Is Prestige Consumer Healthcare’s Upbeat Outlook and Buyback Activity Reframing Its Long-Term Story (PBH)?

- Prestige Consumer Healthcare recently reported second-quarter results that surpassed analyst expectations, raised its adjusted earnings guidance to the high end of the prior range, and reaffirmed revenue goals for fiscal 2026 despite supply constraints affecting the Clear Eyes product line.

- The company also repurchased approximately 1.1 million shares last quarter and remains focused on disciplined use of strong free cash flow, including potential M&A to drive long-term growth and value.

- We'll now explore how Prestige's guidance upgrade and active capital allocation may impact the company's investment narrative going forward.

Find companies with promising cash flow potential yet trading below their fair value.

Prestige Consumer Healthcare Investment Narrative Recap

To own Prestige Consumer Healthcare, an investor needs to believe the company can recover from supply chain disruptions, particularly with the Clear Eyes product line, and capitalize on consistent free cash flow and disciplined capital allocation. The latest results, beating earnings expectations and raising adjusted EPS guidance, suggest some stabilization, but they do not materially change the near-term catalyst: recovery of product supply, nor do they remove the primary risk of prolonged supply challenges or delayed normalization in market share. Among management’s recent moves, the decision to raise adjusted EPS guidance to the upper end of the previous range stands out. This refinement to profit expectations, despite lower year-over-year sales, reflects confidence in operations and supports the case for supply improvement as the most important catalyst now. EBIT performance, ongoing share buybacks, and completion of the Pillar5 acquisition remain pivotal as the company steers through its supply issues. On the other hand, investors should still be mindful of the potential for further disruptions in key brand supply chains if recovery proves slower than expected...

Read the full narrative on Prestige Consumer Healthcare (it's free!)

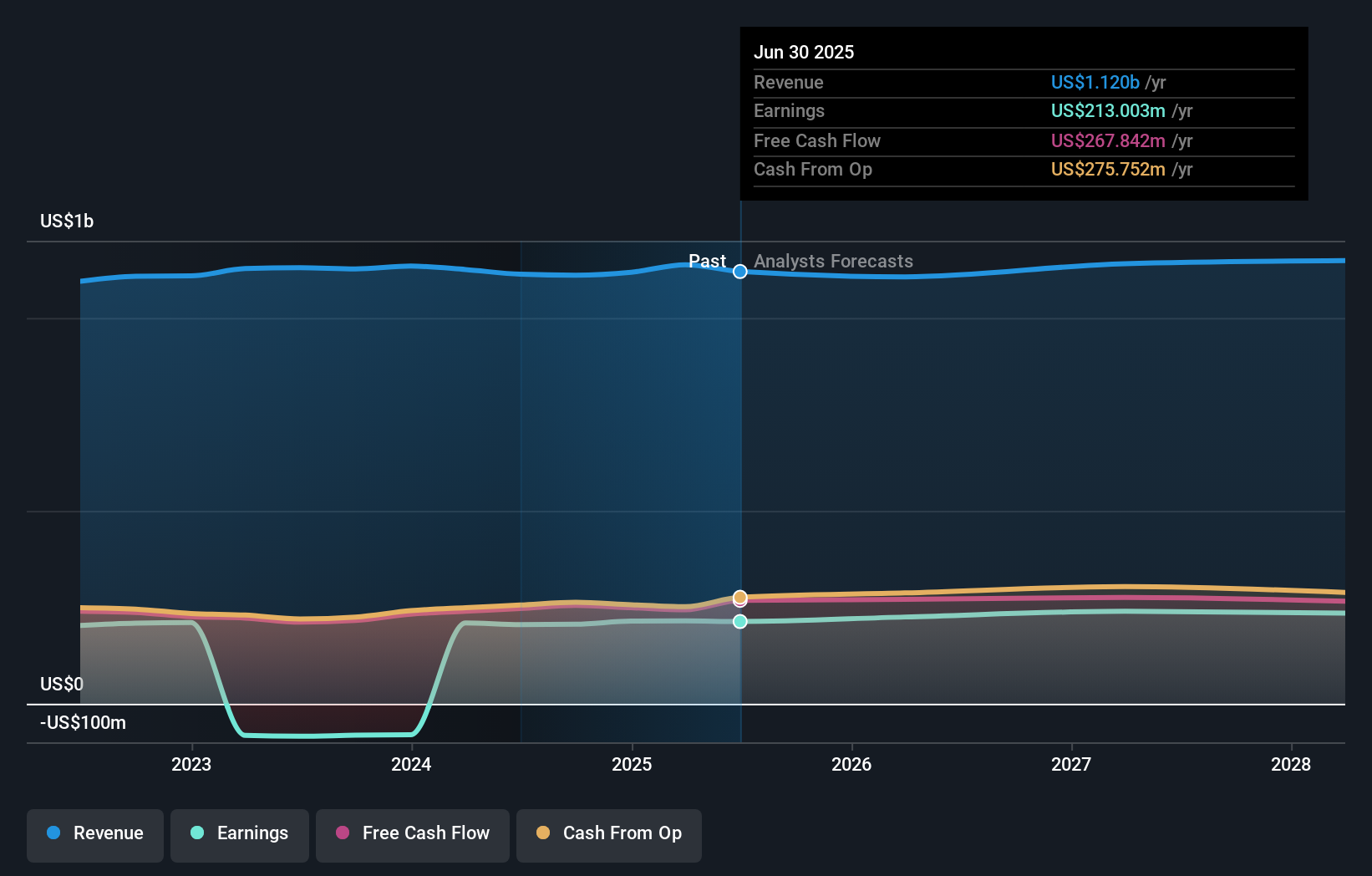

Prestige Consumer Healthcare's outlook projects $1.2 billion in revenue and $236.2 million in earnings by 2028. This is based on a 1.0% annual revenue growth rate and a $23.2 million increase in earnings from the current $213.0 million.

Uncover how Prestige Consumer Healthcare's forecasts yield a $80.17 fair value, a 33% upside to its current price.

Exploring Other Perspectives

All one of the Simply Wall St Community’s fair value estimates for Prestige stand at US$80.17, pointing to a strong consensus. However, ongoing supply recovery concerns may affect earnings momentum and could challenge optimistic valuations over time. Explore more perspectives to see how opinions differ.

Explore another fair value estimate on Prestige Consumer Healthcare - why the stock might be worth just $80.17!

Build Your Own Prestige Consumer Healthcare Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Prestige Consumer Healthcare research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Prestige Consumer Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Prestige Consumer Healthcare's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com