Prosus (ENXTAM:PRX) has just wrapped up a series of debt moves that matter for equity holders, including tender offers and new bond issues that reshape its 2027 maturities and longer term funding profile.

See our latest analysis for Prosus.

Prosus shares trade at €40.43 after a mixed period, where the 1 month share price return of 4.19% contrasts with a year to date decline of 24.86% and a 3 year total shareholder return of 32.62%. This suggests recent pressure despite a stronger multi year picture, as investors weigh the debt refinancing against longer term value drivers.

If this debt reshaping has you thinking about where capital could work differently, it might be worth seeing which other companies are catching attention through 106 top founder-led companies

Prosus has tidied up its 2027 debt, yet the share price is still down sharply this year. This leaves you weighing up whether today’s level is a reasonable entry point or whether patience might be better rewarded in the valuation work that follows.

Most Popular Narrative: 2% Undervalued

On the most followed narrative, Prosus screens as slightly undervalued, with a fair value of €41.27 against the last close of €40.43. This puts recent debt moves in the context of a modest upside case built on earnings and margin assumptions rather than a deep discount story.

In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 15.0x on those 2029 earnings, up from 8.6x today. This future PE is greater than the current PE for the NL Multiline Retail industry at 7.5x.

The narrative leans on steady revenue expansion, slimmer profit margins and a richer future earnings multiple. Want to see which assumptions really carry the fair value and how they fit together?

Result: Fair Value of €41.27 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if Prosus delivers stronger execution on AI rollouts or proves that OLX and iFood can consistently support margins, this more cautious narrative could be challenged.

Find out about the key risks to this Prosus narrative.

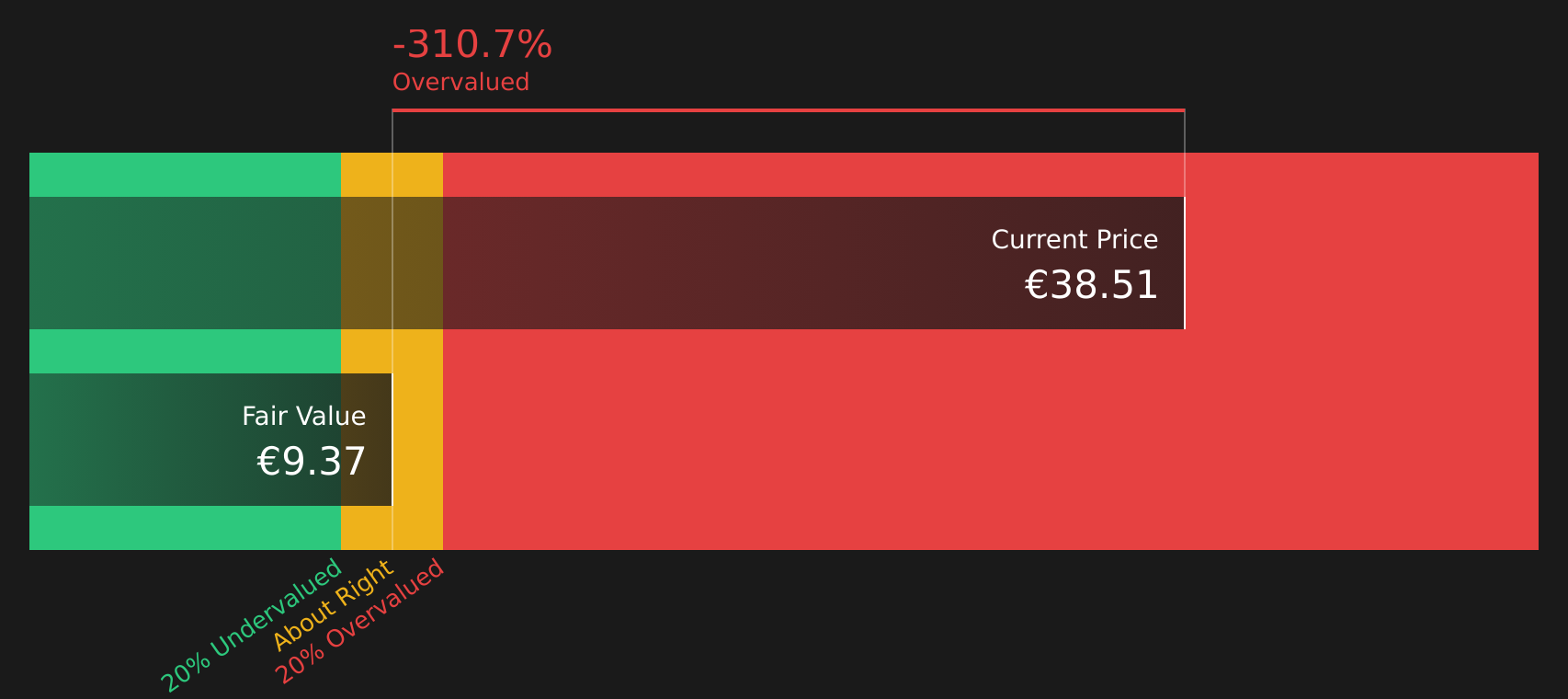

Another View: Prosus Through the SWS DCF Lens

The fair value narrative around Prosus looks different when using the SWS DCF model. On this framework, Prosus at €40.43 is trading above an estimated future cash flow value of €9.39, which flags the stock as overvalued on cash generation alone.

That gap raises a simple question for you as an investor: are analysts overestimating Prosus's ability to convert its portfolio into cash, or is the DCF underestimating assets that may not show up cleanly in near term cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Prosus for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 220 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Prosus pulled between mixed returns and conflicting valuation signals, this is a moment to move quickly, review the full data, and weigh both the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Prosus?

Prosus may be front of mind today, but some of the most interesting opportunities often sit just outside your current watchlist, waiting for a closer look.

Use the Simply Wall Street Screener to quickly surface fresh ideas while this analysis is still top of mind.

- Target potential mispricings by scanning companies that combine quality with attractive valuations through the 220 high quality undervalued stocks.

- Prioritise resilience by focusing on businesses with stronger finances using the solid balance sheet and fundamentals stocks screener (417 results).

- Spot under followed opportunities before the crowd by checking the screener containing 506 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com