The Zhitong Finance App learned that Qunzhi Consulting published an article stating that global smartphone shipments in the second quarter of 2026 were about 250 million units, a year-on-year decrease of 9.7%. In the second quarter of 2026, China's smartphone shipments were about 63.1 million units, a year-on-year decrease of 7%. Based on current supply-side cost pressure and continued weakness on the demand side, global smartphone shipments are expected to be around 1.06 billion units in 2026, a year-on-year decline of 11.3%. Of these, China shipped about 240 million units, a year-on-year decline of 13.8%.

I. Global smartphone market

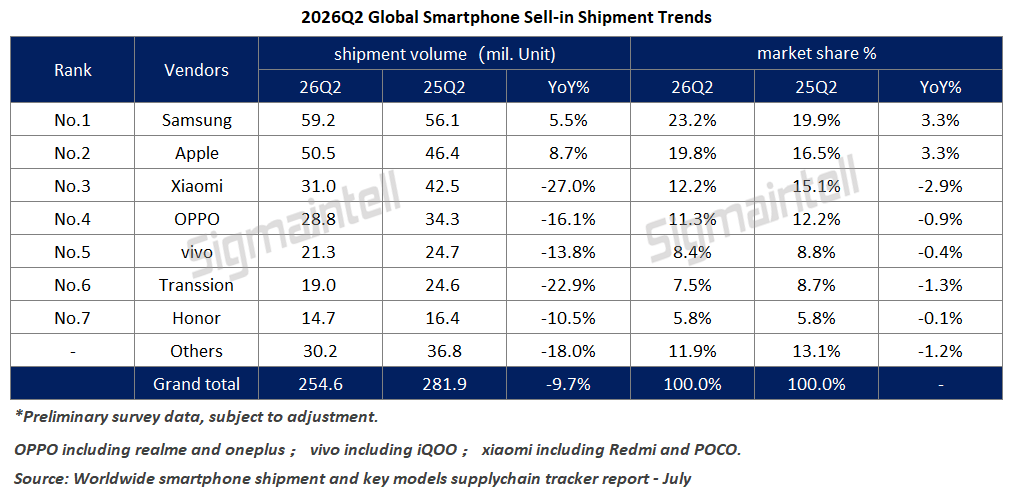

According to data from Sigmaintell (Sigmaintell), global smartphone shipments in the second quarter of 2026 were about 250 million units, a year-on-year decrease of 9.7%.

(1) The head gap is gradually widening, and the trend of Samsung/Apple siphoning domestic brands is getting worse. Samsung and Apple achieved contrarian growth, with growth of 5.5% and 8.7% respectively.

Samsung's growth is mainly due to the contribution of its low-end 4G products. Domestic mobile phones were forced to raise product prices due to cost pressure, while Samsung entry-level products (such as the Galaxy A07 4G) still maintained price competitiveness, further highlighted the cost performance ratio and increased the demand for entry-level products; the high-end market stimulated high-end demand with the Galaxy S26 Ultra active security screen and AI features, which stimulated high-end demand, and the high and low end together promoted growth in the second quarter.

Apple's second-quarter growth was mainly due to the iPhone 17 series. Its strong product competitiveness and stable price system were the main reasons that stimulated demand, #群智咨询(Sigmaintell)数据显示,iPhone17系列在2026年第一季度和第二季度的备货较去年同期(iPhone16系列)分别增长了52% and 84%.

(2) Due to the rise in memory supply costs, domestic brands have seriously shrunk in their scale of decline, which is the main reason for the year-on-year decline in domestic brands. Among them, Transmission has the largest distribution of ultra-low-end tiers in the global market, and its ability to withstand price increases is relatively weak when rising costs are forced to raise prices (low-income groups are more sensitive to price increases), so the year-on-year decline was also the most serious, with a decrease of 22.9%. Brands such as OPPO and vivo also optimized their product layout, adjusted production strategies, streamlined product quantities, and raised product prices due to rising cost pressures, etc., and the global market also declined by 16.1% and 13.8%, respectively.

