As the Canadian market experiences robust earnings growth, largely propelled by the energy and material sectors, investors are keenly observing whether this momentum will sustain beyond the second quarter's peak. In this dynamic environment, identifying promising small-cap stocks that can thrive amidst these conditions requires a focus on companies with solid fundamentals and potential for long-term growth.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Alvopetro Energy | 19.58% | 10.05% | 8.67% | ★★★★★★ |

| China Gold International Resources | 22.48% | -1.05% | 7.48% | ★★★★★★ |

| Fortuna Mining | 7.42% | 12.80% | 34.67% | ★★★★★★ |

| Mako Mining | 24.28% | 36.18% | 60.06% | ★★★★★★ |

| Calfrac Well Services | 22.77% | 11.78% | 32.39% | ★★★★★★ |

| GoGold Resources | NA | 11.97% | -3.31% | ★★★★★★ |

| Santacruz Silver Mining | 23.34% | 26.91% | 51.48% | ★★★★★★ |

| Eldorado Gold | 28.48% | 15.28% | 50.23% | ★★★★☆☆ |

| Logan Energy | 20.64% | 29.77% | 62.16% | ★★★☆☆☆ |

| Journey Energy | 14.72% | 8.95% | -32.77% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

GoGold Resources (TSX:GGD)

Simply Wall St Value Rating: ★★★★★★

Overview: GoGold Resources Inc. is a company focused on the exploration, development, and production of silver, gold, and copper primarily in Mexico, with significant assets including the Los Ricos property and Parral Tailings project; it has a market capitalization of approximately CA$1.37 billion.

Operations: Revenue for GoGold Resources primarily comes from the Parral Tailings project, generating approximately $97.24 million.

