- In the days leading up to its 22 July 2026 earnings release, GE Vernova drew attention as analysts pointed to strong anticipated second‑quarter results supported by AI data center–driven power demand and a growing backlog in its Power and Electrification segments, even as the Wind business continued to face project delays and supply‑chain issues.

- An interesting angle is GE Vernova’s decision to commit US$11 billion to capital expenditure and R&D through 2028 to capture AI‑related power and grid opportunities, a move that could reshape the balance between growth potential and execution risk across its large infrastructure project portfolio.

- We’ll now examine how this AI‑driven demand and heavy investment program could influence GE Vernova’s existing investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

GE Vernova Investment Narrative Recap

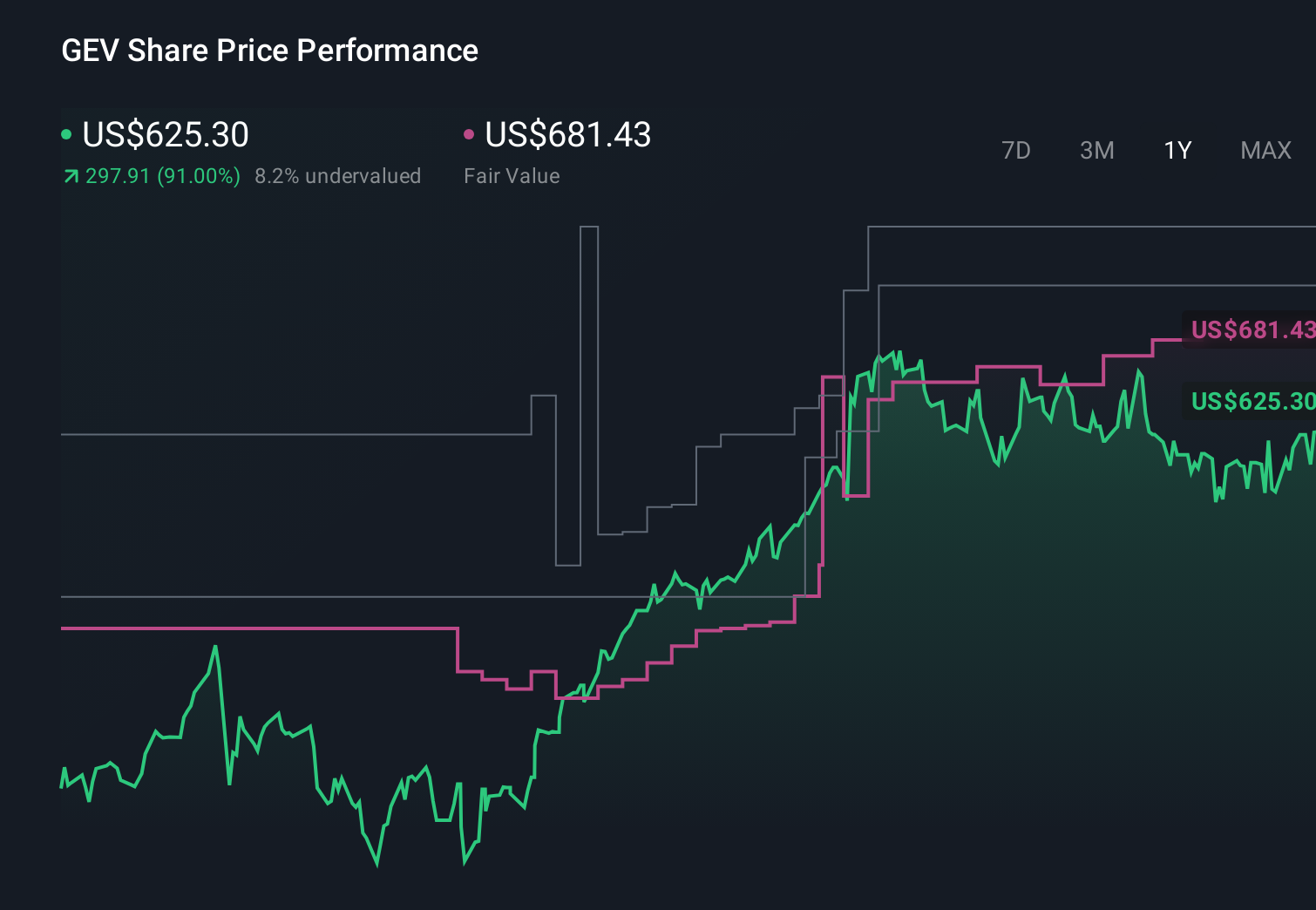

To own GE Vernova, you have to believe that rising electrification and AI data center demand will keep feeding a high‑margin backlog in Power and Electrification while the loss‑making Wind segment is gradually contained. The immediate catalyst is whether the 22 July earnings confirm the expected revenue and margin strength that recent commentary points to. The biggest risk remains execution on large, complex projects where cancellations or delays could quickly unsettle this upbeat setup.

The most relevant recent development is GE Vernova’s plan to spend US$11,000,000,000 on capex and R&D through 2028 focused on AI‑related power and grid needs. This commitment sits right at the intersection of today’s enthusiasm around AI‑driven electricity demand and the company’s reliance on big infrastructure orders, sharpening both the upside case around backlog quality and the downside risk if project economics or customer needs shift.

Yet against this promising AI story, investors should still be aware of how exposed GE Vernova is to large, lumpy grid and wind projects that could...

Read the full narrative on GE Vernova (it's free!)

GE Vernova's narrative projects $60.9 billion revenue and $9.7 billion earnings by 2029. This requires 15.7% yearly revenue growth and about a $0.3 billion earnings increase from $9.4 billion today.

Uncover how GE Vernova's forecasts yield a $1212 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts were assuming GE Vernova’s earnings could fall to about US$6.0 billion by 2029 even as geopolitical and policy risks threatened the very backlog many bulls are focused on today, reminding you that reasonable people can look at the same AI‑driven demand story and reach very different conclusions that might need revisiting after this earnings season.

Explore 10 other fair value estimates on GE Vernova - why the stock might be worth as much as 37% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your GE Vernova research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free GE Vernova research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GE Vernova's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com