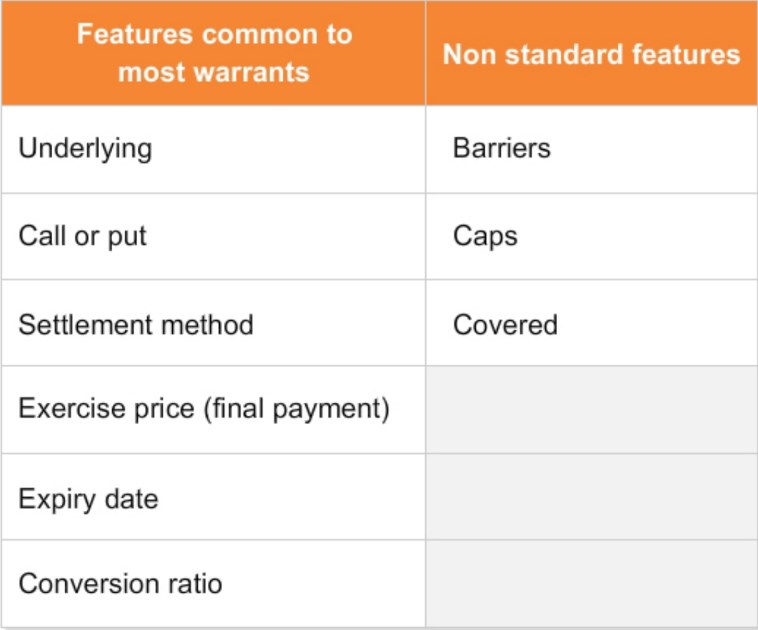

Warrant features

Warrants are not standardised. There are a wide range of warrant types, and the features of warrants offered by various issuers can vary widely. There can even be significant differences between different warrant series offered by the one issuer.

The Product Disclosure Statement (PDS) sets out the terms and conditions of the warrant in detail. When reading these documents, be aware that different issuers may not always use the same words to describe a given warrant feature. For example, the term 'loan amount', 'final payment' or 'exercise price' may be used interchangeably to refer to the final payment of an instalment.

The price (or first payment) of the warrant is not specified in the PDS, but is determined by the price of the underlying asset, and market conditions at the time.

Underlying

Warrants are issued over a range of underlying assets, including: ASX-listed securities, shares listed on an overseas exchange, baskets of ASX-listed securities, share price indices, commodities and currencies.

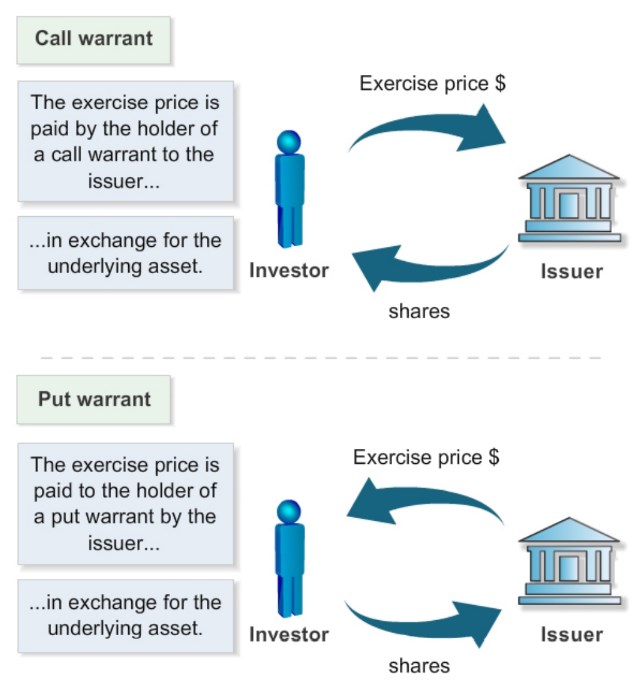

Call or put

A warrant is either a call or a put.

A call gives you the right to buy the underlying asset from the warrant issuer. A put gives you the right to sell the underlying asset to the issuer.

Settlement method

A warrant may be deliverable or cash settled.

Deliverable warrants are settled by a transfer of the underlying asset. If, for example, you exercise a call warrant over XYZ shares, the issuer transfers ownership of XYZ shares to you.

Cash settled warrants are settled by a cash payment from the warrant issuer to the holder. If the warrant is in-the-money, the difference between the warrant's exercise price and the price of the underlying asset is paid to the holder.

Exercise price (final payment)

The exercise (or strike) price is the amount of money that must be paid on exercise of the warrant:

- by the warrant holder to the issuer, in the case of a call warrant, or

- by the issuer to the warrant holder, in the case of a put warrant.

The exercise price is generally fixed at the time the warrant is issued. However, in the case of some investment-style warrants, such as self-funding instalments and rolling instalments, the exercise price may be adjusted over time.

The exercise price may also be adjusted during the warrant's life if there is some corporate event that affects the value of the underlying asset, such as a share split or bonus issue. The PDS will explain how any such adjustments would be implemented.

