Inflation readings across major economies are sending mixed signals, energy prices are swinging, and central banks are rethinking interest rate paths. In this kind of stop start backdrop, many investors are looking for income that feels steadier than the latest data release. That is where the Dividend Powerhouses screener comes in, focusing on companies with more than a 5% yield that is covered, growing and relatively stable. In this article, you will see three of the strongest stocks from this list so you can decide whether they deserve a place in your dividend playbook.

Hero MotoCorp (BSE:500182)

Overview: Hero MotoCorp is a New Delhi based manufacturer of motorcycles, scooters and electric scooters, selling vehicles, parts and related services across India and multiple international markets, with a presence that stretches from Asia to Latin America, Africa and the Middle East.

Operations: Hero MotoCorp generates about ₹474.1b in revenue primarily from its Automotive segment, with ₹415.0b from India and ₹59.1b from outside India.

Market Cap: ₹977.4b

Income focused investors may want to keep Hero MotoCorp on the radar because it couples strong recent earnings growth and solid 12.1% net margins with efforts to move into higher value areas such as premium bikes, electric scooters and export markets. A P/E of 17x that sits below both the wider Indian market and peer averages adds to the appeal, especially as the company invests in EVs through VIDA and Ather Energy and expands parts capacity to support recurring revenue. On the other hand, there is an unstable dividend track record and reliance on India for most sales, so the real question is whether the push into EVs, premium models and overseas markets can offset those pressure points over time.

Hero MotoCorp’s push into premium bikes, EVs and exports could be masking a far more interesting story around what investors are actually paying for that growth, so the DCF valuation analysis for Hero MotoCorp might change how you see the key risk reward trade off