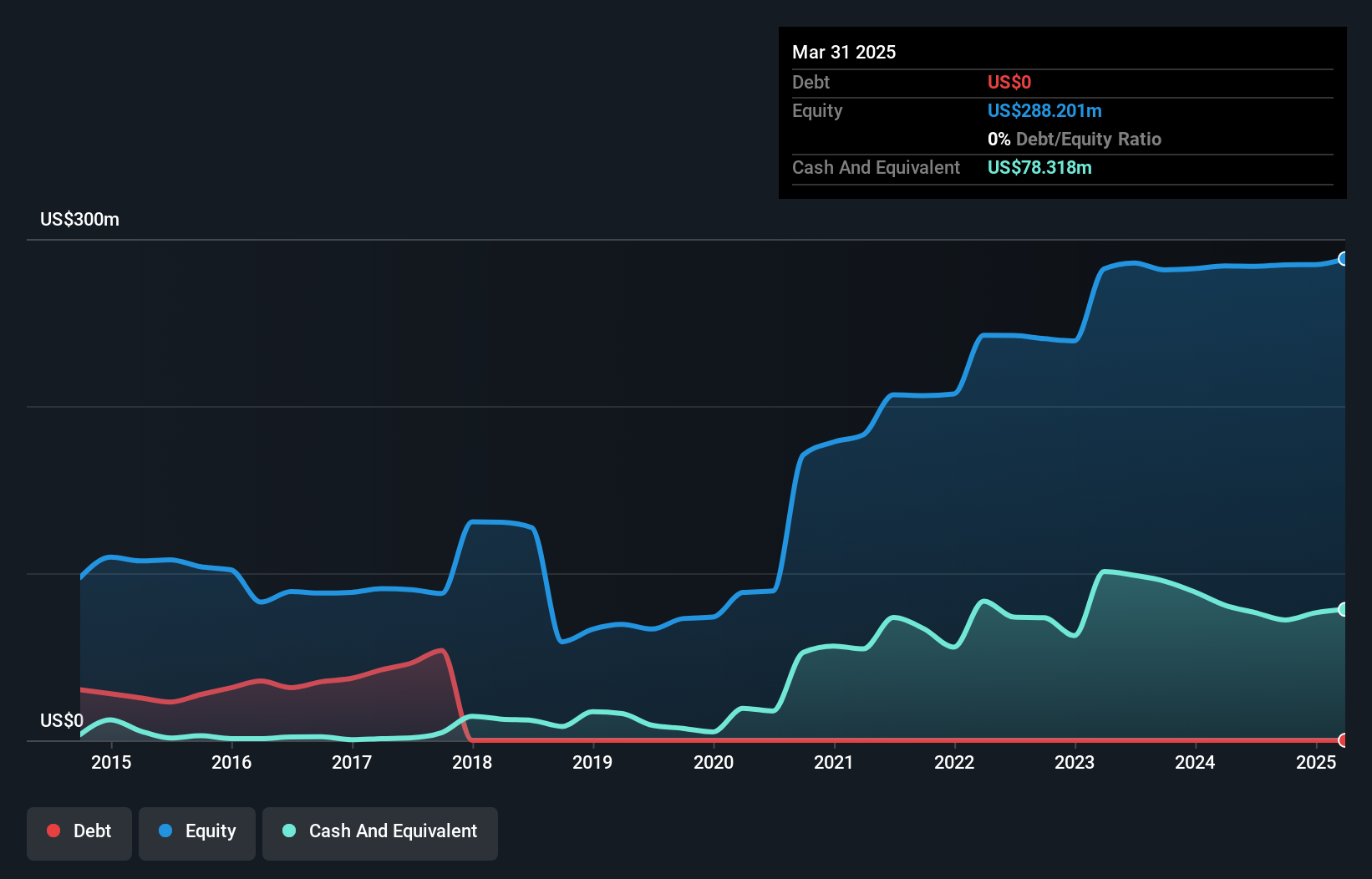

GoGold Resources, a nimble player in the mining sector, is making waves with its impressive earnings growth of 1214.3% over the past year, outpacing industry norms. The company operates debt-free and boasts high-quality earnings, which underscores its financial health. Recent quarterly results show silver production at 268,673 ounces while net income for six months reached US$29.75 million compared to US$3.22 million previously. With permits secured for the Los Ricos South project in Mexico, GoGold is poised to enhance its production capabilities and contribute positively to regional economic development through sustainable practices and local employment opportunities.

- Dive into the specifics of GoGold Resources here with our thorough health report.

Review our historical performance report to gain insights into GoGold Resources''s past performance.

Torex Gold Resources (TSX:TXG)

Simply Wall St Value Rating: ★★★★★★

Overview: Torex Gold Resources Inc. is a mineral exploration company focused on acquiring, exploring, and developing mineral properties in Mexico and the United States, with a market capitalization of approximately CA$5.10 billion.

Operations: Torex Gold Resources generates revenue primarily from its Morelos Complex, amounting to $1.67 billion. The company's financials reflect a focus on this segment as the primary source of income.