For most warrants, the exercise price is denominated in Australian dollars. However, the exercise price of index warrants is expressed in points, and some commodity and currency warrants may have an exercise price expressed in a foreign currency.

Expiry date

The expiry date is the final date of the warrant's life. This is the last date on which the warrant may be exercised. At the end of this day, the warrant lapses, and the holder's right to exercise the warrant ceases.

If the warrant has been validly exercised, the issuer must deliver or take delivery of the underlying instrument, or make a cash payment according to the warrant's terms.

Exercise style

A warrant is either American style exercise or European style exercise.

An American style instalment may be exercised at any time during the life of the warrant, while a European style warrant may be exercised only on the expiry date.

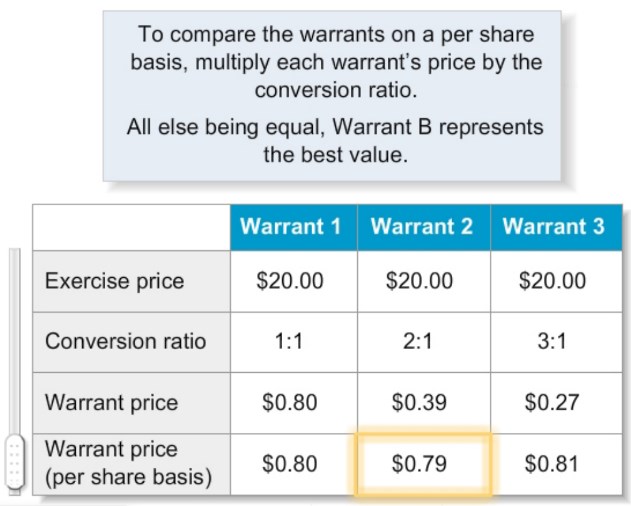

Conversion ratio

The conversion ratio refers to the number of warrants that must be exercised in order to transfer the underlying instrument.

Some warrants convert on a 1:1 basis, while for others, the holder must exercise two or more warrants to buy or sell one underlying.All else being equal, the higher the conversion ratio, the lower the price of the warrant. A warrant with a 2:1 conversion ratio should trade at roughly half the price of a warrant that converts 1:1.

You need to take into account the conversion ratio when comparing different warrants over the same underlying, and be sure to compare the warrants on a 'per share' basis.

First, check that the exercise price, expiry date and other important features of the warrants you are comparing are the same.

Then, to compare on a per share basis, simply multiply each warrant's price by the warrant's conversion ratio.

Non-standard features a warrant may have include:

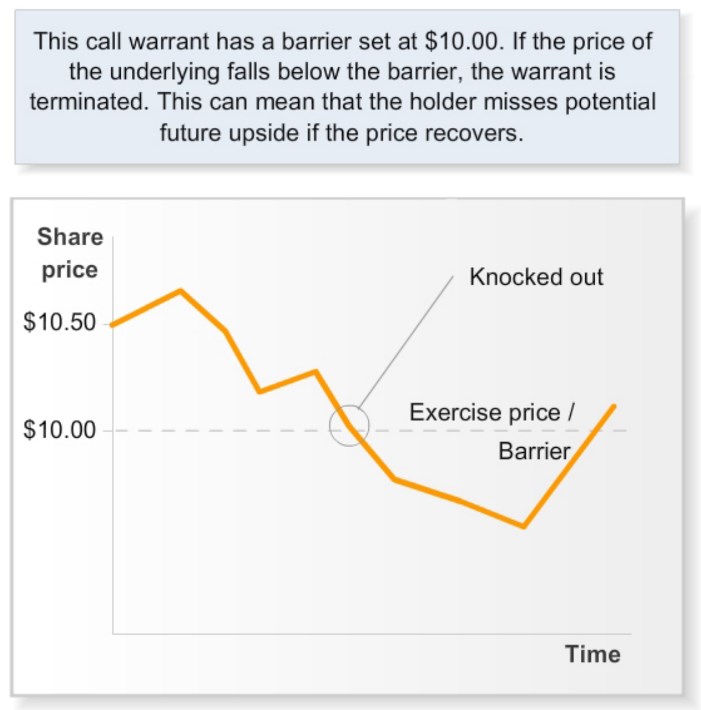

Barriers

Some types of warrants, in particular knock-out warrants, have a barrier feature. If the price of the underlying breaches the specified barrier, an event occurs. For example, the issuer may have the power to terminate the warrant, or adjust the exercise price. The consequences of breaching a barrier are specified in the Disclosure Document.

Caps

Some warrants have their upside potential capped at a certain level. A cap level is fixed by the issuer at the time of issue. If the value of the underlying is above the cap level on exercise or at expiry, settlement of the warrant is based on a return equal to the cap level.

As the profit potential is limited, a capped warrant should trade at a lower price than an uncapped warrant, all else being equal.

Covered Warrants

A warrant is 'covered' if the issuer places the underlying instrument in a trust or similar custodial arrangement on behalf of the holder. Most instalments are covered.

Information contributed by ASX. To see the full course on Warrants go to: https://www.asx.com.au/investors/investment-tools-and-resources/online-courses/warrants-course