the Discounted Cash Flow (DCF) work and the P/E based view point to the stock looking undervalued rather than expensive, even if the broader checks are only mixed. The crux is whether the cash flows implied by the intrinsic value estimate and fair P/E can hold up against risks around the USPS air contract and margin execution. From here, what matters most is whether UPS converts its higher margin logistics focus into stable, repeatable earnings that justify a higher multiple, rather than the current discount turning into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com