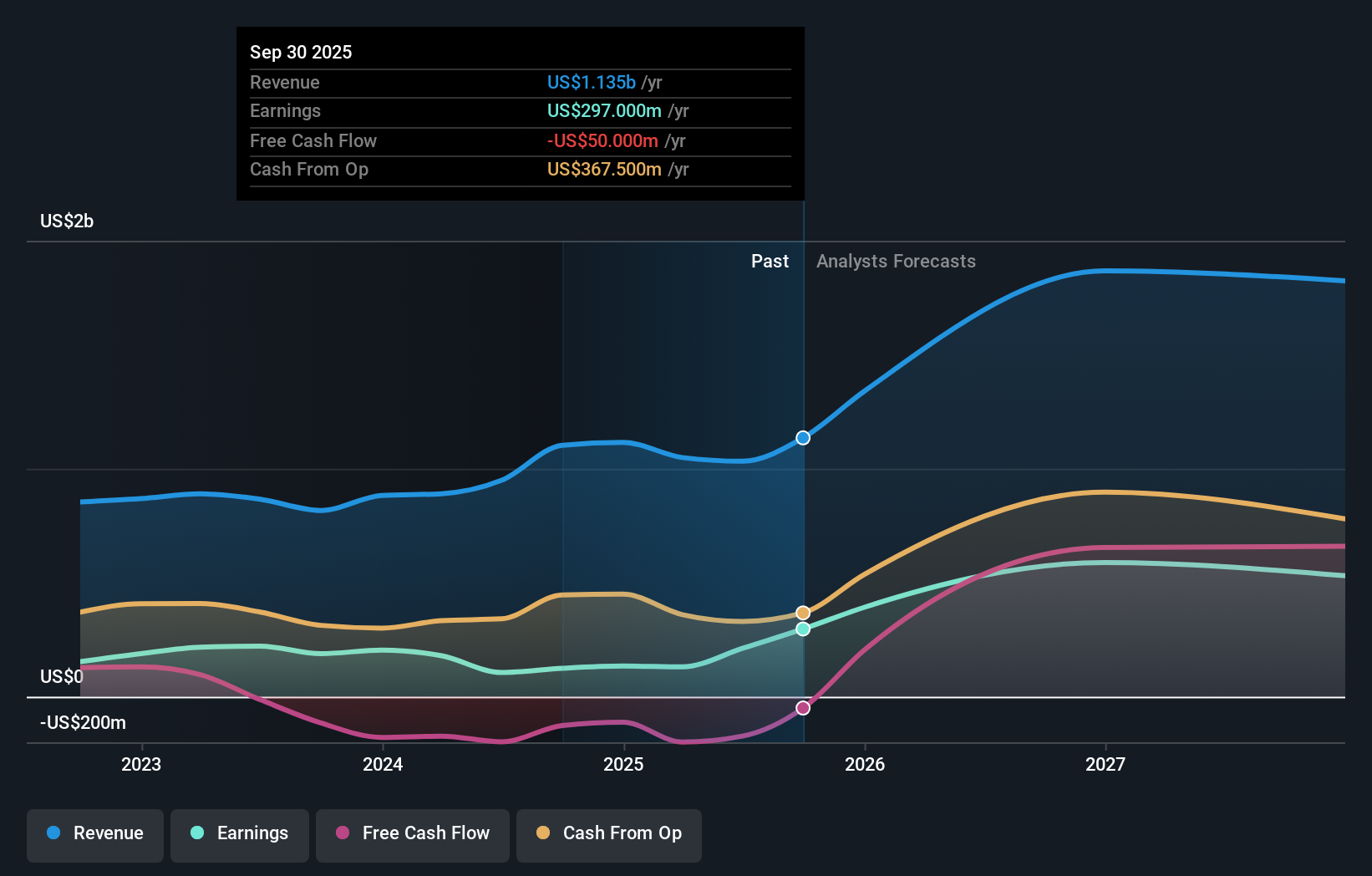

Torex Gold Resources, a Canadian mining company, is making strides with its strategic initiatives and robust exploration efforts. The firm has been debt-free for five years, a notable achievement given its past debt-to-equity ratio of 0.1%. Over the last year, Torex's earnings surged by 338%, outpacing the industry growth of 137%. Recent drilling at Media Luna and ELG Underground shows promising high-grade mineralization results, such as 9.14 grams per tonne over 7.5 meters at Media Luna East. These developments suggest potential resource expansion and may bolster Torex's production profile in the future.

Logan Energy (TSXV:LGN)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Logan Energy Corp. is involved in the exploration, development, and production of crude oil and natural gas properties with a market capitalization of CA$636.25 million.

Operations: Logan Energy generates revenue primarily from its oil and gas exploration and production segment, amounting to CA$176.06 million.