II. China's smartphone market

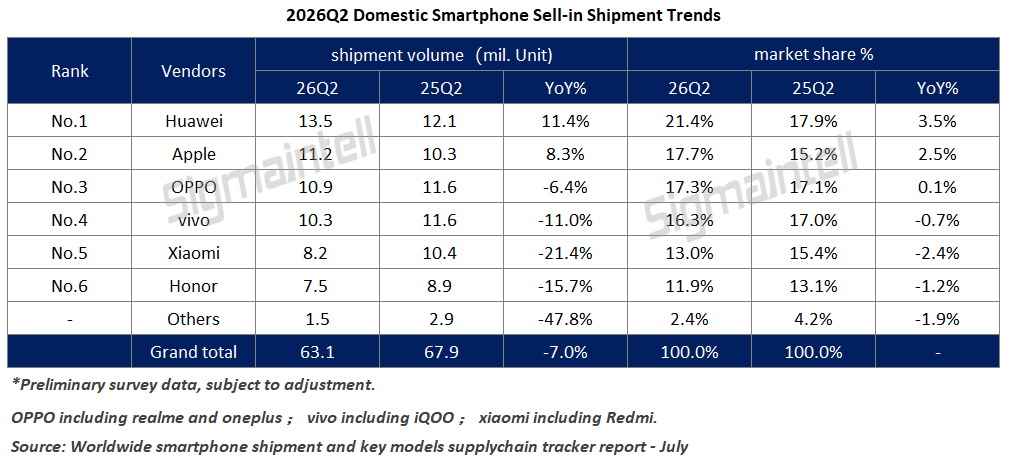

According to Sigmaintell (Sigmaintell) data, China's smartphone shipments in the second quarter of 2026 were about 63.1 million units, a year-on-year decrease of 7%. The weakening of the “state subsidy” effect and the increase in sales prices by manufacturers are the main reasons for the decline in market demand.

(1) Huawei is gradually consolidating its dominant position, and demand for Apple is even stronger. Huawei and Apple bucked the trend in the domestic market, growing 11.4% and 8.3% respectively.

Huawei has always been on a growth trend, achieving double-digit growth in the second quarter. In addition to the high-end product Mate and Pura's dual flagship strategy, the low and middle end (nova16 series and enjoy 90 series) have shown offensive results in sinking cities, sinking channels, sinking silver-haired people, and sinking young people, which is the main reason for its sales contribution.

Apple's contrarian growth stems from two aspects: one is the stickiness and loyalty of its apple ecosystem, which belongs to a fixed group and is a source of stable sales; the other is the price increase of domestic flagships, superimposed on Apple's stable price system, to jointly promote the return of the user base to Apple.

(2) Demand for the Android camp has collectively weakened, and the challenge of resisting costs has intensified. Brands such as OPPO, Vivo, and Honor are forced to adjust product strategies and product sales prices under product cost pressure, while consumers' perception of the value of product price increases (product configuration upgrades) is not strong, and their desire to switch is suppressed. The market has always been in a wait-and-see trend, and it will continue in the short term. This is a serious challenge for domestic brands in the Android camp.

III. Prospects for future trends

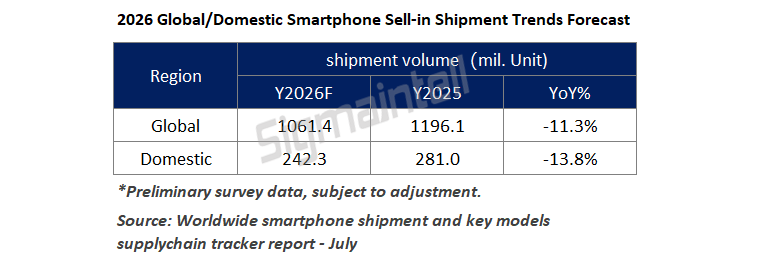

According to data from Sigmaintell (Sigmaintell), based on current supply-side cost pressure and continued weakness on the demand side, global smartphone shipments are expected to be around 1.06 billion units in 2026, a year-on-year decrease of 11.3%. Of these, China shipped about 240 million units, a year-on-year decline of 13.8%.

Global smartphones fell 6% year on year in the first half of 2026 (the Chinese market fell 6.3%). As the low-cost inventory materials purchased by mainstream brand manufacturers were gradually exhausted, cost pressure will be concentrated in the second half of the year. Global smartphones are expected to decline 16.1% year on year in the second half of 2026 (the Chinese market fell 17%). Looking ahead to 2027, the increase in storage prices will stabilize in the first half of 2027, but it is still at a high level, and there is little room for significant decline in the short term. The overall market will still face serious challenges. The global smartphone market is expected to decline 3.3% year on year in 2027 (the Chinese market will decline 5.5%).

Sigmaintell (Sigmaintell) believes that smartphones may usher in a new development trend in the future:

(1) The ultra-low end (below $100) level in the global market has seriously shrunk, forming and defining a new gear pattern. According to Sigmaintell (Sigmaintell) data, the future minimum memory package (4GB+64GB) will cost about $100, and the ultra-low-end smartphone market will experience a serious contraction.

(2) Mainstream brands are thinking about how to use smaller RAM to support AI operation in order to meet the AI needs of low- and mid-range phones under the premise of rising costs. The Apple iPhone 18 standard version is evaluating the use of 9GB of RAM to ensure AI operation.

(3) Looking for a differentiated product circuit. New screen formats and larger batteries will be the main direction of mainstream brands' high-end and low-end product strategies starting in the second half of this year.