Warrant Issuers

Approved warrant issuers

Warrants may only be issued by a bank or other financial institution approved by the Australian Securities Exchange (ASX) as a warrant issuer.

ASX Operating Rules set out stringent criteria that an issuer must meet in order to be approved to issue warrants.

In brief, to be eligible to issue warrants, an institution must:

- Be regulated under the Banking Act 1959, or

- Hold an Australian Financial Services Licence, have an investment grade credit rating, and meet certain capital requirements, or

- Be a government, or

- Have a guarantor that meets at least one of the above criteria, or

- Propose to issue fully covered warrants.

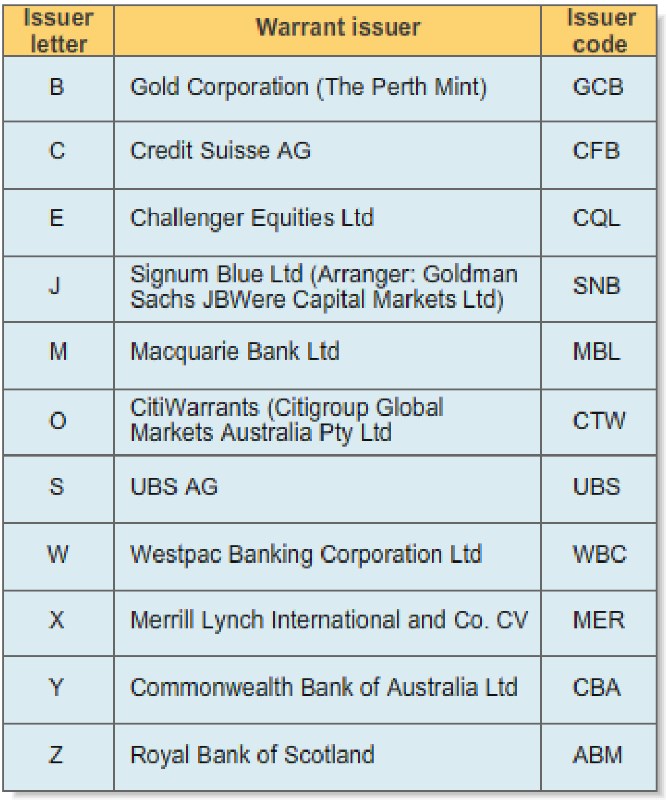

The table opposite sets out the approved issuers, including the letter that identifies the issuer as part of a warrant code.

Role of warrant issuers

Issuers have a central role in the warrants market.

Aside from issuing warrants, one of the most important functions of an issuer is to develop new products in response to investor demand. Over the years, warrant issuers have become very creative in structuring products to appeal to a wide range of investors. Because warrants are not a standardised product like exchange traded options, there is the flexibility to tailor products to suit specific investor needs.

Other responsibilities of the issuer include:

- Providing liquidity for warrant traders in the secondary market

- Meeting obligations under the terms and conditions contained in the warrant's PDS, and

- Providing information such as indicative pricing matrices and educational material.

Market obligations

Warrant issuers have certain obligations in the interests of promoting a liquid market in which warrant holders can sell their warrants.

Under ASX Operating Rules, issuers have a choice.

They can ensure that the warrant series has an initial spread of holders that, in the opinion of ASX, is adequate and reasonable, or they can arrange for a market to be made in the warrant series on an ongoing basis. In practice, most issuers choose to meet their obligations by making a market.

'Making a market' means ensuring that a reasonable bid and volume is maintained in the market for a prescribed period of the trading day.

As a result, there should be a price quoted on the trading system at which warrant holders will be able to sell during most of the normal Trading Day. Warrant issuers will usually display an offer as well as a bid price.

For more details, please refer to Warrants market making on the ASX website.

Indicative pricing matrices

Many warrant issuers publish an indicative pricing matrix for their warrants on a daily basis.

The matrix sets out various prices for the underlying for the day, and gives the issuer's expected bid/offer spread for the warrant for that underlying price.

These prices are not guaranteed, and should be used only as a guide. Changes in volatility or other price sensitive variables may mean that the issuer's buy/sell spread varies from that specified in the matrix.

You can find a warrant's indicative price matrix on the issuer's website. The issuer may also distribute the information via email.

Each time a warrant issuer issues a warrant, the terms and conditions of the warrant must be set out in a disclosure document, also known as a Product Disclosure Statement (PDS). The ASX Operating Rules and the Corporations Act specify the information and terms that must be included in this document.

The disclosure document contains information to help you assess the benefits, risks, features, rights and obligations associated with a warrant, and the issuer's capacity to fulfil its obligations.

Because warrants are not standardised, there can be significant differences between warrants offered by the various issuers, and even between different warrant series offered by the one issuer. It is therefore essential to read the PDS for a warrant you are considering investing in, to ensure that it is appropriate for your financial situation and objectives.

A warrant's disclosure document is available from:

- the warrant issuer (either in electronic format or hard copy)

- your broker

- the ASX website through the Warrant Price Search function.

Warrant codes

Each warrant has a six-character ASX code, to distinguish it from the thousands of other warrants on issue.

The individual letters of the code describe some of the main features of the warrant:

- the first three characters of the code identify the underlying instrument. For most equity and instalment warrants this is the same as the three-letter ASX code of the underlying company shares.

- the fourth character of the code identifies the type of warrant.

- the fifth character of the code identifies the warrant issuer.

- the sixth character of the code identifies the particular warrant series. For trading style warrants the range A to O is used for call warrants, while the range P to Z is used for put warrants. In addition, the range 1 to 9 may be used for call and put warrants.

For a detailed explanation of warrant codes, please refer to Understanding warrant codes.