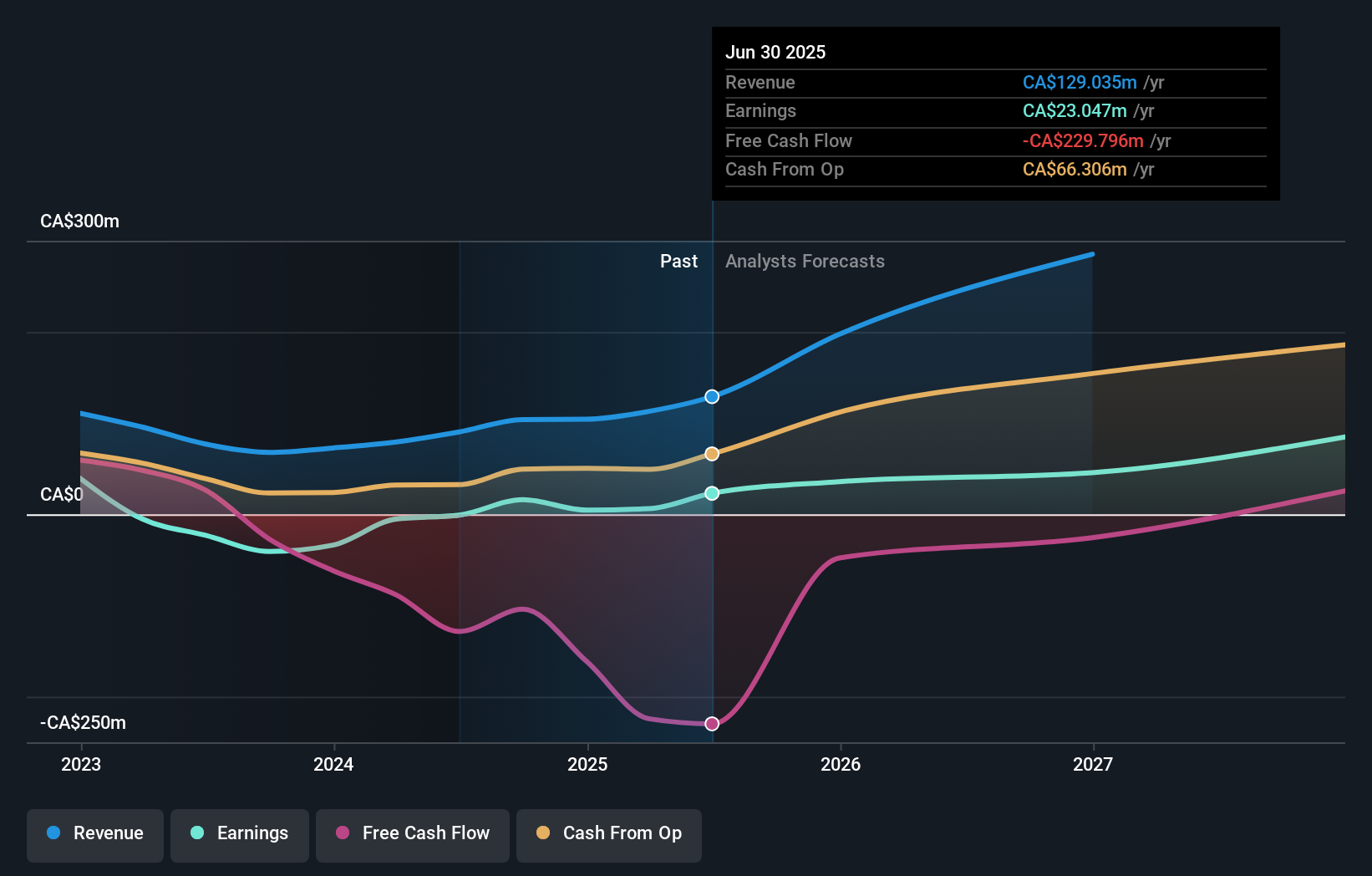

Logan Energy, a small player in the energy sector, has shown impressive growth with earnings surging 365.1% over the past year, outpacing the industry average of -14.8%. Despite a net loss of CAD 9.56 million in Q1 2026 compared to CAD 0.394 million a year prior, its production guidance for the second half of 2026 is optimistic at an increased range of 19,000 to 20,000 BOE/d. Trading at a significant discount—79.5% below its estimated fair value—Logan's interest payments are well-covered by EBIT at a ratio of 4.1x, suggesting financial stability amidst expansion plans.

- Delve into the full analysis health report here for a deeper understanding of Logan Energy.

Gain insights into Logan Energy's historical performance by reviewing our past performance report.

Where To Now?

- Navigate through the entire inventory of 14 TSX Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com