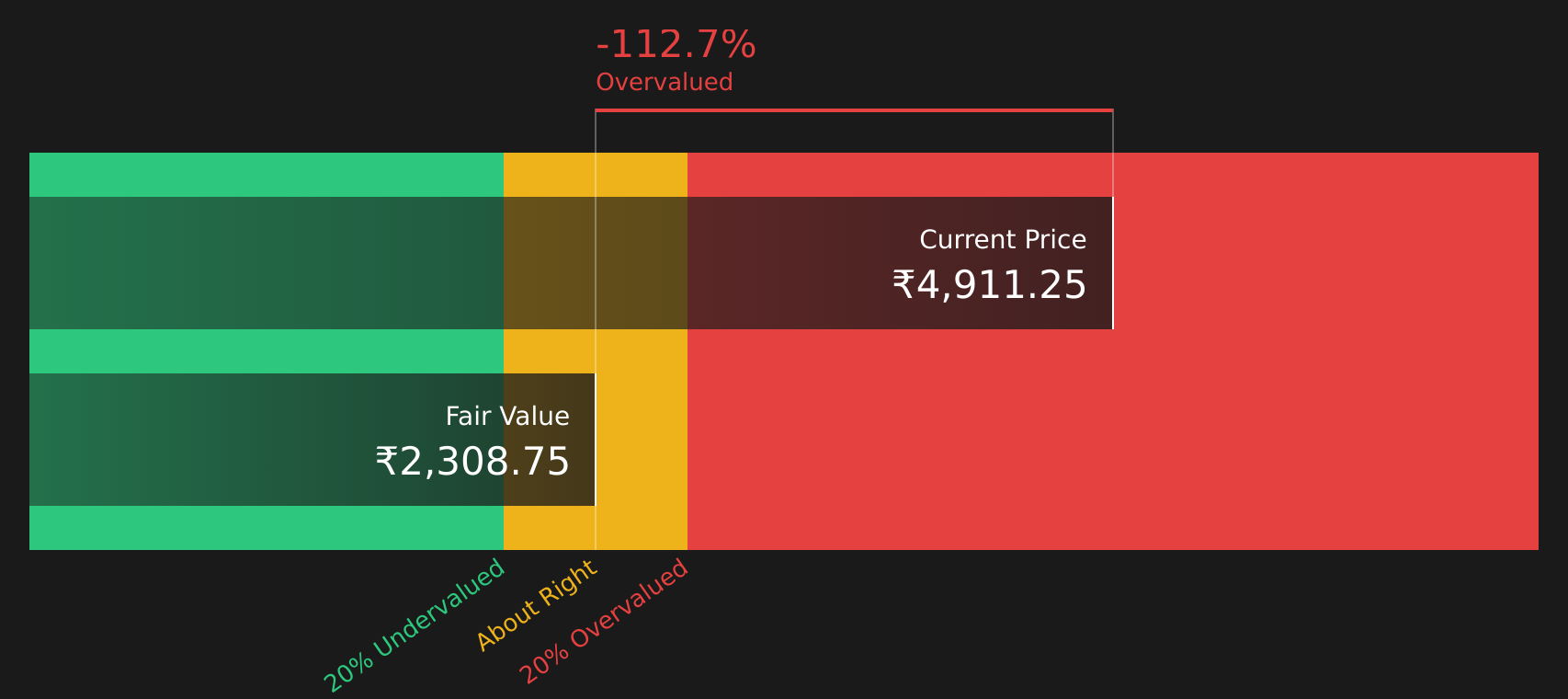

Tata Consultancy Services (NSEI:TCS)

Overview: Tata Consultancy Services is a Mumbai based IT services company that builds and runs large scale software, cloud, AI and digital platforms for clients across banking, insurance, manufacturing, life sciences, retail, public services and more.

Operations: Tata Consultancy Services generates about ₹2,765.6b in revenue, led by Banking, Financial Services and Insurance at ₹1,066.2b, followed by Consumer Business at ₹434.2b and Communication, Media and Technology at ₹406.5b, with additional contributions from Life Sciences and Healthcare, Manufacturing and other segments.

Market Cap: ₹7,961.96b

Income investors may want to look closely at Tata Consultancy Services because its 5.07% dividend yield is backed by high quality earnings, a very strong 45.2% return on equity and a portfolio of AI and cloud projects that includes major contracts like the New Terminal One modernization at New York’s JFK Airport. At the same time, growth is expected to be slower than the wider Indian market and IT industry, net margins have eased slightly and recent revenue trends in North America and some consumer facing segments show that project delays and cautious client spending are real risks. The key question for investors is how that balance of quality, income and moderated growth compares with what they are paying today and what they might reasonably expect over the next few years.

Tata Consultancy Services looks like a high quality income stock whose premium earnings and 45.2% return on equity may not be fully reflected in expectations yet, and the analysis report for Tata Consultancy Services hints at one underappreciated twist in that story.

Indian Oil (NSEI:IOC)

Overview: Indian Oil is a New Delhi based integrated energy company that refines crude oil, transports fuel through pipelines, sells petrol, diesel and LPG, and also operates businesses in petrochemicals, gas, lubricants and emerging clean energy such as renewables, biofuels and green hydrogen across India and some international markets.

Operations: Indian Oil generates about ₹8,421.95b in revenue from Petroleum Products, ₹445.12b from Gas, ₹281.02b from Petrochemicals and ₹52.88b from Other Business Activities, partly offset by ₹186.45b of inter segment revenue.

Market Cap: ₹1,887.39b

Income investors may want to pay attention to Indian Oil because it combines a high earnings base, recent profit of ₹420.96b and a dividend payout with what analysts regard as good value, trading well below some fair value estimates and at a P/E that is far under the Indian Oil and Gas industry average. At the same time, heavy capital spending, high leverage and an unstable dividend history show that government policy, energy transition timing and execution on large refinery and renewable projects will matter a lot for future cash flows. The interesting part is how this mix of earnings momentum, clean energy projects and policy risk fits together for long term dividend focused investors.

Indian Oil’s earnings base and clean energy push could be masking a much tighter risk reward profile than headline valuation suggests, so the 3 key rewards and 3 important warning signs (1 is major!) might be the missing piece in your thesis

The three dividend stocks in this article are just the starting point, with the full Dividend Powerhouses (3%+ Yield) screener surfacing 32 more companies that pair high yields with equally compelling stories around earnings quality, payout strength and business model resilience. Use Simply Wall St to identify, analyze and filter for the specific catalysts and narratives that matter to you so you can focus on the dividend opportunities that best align with your own income goals.

Take Control of Your Investment Journey

If Indian Oil or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Dividends?

Fresh opportunities can move from quiet accumulation to full breakout faster than most investors react, so scan these curated ideas before the crowd catches on and act now.

- Spot potential market leaders early by running the 503 high quality undiscovered gems that are still flying under the radar for now, before momentum really builds.

- Strengthen your defense by reviewing the 298 resilient stocks with low risk scores designed to help you focus on resilient businesses when volatility picks up and certainty feels scarce.

- Ride long term infrastructure themes by checking the 34 power grid technology and infrastructure stocks capturing companies positioned around critical grid upgrades while that story still feels early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com