- Recently, Zacks assigned ZTO Express (Cayman) a Rank #1 (Strong Buy), highlighting an improved earnings outlook versus peer C.H. Robinson Worldwide, supported by ZTO’s lower forward P/E ratio of 11.80 and PEG ratio of 0.87.

- This combination of a top analyst ranking and comparatively cheaper valuation metrics has drawn attention to ZTO as a potentially more compelling value option within the logistics space.

- Now we will examine how ZTO’s upgraded ranking and relative valuation advantage might influence its existing investment narrative and outlook.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

ZTO Express (Cayman) Investment Narrative Recap

To own ZTO Express (Cayman), you need to believe it can convert parcel scale and automation into resilient margins despite pricing pressure and slowing industry growth. The Zacks Rank #1 and lower forward P/E and PEG highlight improved earnings expectations versus peers, but they do not materially change the key near term catalyst of cost savings from technology or the central risk of ongoing price competition compressing margins and net income.

The most relevant recent development is ZTO’s Q1 2026 result, which showed higher revenue and earnings versus the prior year. This concrete earnings delivery now sits alongside the upgraded Zacks ranking, giving fresh data for how ZTO is managing volume growth, pricing pressure and cost efficiency. Together, they help investors weigh whether current valuation metrics reflect the execution risk around margins, parcel mix shifts and heavy investment in automation.

Yet, despite the upbeat ranking, investors should be aware that sustained price competition and slower parcel growth could still...

Read the full narrative on ZTO Express (Cayman) (it's free!)

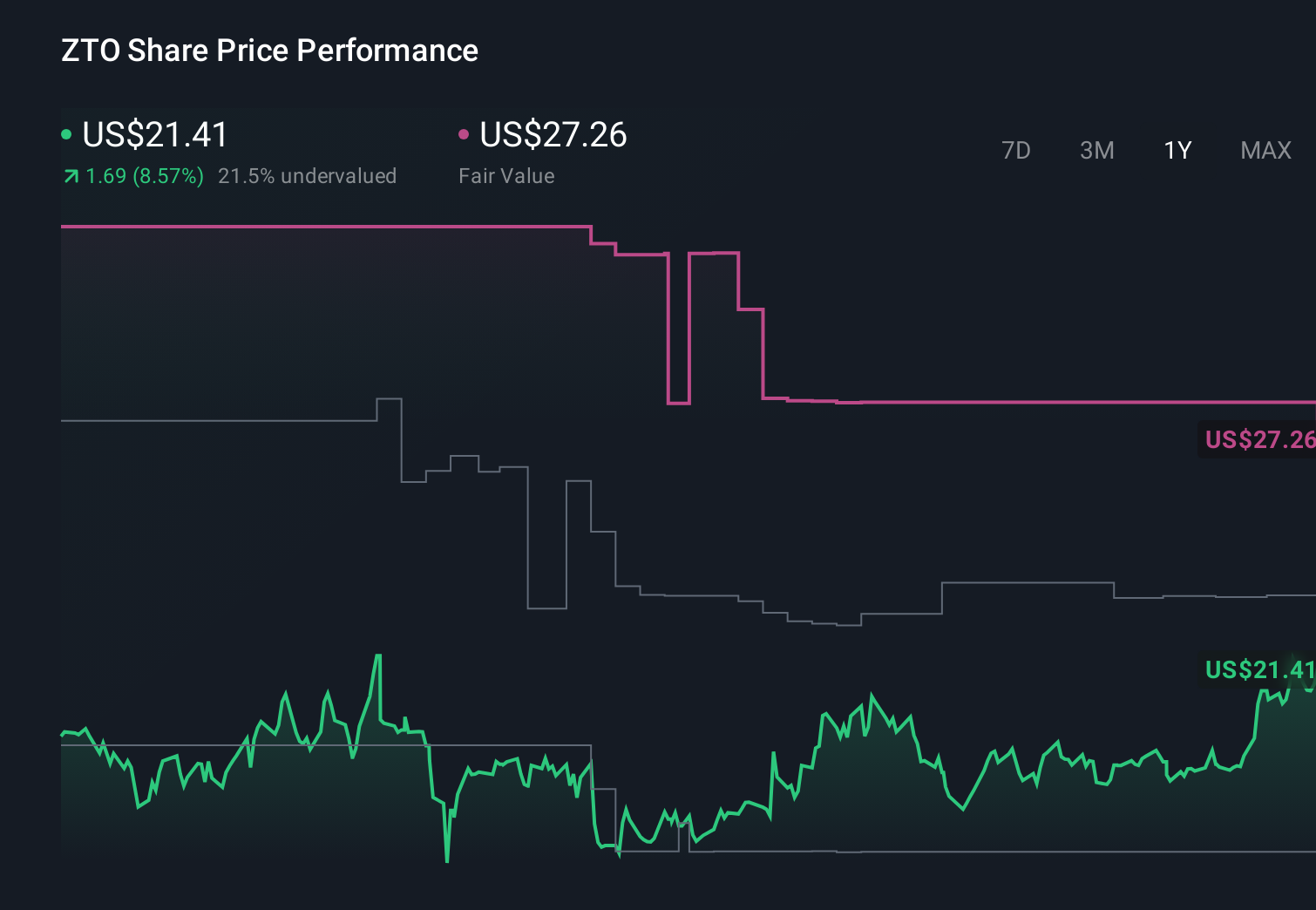

ZTO Express (Cayman)'s narrative projects CN¥70.4 billion revenue and CN¥13.1 billion earnings by 2029. This requires 11.0% yearly revenue growth and about CN¥3.9 billion earnings increase from CN¥9.2 billion today.

Uncover how ZTO Express (Cayman)'s forecasts yield a $29.03 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once penciled in revenue of about CN¥77.1 billion and earnings near CN¥15.4 billion by 2029, yet the latest Zacks upgrade and valuation debate sit against unresolved concerns about rising capital spending and customer concentration, reminding you that opinions can differ widely and both the bullish and cautious cases may evolve as new data comes in.

Explore 6 other fair value estimates on ZTO Express (Cayman) - why the stock might be a potential multi-bagger!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ZTO Express (Cayman) research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ZTO Express (Cayman) research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ZTO Express (Cayman)'s overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com